Polyimide (Kapton) Tape Market: Strategic Implications for 2026 — A PW Consulting Industry Primer

As companies recalibrate product roadmaps, supply chains and M&A pipelines for a more volatile post‑pandemic macrocycle, the polyimide tape market presents a classic case of a technically specialized commodity experiencing structural demand uplift. PW Consulting’s latest market study synthesizes five years of historical performance and a seven‑year forecast to illuminate where value will be created — and where strategic missteps are most costly — through 2032. This primer lays out the high‑level, decision‑centric takeaways for executive teams planning 2026 actions, while reserving the granular segment matrices and proprietary scenario models for the full report.

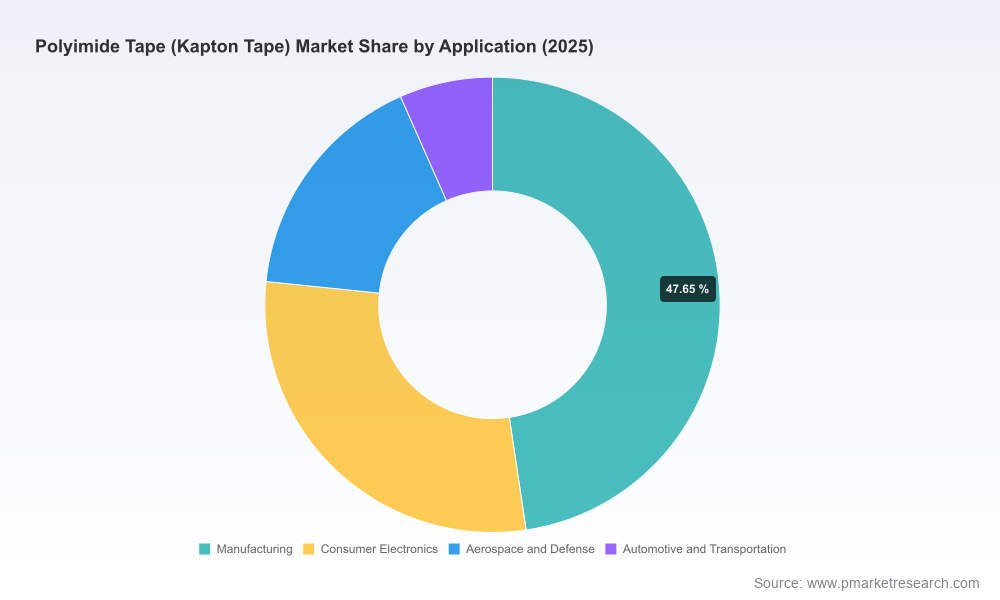

Polyimide Tape (Kapton Tape) Market

Market Snapshot: Growth Trajectory and Structural Momentum

The polyimide tape market has moved from a mature niche into a growth runway driven by electrification, semiconductor manufacturing complexity, and aerospace/defense requirements. On a headline level, total market revenue rose from approximately USD 790 Million in 2020 to around USD 1,210 Million in 2025. Our forecast models — built from bottom‑up demand drivers, capacity evolution, and regulatory scenarios — project continued compound growth at roughly 9.2% CAGR across the 2026–2032 window, reaching an approximate USD 2,234 Million by 2032.

Polyimide Tape (Kapton Tape) Market

That trajectory is both rapid and uneven: growth is concentrated where high‑temperature masking, EMI shielding and advanced electrical insulation intersect with high‑value end markets (semiconductors, EV power electronics, aerospace). The net effect for 2026 is that manufacturers and suppliers alike must treat polyimide tape not as a static sourcing item but as a strategic input whose availability, specification and cost will materially affect product performance and gross margins.

Polyimide Tape (Kapton Tape) Market

Why This Study Matters for 2026 Decisions

- Procurement Risk & Cost Pass‑Through: Rising polyimide resin inputs and concentrated processing assets mean procurement teams must redesign sourcing strategies; fixed, short‑term buying is likely to expose firms to volatility and capacity squeezes.

- Product Roadmaps & Differentiation: Innovations in adhesive chemistry and film formulations are yielding tape variants that enable higher temperature tolerance, lower outgassing and better EMI management — features that can unlock premium pricing in semiconductor and aerospace BOMs.

- Capacity Planning & Investment Timing: Large incumbents are expanding capacity in response to demand; buyers and potential entrants must time investments to avoid overcapacity or being late to market.

- Regulatory & Supply‑Chain Resilience: Export control updates and tightened trade rules introduced in 2024–2025 alter cross‑border access to certain aromatic polyimides and related processing technology — a direct input into risk assessments and onshore/nearshore strategies.

- M&A and Partnership Opportunities: With the market exhibiting moderate concentration (CR3 ~45%, CR5 ~65%), there is room for bolt‑on acquisitions to gain technical edge, extend distribution or secure strategic materials.

What the Full Report Delivers (Practical, Actionable Content)

PW Consulting’s full market study is built for executives and functional leaders who need executable intelligence rather than academic summaries. The report includes:

- Comprehensive market sizing and validated forecasts (2020–2032) with scenario sensitivities to raw material price shocks, export control stressors, and accelerated EV adoption curves.

- End‑market demand mapping and technology‑led segmentation (masking, electrical insulation, high‑temperature, double‑sided, etc.), with use‑case performance thresholds.

- Supply‑chain and capacity map, including global conversion facilities, lead times, and long‑lead raw material sources.

- Competitor benchmarking, covering product portfolios, channel strategies, recent investments and go‑to‑market positioning for key providers.

- Regulatory impact assessment and compliance playbooks for procurement, R&D and export control functions.

- Commercial playbooks: pricing strategy models, contract language templates for long‑lead procurement, and a supplier qualification checklist tailored to high‑reliability industries.

- Investment cases and M&A screens, including NPV sensitivities and integration risk cushions for potential bolt‑ons in adhesives, film conversion and distribution.

- Practical next steps and a 90‑day action plan for suppliers, OEMs and private equity investors entering or expanding in the segment.

Competitive Landscape — Who Matters and Why

The polyimide tape market blends legacy chemical majors, specialty tape manufacturers and nimble niche suppliers. Market concentration shows meaningful market share at the top end (CR3 ~45%, CR5 ~65%), indicating leaders exert strong influence on pricing, technology benchmarks and capacity dynamics.

- DuPont (Wilmington, DE) — A strategic bellwether: DuPont’s Kapton brand and capacity expansions (notably a large investment in Ohio completed in early 2024) signal continued emphasis on scale and integrated resin–film value chains. For buyers, DuPont’s moves imply both potential supply stability at scale and an imperative to validate alternative sources if dependence is concentrated.

- 3M Company (St. Paul, MN) — Technology and channel power: 3M leverages adhesive chemistry and distribution reach; a late‑2025 high‑performance product launch for semiconductor masking demonstrates the company’s ability to translate R&D into rapid product refreshes. Competitors and customers should watch 3M’s specs as a de‑facto market standard for high‑temperature masking.

- Nitto Denko (Osaka, Japan) — Targeted specialization: With recent production line expansions in Asia‑Pacific for EV power electronics and EMI shielding, Nitto focuses on high‑growth verticals where performance tolerances are premium. Strategic partners in the EV supply chain may find collaboration opportunities for co‑development.

- Saint‑Gobain, Scapa, Fralock and regional specialists — Differentiation via niche capabilities: These players compete on adhesive systems, converter services, and certifications for aerospace/defense. Their agility can be an advantage for OEMs needing custom roll sizes, traceability, or qualification support.

- Distributors and pureplay suppliers (CS Hyde, KaptonTape.com, TapeCase) — Channel and convenience: These firms play a critical role in short‑run supply, kitting and ESD‑safe solutions, particularly for contract manufacturers and repair/servicing markets.

Recent corporate actions underline the market’s structural shifts: DuPont’s capacity expansion in 2024, Nitto Denko’s Asia‑Pacific line augmentations in early 2025 targeted at EV power electronics, and 3M’s late‑2025 product introduction aimed at semiconductor fabs. These moves illustrate how both demand signals (EVs, semiconductors) and supplier strategies (scale, specialization, product innovation) are reshaping the competitive map in real time.

Regulatory and Raw‑Material Dynamics: The New Normal

Two non‑market forces are materially reshaping strategic thinking in 2026:

- Raw‑material cost pressure: High costs for aromatic polyimide monomers and specialty solvents mean tape production is exposed to ingredient price swings. Price volatility compresses margins for converters and complicates multi‑year supply contracts.

- Export controls and trade policy: A stream of updates across 2024–2025 — including revised export control lists and tightened rules affecting aromatic polyimides, film processing technologies and semiconductor‑related materials — creates potential for supply disruptions and compliance costs. Companies must treat regulatory monitoring and legal‑technical alignment as operational necessities, not back‑office functions.

For 2026 planning, build scenarios that explicitly model supply interruptions, re‑routing costs for nearshoring, and the time to qualify alternate resin sources. Failing to do so risks production pauses that are expensive and brand‑damaging for high‑reliability customers.

Recommended 2026 Playbook — Tactical Moves with Strategic Impact

- Implement a two‑pronged procurement strategy: secure long‑term agreements with prioritized suppliers for core grades while maintaining spot access through distributors for specialty variants.

- Prioritize qualification of at least one alternative supplier per critical film/adhesive spec within 12 months; validate through joint pilot runs.

- Accelerate R&D collaboration or licensing for adhesive chemistries that enable higher temperature stability or lower outgassing, to capture premium OEM contracts.

- Model price pass‑through scenarios and update contract templates with fuel‑and‑feedstock clauses tied to transparent indices for resin input costs.

- Pursue targeted M&A or JV opportunities to secure conversion capacity in strategic geographies, particularly where export controls or logistics create supply risk.

- Stand up an export‑control and sanctions program with legal and technical reviewers to reduce classification ambiguity and approval lead times.

- For private equity and corporate development teams: prioritize targets with converter scale, proprietary adhesive IP or embedded positions in high‑value end markets (semiconductor, aerospace, EV power electronics).

Next Steps and How PW Consulting Can Help

PW Consulting’s full Polyimide Tape (Kapton Tape) Market report contains the granular market segmentation, supplier scorecards, proprietary cost models and the scenario matrices referenced in this primer. If your 2026 plans hinge on securing supply, launching differentiated tape‑enabled products, or evaluating M&A in this space, the full report provides the detailed intelligence and executable roadmaps required for confident decision‑making.

Contact PW Consulting to obtain the full report and a tailored briefing: we will walk your cross‑functional team through the demand models, supplier heatmaps and a 90‑day tactical plan aligned to your strategic priorities.

For detailed analysis of this topic, please visit the official page:Polyimide Tape (Kapton Tape) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com