Spectra Perfume: A Modern Fragrance Experience

Shopping |

2026-05-23 09:36:56

As companies plan capital allocation, sourcing strategies, and product roadmaps for 2026, the triacetin market presents a classic mix of steady growth, regulatory pressure, and concentrated supply dynamics. PW Consulting’s new Triacetin Market study (base year 2025) synthesizes five years of historical tracking (2020–2025) and a 2026–2032 forecast horizon driven by a 5.12% compound annual growth rate (CAGR). The total market — measured in USD Million — grew materially through 2025 and is projected to advance meaningfully across our forecast window, creating clear decision inflection points for buyers, producers, and investors.

Triacetin Market

Budgeting and capex timing: An established mid-single digit CAGR through 2032 makes triacetin an attractive, predictable investment for downstream formulators seeking margin stability while they retrofit product lines for regulatory compliance.

Triacetin Market

Sourcing and raw‑material strategy: Feedstock pathways and availability are shifting; choices made in 2026 about glycerin sourcing, purification capital, and contract structures will lock in unit economics for the next business cycle.

Triacetin Market

Regulatory readiness: Tightened migration limits and traceability requirements will convert to operational costs and product development constraints unless anticipated in 2026 roadmaps.

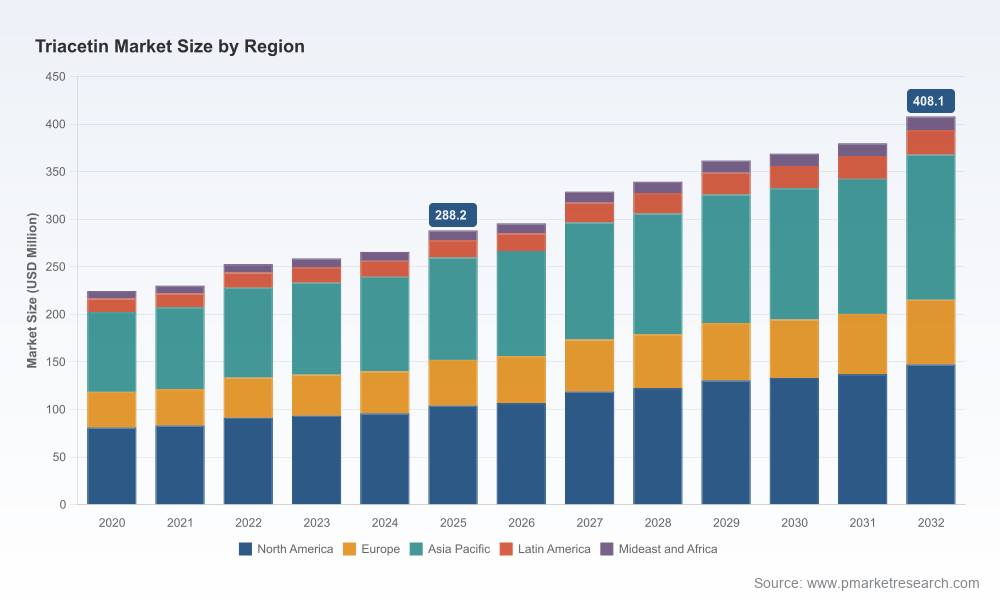

PW Consulting’s headline model puts the market size at USD 288.2 Million in 2025 (base year), with a steady advance thereafter driven by both volume growth and value capture through specialty, higher‑purity SKUs. By 2032 our top‑line projection reaches USD 408.1 Million under the central 5.12% CAGR pathway. Market concentration metrics indicate a moderately consolidated structure (CR3 ≈ 47.5%, CR5 ≈ 58.2%), implying that leading producers retain meaningful pricing influence while mid‑tier competitors still command material niches. These macro indicators should be treated as the strategic context for 2026 procurement, R&D, and M&A decisions.

Product formulation momentum: Demand is being sustained across legacy end uses (plasticizers and solvents) and higher‑value applications where triacetin’s physicochemical profile — low volatility, plasticizing performance, solvent compatibility — enables reformulation toward cleaner‑label and pharmaceutical excipient uses.

Regulatory arbitrage and premiumization: Tighter migration and purity thresholds are bifurcating the market between commodity technical grades and premium, fully verified high‑purity grades. Firms that can demonstrate robust traceability and batch‑level analytics will achieve price differentials.

Feedstock evolution: The supply base is evolving. Synthetic glycerin still supplies a majority of output, while vegetable‑glycerin routes are expanding at notably higher growth rates. This has implications for cost curves, sustainability credentials, and access to pharma‑grade intermediates.

Regulation (EU) 2025/351 – practical consequences: The European Commission’s 2025 mandate requires exhaustive documentation for every food‑contact triacetin batch and establishes a strict migration limit at 0.05 mg/kg. Compliance requires investment in analytical capacity, chain‑of‑custody systems, and potentially reformulated compositions to achieve the margin targets in food applications.

REACH amendments and UK protocols: Parallel tightening under REACH and evolving UK e‑liquid/aerosol testing protocols — which require toxicological substantiation for products containing triacetin at low weight‑percentages — mean that one‑off product approvals are no longer sufficient. Firms should standardize robust toxicology and migration dossiers in 2026.

Feedstock arbitrage and pricing: Crude glycerol from biodiesel side‑streams continues to present a discounted pathway into purification chains — a lever for producers aiming to compete on cost. At the same time, synthetic glycerin remains the predominant source of triacetin output; any feedstock shocks or policy shifts that affect glycerin economics will cascade quickly into the triacetin price deck.

Observed supplier behavior through 2025 signals a market that is responsive but cautious. Notable industry actions include:

Eastman Chemical Company implemented staged price increases on technical grades in 2025 (announced January and adjusted again in April, with the latter specifying a $0.04 per lb adjustment for technical triacetin). These moves function as a real‑time signal of tighter margins and underscore the pricing leverage that integrated producers can exert.

Regulatory layers introduced in 2025 have forced a reclassification of premium SKUs across Europe, creating a commercialization window for suppliers that can guarantee migrational behavior under new thresholds.

Our competitive analysis focuses on established producers that together shape supply reliability, technical service capability, and price formation. PW Consulting’s report includes detailed supplier scorecards; below are the strategic highlights and implications for 2026 decisions.

Eastman Chemical Company (Kingsport, Tennessee): Offers TRIACETIN™ technical grades targeted at cellulosic resins and acetate filters. Strengths: integrated downstream channels, strong technical‑support offering. Strategic implication: Eastman’s pricing behaviour should be a benchmark for short‑term contract negotiations and a trigger for buyers to evaluate alternate technical sources if flexibility is necessary.

Daicel Corporation (Osaka): Produces triacetin in tandem with tri‑acetyl cellulose operations. Strengths: manufacturing synergies and diversified end‑use pathways. Strategic implication: Partnerships with vertically integrated producers can secure differentiated SKUs for pharmacopeial or food‑grade end uses.

LANXESS (Cologne): Markets TRIACETIN® targeting PVC and polymer applications. Strengths: polymer science expertise and channel access in industrial applications. Strategic implication: Where polymer performance is a differentiator, aligning with LANXESS can accelerate reformulation timelines.

Polynt S.p.A. (Cologno Monzese): Produces specialty glycerol triacetate esters suited for food packaging and confectionery at dedicated sites. Strengths: niche product engineering and localized food‑grade expertise. Strategic implication: For premium food applications and packaging, consider multi‑sourcing to balance compliance risk and supply security.

BASF SE (Ludwigshafen): Supplies Kollisolv GTA for pharmaceutical and personal care applications. Strengths: excipient know‑how and regulatory dossiers. Strategic implication: Buyers targeting pharmacopeial channels should prioritize suppliers with established excipient records and regulatory submissions.

Base case: Continued mid‑single‑digit CAGR with premiumization of high‑purity product lines; regulated markets absorb compliance costs into price structures.

Upside: Faster substitution into pharmaceutical and personal care segments driven by reformulation trends and validated excipient performance; higher share of vegetable‑glycerin feedstocks may create new value pools.

Downside: Feedstock shocks or a regulatory ban on specific acetylation routes could compress volumes and force temporary dislocation; non‑compliant suppliers may be excluded from key markets, tightening supply and lifting prices.

The full study is designed as a working tool for 2026 executives. Key deliverables include:

Forward‑looking demand model (2026–2032) with scenario toggles for feedstock mix, regulatory stringency, and substitution effects.

Supplier scorecards and a procurement playbook: qualitative and quantitative assessments of technical capability, traceability systems, and price elasticity. This includes hands‑on negotiation levers for sourcing teams.

Regulatory matrix and compliance checklist mapped to product development stages (including batch‑level documentation templates aligned to EU 2025/351 and REACH amendments).

Price‑deck analytics and margin sensitivity tables that translate glycerin pathway changes into finished‑goods impact (USD Million level and unit cost scenarios).

Operational readiness templates: recommendations for lab investments, analytical capability, and supplier‑audit protocols to achieve high‑purity claims at scale.

M&A and investment screeners: criteria and valuation heuristics for buyers and private equity investors targeting triacetin‑adjacent assets.

Procurement: Lock in multi‑year contracts with optionality for feedstock substitution; include performance‑based clauses tied to migration and purity thresholds.

R&D: Prioritize analytical method development and co‑validation with chosen suppliers to reduce time‑to‑market for regulated SKUs.

Operations: Stage purification and QA investments where biodiesel‑derived glycerol will be used as feedstock, and model the capex payback under different price decks.

Commercial: Segment customers by regulatory exposure and willingness to pay for documented high‑purity triacetin; launch premium SKUs with fortified dossiers for Europe and pharmaceutical channels.

M&A/Strategic partnerships: Target bolt‑on assets that enhance traceability and analytical throughput, or JV structures with glycerin refiners to secure high‑purity streams.

This briefing intentionally highlights the strategic signals, macro figures, and operational levers that will matter in 2026 while omitting granular subsegment tables and certain proprietary split data to preserve investigative value. PW Consulting’s full Triacetin Market Report contains the granular regional, grade, product‑type, and end‑use breakouts, supplier financials, and downloadable model workbooks that permit client‑specific scenario runs. If your 2026 planning requires transaction‑grade analysis, supplier benchmarking, or an executable procurement playbook, consult the full report and data pack on the PW Consulting Triacetin Market page.

For detailed analysis of this topic, please visit the official page:Triacetin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com