Access Control Reader Market Insights and Growth Trends

Other |

2026-06-06 11:13:45

As organizations expand computing into the most austere environments—from frontline military operations to offshore energy platforms and temperamental industrial yards—the market for rugged notebooks is transitioning from a niche procurement line item into a strategic hardware category. PW Consulting’s latest Rugged Notebooks Market study, with a base year of 2025 and a forecast horizon stretching through 2032, unpacks that transition with operationally actionable analysis designed to influence procurement, product strategy, channel planning and M&A decisions in 2026.

Rugged Notebooks Market

Decision velocity: Procurement and product teams face compressed timelines to specify devices that must now support edge AI workloads, hardened connectivity and extended lifecycle services. The report translates market signals into decision-ready specifications and vendor shortlists.

Rugged Notebooks Market

Risk framing: Geopolitical, regulatory and standards pressures (e.g., MIL‑STD, IP ratings, electromagnetic compliance) materially affect certification timelines and supplier selection. Our analysis quantifies these program risks and recommended mitigation steps.

Rugged Notebooks Market

Value capture: The study couples top‑down market sizing with bottom‑up cost and total cost of ownership (TCO) constructs to reveal where manufacturers, integrators and channel partners can extract margin—or where buyers can negotiate hard.

Using 2025 as the analytical base year, PW Consulting maps the rugged notebooks market across a consistent 2020–2025 historical window and projects through 2026–2032. The market expanded from roughly USD 180 million (2020) to approximately USD 235 million in 2025, reflecting resilience through pandemic disruptions and early supply‑chain normalization. From that base, our model forecasts a compound annual growth rate (CAGR) of 7.5% across the 2026–2032 forecast period, reaching an estimated USD 375 million by 2032 under the base scenario.

Those headline numbers conceal important inflection points: a post‑2022 acceleration driven by growing demand for AI‑capable edge devices, renewed defense procurement cycles, and rising adoption in industrial IoT ecosystems. Conversely, episodic supply constraints and component pricing volatility introduce downside risk that scenario analysis in the report quantifies for planners.

Market sizing and methodology: Transparent models, assumptions and baseline datasets (2020–2025 historical), plus scenario builds for conservative, base and upside 2026–2032 cases.

Demand drivers and buyer personas: Segmented buyer intelligence (enterprise industrial fleets, public safety agencies, defense programs, logistics operators) and explicit requirements matrices to map form‑factor, performance and certification needs to procurement criteria.

Use‑case ROI modules: Realistic TCO and ROI models for pilot-to-scale rollouts—covering device procurement, lifecycle maintenance, ruggedization premiums, and salvage/resale assumptions.

Go‑to‑market playbooks: Channel strategies, service bundles and aftermarket programs that increase ARPU and reduce churn for OEMs and distributors.

Supplier scorecards and partner heatmaps: Frameworks for evaluating vendors on certification, engineering depth, supply resilience, software ecosystems and aftermarket coverage.

Competitive benchmarking and M&A prioritization: Comparative positioning across capability vectors and a short list of acquisition targets or partnership profiles for both scale and capability consolidation strategies.

Regulatory and standards atlas: Practical checklists for MIL‑STD specifications, IP ingress ratings, electromagnetic compliance and industry‑specific certifications (e.g., ATEX), including anticipated timelines and testing bottlenecks.

The market retains a mix of global OEMs with broad enterprise channels and specialized manufacturers that dominate program‑level procurements. Measured concentration is moderate—our CR3 sits at 22% and CR5 at 32%—indicating a competitive field where specialist engineering and service models are meaningful differentiators.

Dell Technologies (Round Rock, Texas): Leverages scale and enterprise relationships to push ruggedized variants of mainstream platforms. Recent expansions to include discrete GPUs for AI workloads signal a move to capture higher‑value, data‑intensive field applications.

Getac (Taipei): Maintains a technology‑led position with magnesium and polymer chassis engineering and a steady cadence of product introductions oriented to AI readiness and stringent MIL‑STD certifications. Their work on integrating Copilot‑class experiences reflects the push to embed higher software value into rugged form factors.

Panasonic Toughbook (Osaka): Brand strength in military and field operations remains a high‑value asset. Toughbook’s engineering emphasis on full‑rugged designs keeps it in contention for mission‑critical procurements where established certification pedigrees matter.

Zebra Technologies (Lincolnshire, Illinois): Focused on tablets and 2‑in‑1s, Zebra’s advantage is enterprise platform flexibility and verticalized solutions for logistics, public safety and field services.

Regional and specialist OEMs (e.g., Roda, Winmate, Durabook, Xplore, RuggON): These players win through deep vertical engineering, rapid customization, and localized service. They are often preferred partners for defense primes, marine operators, and industrial integrators.

Recent product developments underscore an industry pivot: the integration of AI accelerators, increased thermal budgets for edge inferencing, and new software–hardware co‑designs aimed at operational analytics in the field. Vendors who combine hardened hardware with a coherent software and lifecycle service proposition will command better pricing power and longer account penetration.

Design and procurement teams must now budget not only for unit cost but for certification timelines and compliance testing. Key reference points—such as MIL‑STD‑810H (environmental resiliency), MIL‑STD‑461G (electromagnetic compatibility), and ingress protection ratings (IP66/IP67)—are non‑negotiables for many buyers. The report translates those requirements into test schedules, cost bands and supplier pre‑qualification checklists to avoid program delays.

Embed compute for edge AI: Prioritize modular designs that allow GPU/accelerator upgrades without full chassis replacement; furnish clear performance baselines for inferencing workloads.

Certify once, sell many: Invest in accelerated certification pathways and shared test artifacts to reduce time‑to‑market for variant SKUs targeted at regulated buyers.

Build service‑led differentiation: Offer lifecycle warranties, in‑field service hubs, and device management suites that convert hardware buyers into recurring revenue clients.

De‑risk supply chains: Dual‑sourcing for critical components and regional assembly options reduce exposure to single‑point disruptions.

Pursue targeted M&A: For OEMs seeking capability rather than scale, acquiring specialist providers with certification laboratories or vertical content (e.g., defense‑grade I/O, vehicle mounts) accelerates market entry.

Adopt sustainability and repairability metrics: Enterprise buyers increasingly demand lifecycle transparency—repair programs and parts availability will influence procurement rankings.

For C‑suite strategists, procurement leads and product managers, PW Consulting’s Rugged Notebooks Market study provides:

Actionable vendor shortlists tied to use‑case matrices so teams can fast‑track RFQ/RFP cycles in 2026.

Quantified scenario analyses that translate market growth (7.5% CAGR forecast through 2032) into budgetary guidance and inventory plans.

Operational checklists for certification, supply chain resilience and integration testing that reduce program slippage risk.

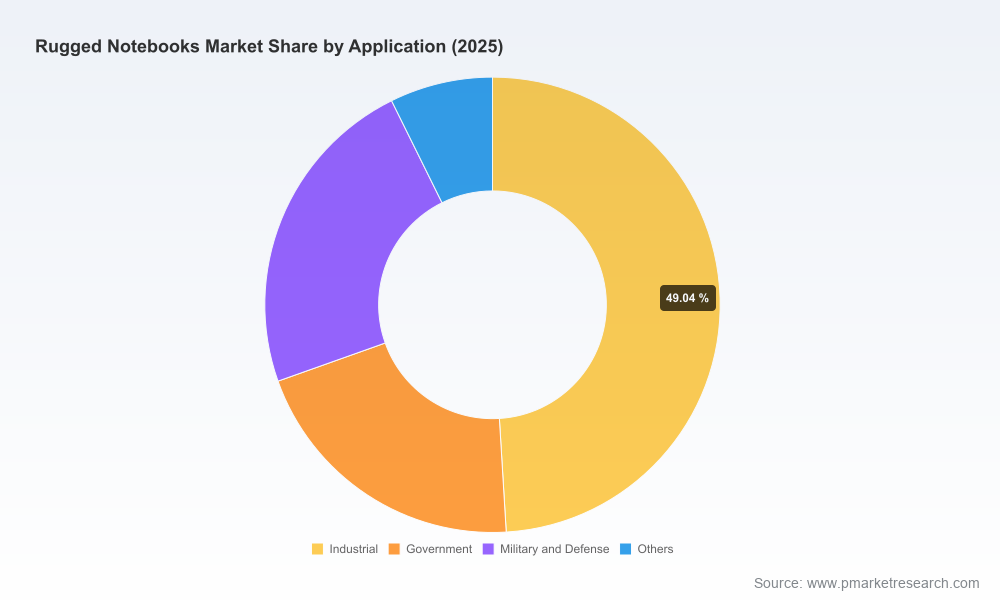

This briefing is intentionally selective: it presents the market’s strategic contours, vendor positioning and practical imperatives while withholding detailed segment‑level tables, region‑ and application‑level revenue breakdowns, and the full dataset used to power our models. Those granular datasets and proprietary segmentation analytics are available in the full PW Consulting report and accompanying Excel workbooks—resources designed for immediate incorporation into procurement specifications, product roadmaps and M&A diligence packages.

If you are aligning budgets or shaping product roadmaps for 2026, the report will accelerate decision quality by converting market signals into executable next steps. For access to the complete analysis, dataset downloads and bespoke advisory engagements, please visit the PW Consulting report page referenced in your client communications.

PW Consulting — translating rugged market complexity into practical strategy for organizations that operate where standard IT cannot go.

For detailed analysis of this topic, please visit the official page:Rugged Notebooks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com