PW Consulting Forecasts 14.5% CAGR for High‑Barrier MDO‑PE Film Market Through 2032

Other |

2026-07-02 11:20:27

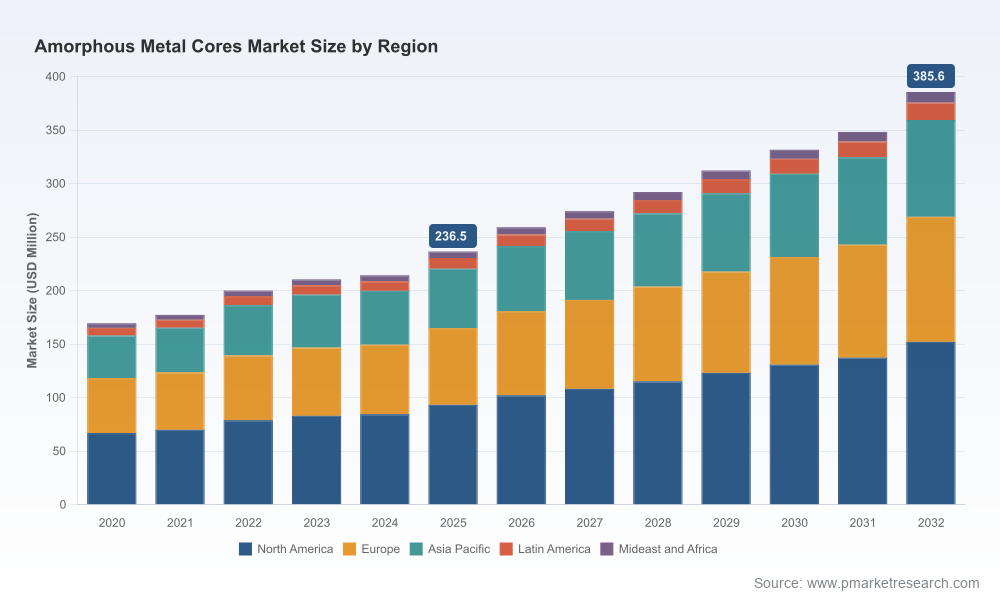

As companies retool product portfolios and supply chains for the energy- and efficiency-led markets of the late 2020s, amorphous metal cores are moving from niche engineering advantage to a near-term strategic lever. Our market model shows that the global amorphous metal cores industry expanded meaningfully through the early 2020s — from a modest industrial base in 2020 to a substantially larger market by 2025 — and is set to continue growing through the 2026–2032 forecast window at a compound annual growth rate of 7.5%. By 2032, the market is projected to be materially larger than it was in 2025, reflecting accelerating adoption in energy distribution, power electronics, and specialized industrial applications.

Amorphous Metal Cores Market

This introduction explains why the 2026 inflection matters to boardrooms, outlines the practical weaponry this PW Consulting study delivers, and profiles the competitive set shaping supply, technology and pricing dynamics. It purposefully demonstrates analytical depth while withholding granular segment-level figures to motivate follow-up and access to the full report for transaction-grade detail.

Amorphous Metal Cores Market

Trajectory: The market moved from a defined baseline in 2020 through steady growth to a materially larger base in 2025, and is forecast to expand through 2032 at a 7.5% CAGR. This trajectory reflects a mix of replacement demand (energy-efficiency upgrades), new-build transformer and power-electronics demand, and increasing interest in high-frequency and pulse applications where amorphous alloys can outperform conventional silicon steel.

Amorphous Metal Cores Market

Structural takeaway: Growth is durable but selective. Adoption is concentrated in applications where efficiency improvements or form-factor advantages translate directly to operating cost savings or system-level performance gains. That makes the technology particularly attractive to utilities, industrial OEMs, and engineered systems suppliers pursuing life-cycle cost reductions and carbon-intensity targets.

Timing: 2026 is pivotal. Several large-scale capacity and localization moves announced in late 2025 and early 2026 change the supply/cost calculus for customers and potential acquirers. Strategic actors should treat 2026 as the year to lock preferred supplier arrangements, accelerate qualifying programs for alternative alloys, or engage in M&A discussions before new capacity materially shifts pricing expectations.

Energy policy and procurement: Decarbonization targets and stricter grid efficiency standards are forcing utilities and distribution transformer specifiers to consider total life-cycle costs. Amorphous metal cores offer no-load loss reductions that operators can monetize over equipment lifetimes, creating procurement windows for suppliers that can demonstrate validated field performance.

Product differentiation in power electronics: In power-dense topologies and high-frequency applications, amorphous and nanocrystalline alloys deliver advantages in core loss and saturation behavior. Suppliers that pair core materials with optimized winding and thermal designs can command premium positioning.

Localization and supply security: New regional capacity and localization announcements in 2026 change the geopolitical and logistical calculus for buyers. Sourcing strategies that previously relied on long-haul supply must be re-evaluated against faster local delivery, shorter lead-times, and potential cost-of-ownership improvements.

Procurement and supplier strategy: Companies should re-segment supplier panels into (a) validated high-performance alloy suppliers, (b) cost-optimized volume producers, and (c) strategic partners for R&D co-development. Use the full report’s supplier scorecards and visit-to-auditor frameworks to triage sourcing decisions. Initiate dual-sourcing pilots with production insurance clauses where the total cost of ownership (TCO) advantage is marginal but operational risk is significant.

R&D and product roadmaps: Prioritize qualification programs that map alloy grades to end-use loss profiles and thermal envelopes. The best commercial outcomes come from matching core metallurgy with winding architecture and cooling regimes, not from a material-only substitution. Fund accelerated prototyping lanes for next-generation topologies where core losses materially determine system efficiency.

Manufacturing and capacity planning: Treat announced greenfield capacity and localized production as potential game-changers for regional pricing and lead times. Capital planning models should incorporate scenario runs where new regional capacity comes online within the next 12–18 months and where incremental volume is absorbed by incumbent players versus open-market buyers.

M&A and partnerships: The market exhibits moderate concentration: the top three and top five firms control an appreciable but not dominant portion of the market, leaving room for tactical consolidation and bolt-on plays. Potential acquirers should use the report’s valuation multiples, synergy calculators, and integration risk templates to size acquisition opportunities against near-term capacity expansions and technology roadmaps.

Commercial and pricing strategy: As adoption shifts from technical pilots to procurement line-items, strategic sellers can capture value by packaging material supply with validation services, warranty-backed performance, and efficiency guarantees. Buyers should demand outcome-based contracts that align price with realized no-load loss improvements and deployment metrics.

The report is built for decision-makers. It synthesizes proprietary market modeling, supplier interviews, plant-level capacity mapping, and techno-economic analysis into actionable outputs:

Market sizing and long-form forecasts (base year 2025; forecast window 2026–2032) with scenario sensitivity across adoption curves and price trajectories.

Demand-side segmentation by application class, type, and region, with TCO case studies showing when amorphous cores become the rational buy vs. conventional alternatives.

Supplier benchmarking and capacity maps, plus risk heatmaps for single-source exposure and critical raw material pinch points.

Commercial playbooks: procurement templates, product qualification roadmaps, and energy-savings claim validation protocols.

M&A toolkit: target shortlists, valuation scorers, and post-merger integration checklists focused on technology transfer and production ramp risk.

Note: Detailed, segment-level tables and downloadable datasets — including granular regional and application splits — are intentionally reserved for the full report to enable transaction-grade analysis.

The competitive set combines heritage producers with regional volume players. Key companies profiled in the study include global technology proprietors and aggressive regional manufacturers. High-level profiles and strategic implications follow (profiles reference company headquarters and public positioning):

Proterial, Ltd. (Tokyo, Japan) — Primary producer of Metglas™ amorphous ribbon used extensively in transformer cores. Proterial operates established sites and has signaled strategic localization with a capacity expansion announced in early 2026: a new production site in Sri City, India (30,000 t/year capacity, starting October 2026). That move reshapes regional supply economics and underscores Proterial’s commitment to serving utility-driven efficiency programs through localized manufacturing.

Metglas, Inc. (South Carolina, USA) — Part of the Proterial group with U.S.-based production that focuses on distribution transformers and core products. The Metglas brand remains important in markets where long-term field performance and qualification history carry premium value with utilities and OEMs.

VACUUMSCHMELZE GmbH & Co. KG (Hanau, Germany) — A materials-technology leader offering VITROVAC® grades, including Fe-based options with high saturation flux densities used in power and pulse applications. Their product depth and application engineering services make them a partner of choice for higher-frequency or high-performance designs.

Advanced Technology & Materials Co., Ltd. (Beijing, China) — Large-scale manufacturer focused on volume production of amorphous and nanocrystalline ribbons and cores, serving transformer and electronic markets with cost-competitive offerings.

Qingdao Yunlu Advanced Materials Technology Co., Ltd. (Qingdao, China) — Regional leader with strong emphasis on energy-efficient transformer cores and aggressive product development toward localized utility specifications.

Zhejiang Zhaojing Electrical Technology Co., Ltd. (Zhejiang, China) — Specialist in C-cores and ribbon products for distribution transformers, with tight integration into domestic transformer OEM supply chains.

China Amorphous Technology Co., Ltd. (Foshan, China) — Producer of amorphous/nanocrystalline cores for soft-magnetic applications, competing on both product breadth and local service capabilities.

Henan Zhongyue Amorphous New Materials Co., Ltd. (Henan, China) — Focused on strips and cores for distribution transformers and industrial magnetic components, offering scale on commodity grades.

Collectively, the market shows moderate concentration: the leading three and five players account for a material, but not dominant, portion of industry revenue — a dynamic that creates scope for consolidation, regional niche plays, and price differentiation strategies.

Energy savings: Manufacturer claims quantify that amorphous cores can reduce transformer no-load loss by roughly one-third versus typical electromagnetic steel sheet solutions. Buyers should require validated field-study data and harmonized test protocols to convert manufacturer claims into procurement-grade performance guarantees.

Material characteristics: Some VITROVAC® Fe-based grades report high saturation flux densities (product literature cites values up to ~1.74 T), a property that matters in designs where saturation margin and magnetic flux density dictate performance under transient loading.

Boards and investment committees: Use the forecast scenarios and sensitivity analyses to stress-test capital allocation, especially for companies contemplating capacity expansion, vertical integration, or acquisitions in feedstock or alloy production.

Procurement leads: Deploy the report’s supplier scorecards and TCO models to renegotiate contracts or to qualify new regional suppliers introduced during 2026 capacity additions.

Product and engineering teams: Leverage the technical annexes to prioritize alloy qualification runs and to quantify system-level efficiency gains for quoting and warranty strategies.

This preview surfaces the strategic contours you need to prioritize near-term decisions but intentionally omits transaction-grade segment tables and region/application splits. To obtain the full dataset — including granular segmentation, pricing curves, downloadable company screening sheets, and scenario models to run your own sensitivity tests — please access the full Amorphous Metal Cores Market report on our web portal. The full report contains the precise segment-level metrics and appendices required for procurement RFPs, M&A diligences, and capital planning.

PW Consulting stands ready to translate the study’s insights into bespoke scenario analyses, supplier RFPs, or integration plans to support M&A. For executives preparing capital budgets or sourcing strategies in 2026, acting early on the signals highlighted here will materially improve negotiating leverage and execution timelines.

For detailed analysis of this topic, please visit the official page:Amorphous Metal Cores Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com