Global Protective Textile Market Outlook Highlights Strong Growth Potential

Other |

2026-05-27 12:52:45

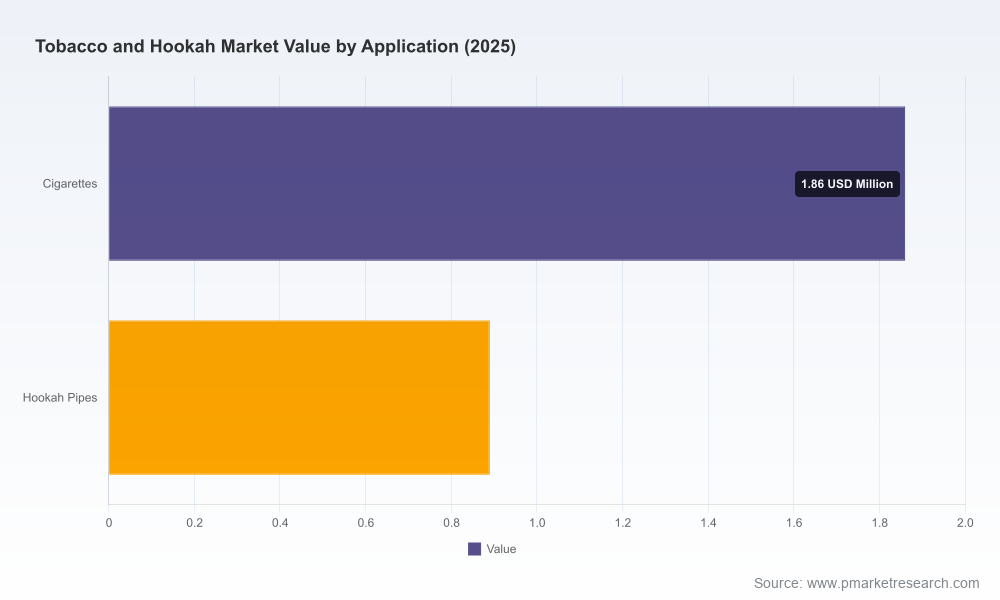

As companies position for growth in 2026, the Tobacco and Hookah market is exhibiting steady expansion under a complex overlay of regulatory shifts, input‑cost volatility and shifting competitive dynamics. Our PW Consulting market model places the global opportunity at approximately USD 2.75 Million in 2025 (base year), up from USD 2.45 Million in 2020, and projects a compounded annual growth rate (CAGR) of 3.45% through the 2026–2032 forecast window. By 2032 the model anticipates the market to reach about USD 3.46 Million—clear evidence of a low‑to‑mid single‑digit growth corridor that rewards scale, distribution reach and regulatory agility.

Tobacco and Hookah Market

Capital allocation: In an environment of modest CAGR, ROI on capacity expansion depends on optimizing channel economics and product mix rather than pure volume plays.

Tobacco and Hookah Market

Regulatory timing: 2026 is a pivot year — several regulatory initiatives and enforcement clarifications are already reshaping market access and commercialization risk profiles.

Tobacco and Hookah Market

Competitive displacement: Fragmentation persists alongside pockets of aggregation; incumbents and nimble challengers are converging on the same premium, flavored and alternative product pools.

From a regional and product‑agnostic standpoint, our consolidated series shows an industry that recovered from short‑term oscillations and resumed steady expansion into 2025. The market grew from approximately USD 2.45 Million in 2020 to USD 2.75 Million in 2025, and our forecast carries that to near USD 3.46 Million by 2032 at a 3.45% CAGR. This trajectory signals a market large enough to sustain specialist players while remaining sensitive to cost inflation, tax adjustments and shifts in consumer preference toward alternatives (heated tobacco, ENDS, etc.).

U.S. regulatory posture: The U.S. Food and Drug Administration (FDA) has updated guidance on enforcement priorities for unauthorized ENDS and nicotine pouch products and expanded market authorizations in mid‑2026—moves that materially affect market entry timelines and product labelling strategies for firms selling within or into the U.S.

European tax modernization: Proposals to modernize excise frameworks and extend taxation to electronic nicotine products are in motion. Firms selling across multiple markets should anticipate higher effective tax rates and plan pricing and product architecture accordingly.

State‑level constraints: Local measures—such as California’s recent restrictions related to co‑location of cannabis product sales at tobacco retailers—illustrate the growing importance of channel compliance and point‑of‑sale segregation strategies.

Input prices are materially consequential for margin management. Recent analyst data show raw tobacco leaf prices varying by quality and origin (roughly in the low single‑dollar per pound range up to higher grades), while premium flue‑cured varieties have recorded locally elevated prices in specific origins. These dynamics create a dispersion of input cost across suppliers and geographies: manufacturers that secure long‑dated contracts, vertically integrate critical inputs, or implement more efficient flavor and humectant usage will protect gross margin differential into 2026 and beyond.

The market exhibits moderate concentration: our concentration metrics show the top three firms account for under one third of the market (CR3 approx. 28.5%), while the top five approach the low‑forties (CR5 approx. 42.3%). This structure creates a two‑track competitive reality:

Global producers and brand‑builders: Regional headquarters and legacy manufacturers—companies with established export channels and flavor portfolios—are leveraging scale in procurement and distribution. Examples include long‑standing producers and exporters of flavored hookah molasses and associated coal/consumables. These firms are prioritizing product consistency, food‑safety certification and cafe‑channel partnerships.

Large tobacco incumbents and alternative nicotine entrants: Major tobacco multinationals and ENDS specialists are encroaching on the same consumer cohorts with diversified product sets that include heat‑not‑burn, vape solutions and branded hookah offerings. Their advantage is capital for compliance investments, broad regulatory affairs capabilities and integrated route‑to‑market networks.

Key company archetypes represented in our competitive review include independent shisha manufacturers and exporters, integrated global OEMs, online and omnichannel retailers, and multinational incumbents adapting legacy advantage to alternative segments. Each archetype requires a distinct playbook for partnerships, pricing, and regulatory engagement.

Our full report is built for commercial and corporate leaders who need executable intelligence rather than academic snapshots. Highlights include:

Proprietary market model (historical 2020–2025, forecasts 2026–2032) with scenario toggles for regulatory tightening, excise shocks and commodity inflation.

Go‑to‑market playbooks for three archetypes: global producers, regional specialists and multinational tobacco groups—each with tailored channel mixes, promotional strategies and cost levers.

Regulatory heatmaps and decision trees mapping authorization risk, labelling compliance steps and time‑to‑market implications for major jurisdictions.

Margin sensitivity tools that model raw material price bands, excise shifts and packaging/transport cost inputs to quantify break‑even for capacity investments.

Corporate development briefs—M&A checklists, valuation comparables and integration risk flags for bolt‑on plays and cross‑category acquisitions.

Note: The report contains the granular segmentation tables, regional and application splits, and company‑level share matrices. We intentionally omit those tables from this introduction to preserve source exclusivity and to invite direct access to the full dataset.

Prioritize regulatory‑first product roadmaps. Assign scarce R&D and regulatory budget to variants and markets with the clearest, fastest path to compliant market access under 2026 guidance.

Hedge critical input exposure. Negotiate multi‑year leaf contracts, consider partial vertical integration and explore alternative humectant and flavor suppliers to reduce unit cost volatility.

Optimize channel economics over volume. In a modest growth market, tightening unit economics via direct‑to‑consumer channels, premiumization and subscription models will outperform broad low‑margin expansion.

Segment with a purpose. Use consumer clustering to prioritize SKUs—focus on variants where brand loyalty and higher margins can be projected within the new regulatory texture.

Prepare for excise drift. Build pricing playbooks and tax scenarios into your 2026 commercial plan; test elasticity assumptions with small geographic pilots before full rollouts.

Design flexible M&A screens. Target bolt‑ons that accelerate compliance capabilities (labelling, testing, market files), add distribution in underrepresented channels, or provide raw material security.

We model three plausible 2026 scenarios: 1) Baseline (policy and cost trends continue at current cadence), 2) Tightening (accelerated excise and expanded regulator scrutiny) and 3) Disruption (rapid consumer shift to non‑combustible alternatives). Each scenario produces distinct trade‑offs between capex and opex investments—e.g., in a tightening scenario, firms that pre‑invest in compliance and product reformulation secure premium shelf space and avoid costly recalls; in a disruption scenario, reallocating budget toward alternative nicotine formats yields higher long‑term growth capture. The key is to operationalize trigger thresholds and staged funding that allows moves without full commitment until signals crystallize.

Translate market CAGR and trajectory into rolling 18‑month investment gates tied to regulatory milestones and commodity benchmarks.

Create a cross‑functional 90‑day regulatory sprint to lock down launch readiness for prioritized SKUs and markets.

Run a value‑at‑risk assessment on raw material exposure and tax policy shifts, then hedge or insure where downside exceeds board risk appetite.

For executives, the 2026 imperative is to convert steady market growth into predictable, defensible returns by combining regulatory foresight, supply‑chain resilience and targeted commercial discipline. PW Consulting’s Tobacco and Hookah market study delivers the layered analytics—forecasting, scenario stress‑testing, competitive benchmarking and executable playbooks—needed to make those trade‑offs with confidence. To access the full segmentation tables, company share matrices, and downloadable financial models that underpin the analysis summarized above, please consult the PW Consulting report landing page.

For detailed analysis of this topic, please visit the official page:Tobacco and Hookah Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com