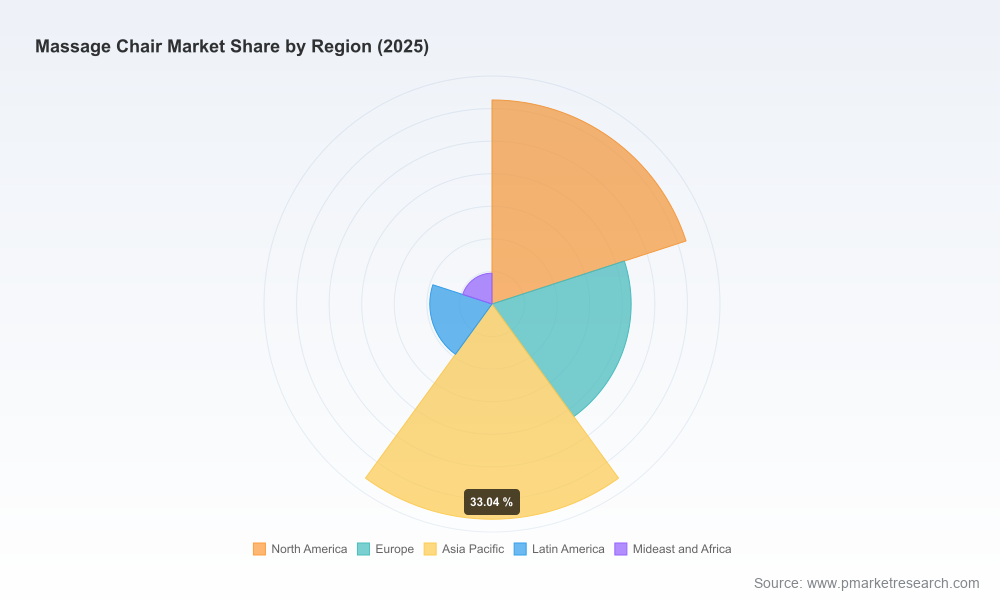

PW Consulting: Massage Chair Market to Grow at 6.98% CAGR Through 2032

Other |

2026-07-08 09:50:23

As companies prepare budgets, capital allocations and M&A strategies for 2026, they require a market intelligence product that does more than confirm known trends. PW Consulting’s Feed + Aquafeed Market study offers a decision-grade, execution-focused view of an industry in structural growth and strategic transition. This introduction summarizes the report’s strategic value for executive teams, highlighting the macro trajectory, competitive dynamics, material and regulatory pressures, and the practical tools the full study delivers — while preserving the proprietary, granular datasets that inform those recommendations.

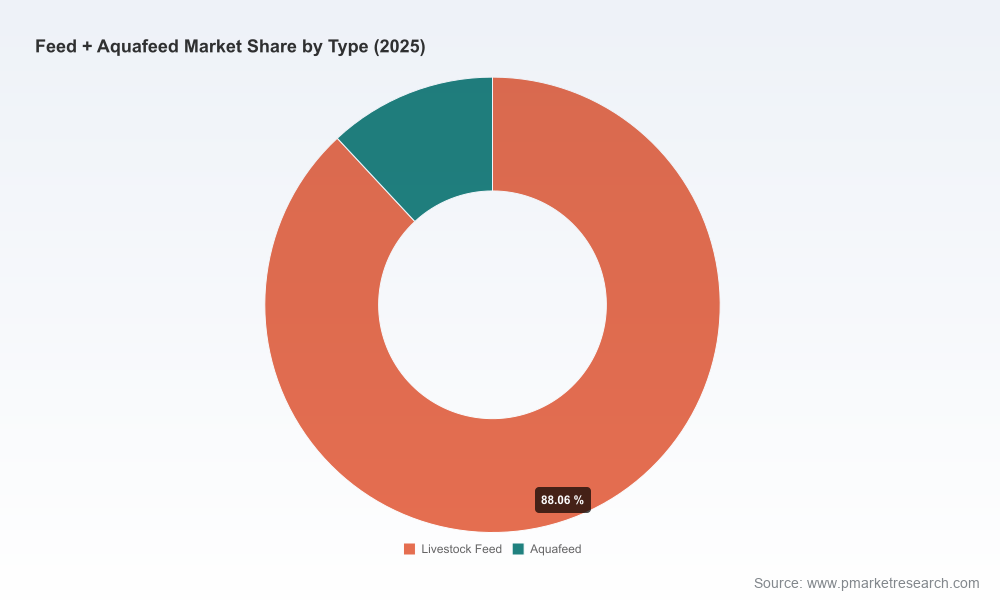

Feed + Aquafeed Market

Our base-year analysis (2025) anchors the market at USD 500 Million (USD Million units). Between 2020 and 2025 the industry expanded from a materially lower base, reflecting recovery, product premiumization and early waves of ingredient substitution. Looking forward across our 2026–2032 forecast horizon, the market is projected to grow at a compound annual growth rate (CAGR) of 6.0%, reaching an estimated USD 752 Million by 2032. That trajectory creates predictable runway for capex deployment, incremental innovation and consolidation plays — but it also underlines the need for careful targeting of product, channel and geographic exposure.

Feed + Aquafeed Market

Capital planning and plant investments: A clear mid-single-digit CAGR across 2026–2032 reduces execution risk for brownfield expansion and selective greenfield projects, but returns will vary by product mix and feed formulation specialization. Executives should align capex phasing to near-term demand inflection points highlighted in the full report.

Feed + Aquafeed Market

M&A and portfolio reshaping: Market concentration metrics indicate a moderate incumbent advantage — the top three companies account for roughly 45% of the market and the top five for about 55% — creating an environment where targeted acquisitions and bolt-on partnerships can deliver scale economics without needing blockbuster deals.

Product and pricing strategy: Premiumization (functional feeds, species-specific formulations and sustainability-branded products) is where margin expansion is most visible. Pricing strategies should be paired with validated value-capture metrics (feed conversion improvements, health outcomes, certification-related premiums), a topic we unpack with client-ready pricing models.

Supply-chain resilience and ingredient strategy: Raw-material innovation — including high-protein co-products and corn protein concentrates — is now commercially relevant. Secure sourcing strategies and inclusion trials can materially influence feed-cost volatility exposure and should be central to procurement plans.

Regulatory and certification positioning: Certification credentials and regulatory alignment (including ASC feed certifications and equivalent schemes) are becoming commercial differentiators, not just compliance items. Certification footprints materially affect market access and commercial pricing, as the competitive vignettes below illustrate.

PW Consulting’s study is structured around a single objective: convert market intelligence into implementable actions. The full report includes:

Proprietary time-series modelling (2020–2032) with scenario branches to stress-test volume, price and ingredient-fuelled margin assumptions under commodity, regulatory and disease-shock scenarios.

Supply-chain maps and supplier-scorecards that identify pinch points, alternative ingredient producers and logistics cost sensitivities.

Go-to-market playbooks tailored to B2B feed manufacturers, integrators and ingredient suppliers — including route-to-customer options, channel economics and partnership frameworks for co-development with producers.

Commercial due-diligence templates and valuation overlays for M&A targets, designed for PE and corporate development teams to rapidly triage opportunities.

Pricing and margin models that link formulation mechanics to real-world farm economics (feed conversion, growth curves, mortality impacts), enabling precise value-capture planning.

Regulatory and certification tracker with practical implications for market access and product positioning, and an impact matrix for planned certification investments.

Prioritized investment roadmap and three-year implementation calendar keyed to business objectives (expansion, premiumization, vertical integration or divestiture).

The industry’s competitive topology blends global integrators, specialized aquafeed leaders and regional champions. The report profiles market-leading players and analyzes how their strategies shift competitive advantage.

Cargill, Incorporated (Wayzata, Minnesota, United States): A diversified feed and ingredient conglomerate with multiple aquaculture-dedicated mills. Its scale and integrated procurement create cost and distribution advantages; however, tactical acceleration into functional feeds and local partnerships is where Cargill will protect margin pools.

Skretting (Stavanger, Norway): A global aquafeed frontrunner operating across many countries. Skretting’s investments in sustainability certification and strategic alliances with large producers demonstrate a playbook focused on premium products and farm-level outcomes rather than commodity volume alone.

BioMar Group (Horsens, Denmark): A specialist in high-value, species-specific formulations targeting health and performance. BioMar’s recent product introductions and certification advances make it an archetype for innovation-led growth strategies in aquafeed.

Alltech (Nicholasville, Kentucky, United States): Known for nutrition solutions and additives, Alltech is focused on maximizing feed efficiency and immune support. Its route-to-market blends ingredient solutions with advisory services, an approach that can lift customer switching costs.

Aller Aqua Group (Christiansfeld, Denmark): A producer of comprehensive feeding programmes across many species, Aller Aqua emphasizes programmatic selling and technical support — a model that scales well in markets where producers are professionalizing.

Thai Union Feedmill Public Company Limited (Bangkok, Thailand): A regional leader with premium brands and a growing global footprint. Strategic MOUs and partnerships are central to its expansion into new aquaculture markets.

Purina Animal Nutrition LLC (St. Louis, Missouri, United States): Purina’s AquaMax® portfolio addresses recreational and commercial segments; brand strength and formulation science support cross-segment expansion opportunities.

Ridley Corporation Limited (Melbourne, Australia): Specialist in extruded and pelleted aquafeeds with proprietary growth enhancers. Ridley’s technical IP positions it well in markets prioritizing production efficiency and product quality.

Recent company developments — product launches, strategic agreements and certification achievements — are not noise: they shift competitive dynamics and set near-term barometers for where commercial premiums will be paid. The full report contains deal-level implications and scenario analyses for each highlighted development.

Certification and market access: Several major producers expanded ASC certification footprints recently. Certification is not simply an ethical statement; it is increasingly embedded in procurement specs and offtake agreements demanded by large buyers and export markets.

Ingredient innovation: Trials with high-protein co-products and novel corn protein concentrates have demonstrated meaningful inclusion rates without compromising growth in select species. These developments create opportunities to diversify cost exposure and improve margin resilience.

Commercialization of functional feeds: New functional formulations targeted at species-specific disease vectors and growth stages are arriving in market. Early movers gain pricing power where clinical outcomes are validated.

Consolidation vs. specialization: The mid-market is fertile for bolt-on transactions that combine technical expertise with distribution heft. Our CR metrics indicate incumbents hold meaningful share, but the fragmented tail remains accessible for focused players.

Procurement teams: Use the supplier scorecards and ingredient-substitution scenarios to redesign procurement contracts and hedge feed-cost volatility over 12–36 month horizons.

R&D and product teams: Prioritize development pipelines toward formulations that demonstrate measurable farm-level ROI; validate through PW Consulting’s field-trial templates and metrics.

Corporate development: Apply the commercial due-diligence templates to screen targets, quantify synergies and estimate integration timelines aligned to the industry’s growth cadence.

Sales and marketing: Reframe value propositions around certified sustainability claims and health outcomes; use the go-to-market playbooks to optimize channel mix and contract terms.

Risk and compliance: Map certification investments against near-term market access needs and quantify payback periods using our certification impact matrix.

This briefing is a strategic overview designed to orient leadership teams and investment committees. The full PW Consulting Feed + Aquafeed Market study contains the complete, proprietary datasets, region- and application-level segmentation, model inputs, and downloadable decision-support tools that operational teams can apply directly to 2026 plans. For access to the full forecast models, scenario workbooks and the granular appendices that underpin the recommendations here, please consult the PW Consulting report webpage and associated client-delivery options.

In an industry where certification credentials, ingredient innovation and targeted partnerships will determine winners, having a data-backed operational roadmap is a competitive requisite for 2026. PW Consulting’s study is engineered to convert macro growth visibility into executable advantage — without hoping for serendipity. Access the full report to move from strategic intent to an operational plan that captures the market’s growing opportunity.

For detailed analysis of this topic, please visit the official page:Feed + Aquafeed Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com