Advanced Semiconductor Fabrication and Process Innovation Propel Etch Equipment Market Through 2034

Fitness |

2026-06-18 05:49:05

As global manufacturers confront changing consumer preferences, tighter regulation, and volatile feedstock markets, the thickener market is entering a phase where strategic clarity will determine winners and laggards. Our PW Consulting Thickener Market study — built on a 2025 base year and a 2026–2032 forecast horizon — quantifies this transformation. The market, which registered sustained expansion through 2020–2025 and reached a multi-billion USD scale by 2025, is projected to continue expanding at a compound annual growth rate of 5.8% across the forecast period. By 2032 the sector’s addressable value is materially larger than in 2025, underscoring both volume-driven demand and price / mix improvements driven by premium, sustainable formulations.

Thickener Market

Strategic timing: 2026 is a pivot year for investment cycles. Many incumbent producers completed pandemic-era capacity rationalizations by 2024–25 and left a narrow window for new entrants or capacity upgrades to influence pricing and availability through 2032.

Thickener Market

Regulatory inflection points: Across major markets regulators are accelerating adoption of biodegradable and bio-based thickeners while increasing scrutiny of non-biodegradable polymers. These shifts are changing product acceptance criteria in food, personal care, and industrial end-markets and raising the cost of non-compliant waste streams for producers and formulators.

Thickener Market

Raw material and input volatility: Feedstock pressures are real and immediate — Q1 2026 price movements for key biopolymers have pushed procurement teams to re-evaluate supplier strategies and pass-through clauses in commercial contracts. Short-term raw material spikes and longer-term supply tightness will affect margins and product selection through the next investment cycle.

Concentration and competitive dynamics: The industry is moderately concentrated; the top-tier suppliers collectively control a significant share of global demand, creating both scale advantages and opportunities for niche players to exploit unmet formulation needs.

Robust market architecture — a transparent methodology linking macro demand drivers to end-use modelling across the 2020–2032 horizon, with scenario-led forecasts and sensitivity ranges for commodity and premium segments.

Actionable commercial playbooks — go-to-market options by customer archetype (food OEMs, beverage formulators, personal care brands, industrial users), negotiation levers, and pricing strategies tuned to 2026 market realities.

Supplier and input risk matrix — forward curves and stress tests for key feedstocks, plus procurement hedging templates to protect margins against volatility.

Regulatory and sustainability roadmaps — mapped requirements across major jurisdictions, compliance cost scenarios for non-biodegradable polymers, and an implementation timeline for transitioning formulations to meet evolving standards.

Investment and capacity planning tools — payback models, utilization gap analysis, and brownfield vs greenfield decision frameworks calibrated to mid-term demand growth.

Competitive benchmarking — capability heatmaps, product-portfolio positioning, and M&A target screens based on technology, geography, and customer access. High-level concentration metrics are provided to inform consolidation strategies and partnership targets.

Commercial intelligence deliverables — Excel modelling packs, negotiation playbooks, and a prioritized list of commercial pilots (formulation trials, co-development partnerships) designed to be executed within 6–12 months.

Shift to bio-based and clean-label: Consumer demand and regulatory nudges have elevated bio-based thickeners from niche to mainstream in many food and personal care segments. Companies that can validate biodegradability and supply-chain traceability will command premium positioning.

Input cost pressure and supply chain resilience: Biopolymer prices and logistics costs are creating short-term margin stress. These pressures make vertical integration, contract manufacturing partnerships, and multi-sourcing strategies immediate priorities for procurement teams.

Industrial and mining applications driving capex: Operational improvements in sectors such as mining and wastewater continue to spur demand for engineered thickener systems, where performance and lifecycle costs—rather than unit price—dictate procurement.

Decarbonisation and manufacturing upgrades: Recent facility upgrades by leading producers demonstrate a clear trend — investments are targeting both energy efficiency and process emissions. Such projects materially reduce long-term operating costs and support sustainability claims in customer tenders.

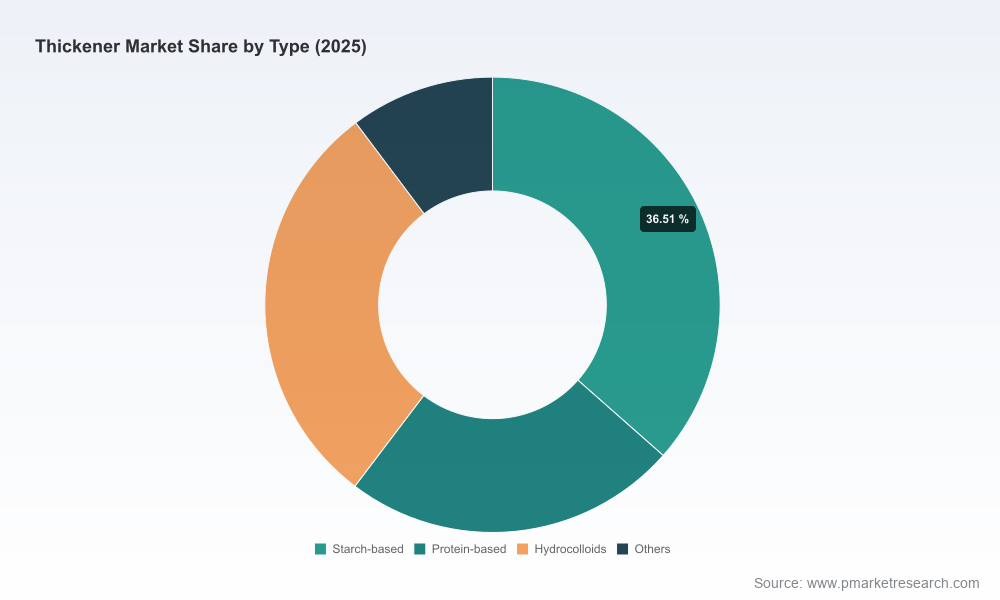

The market is shaped by a mix of large ingredient suppliers, specialty rheology firms, and chemical majors. Leading names cover the full spectrum from plant-based starches and hydrocolloids to synthetic polymers and engineered cellulose ethers. High-level positioning is as follows:

Cargill, Incorporated (Wayzata, MN) — broad hydrocolloid and starch portfolio with emphasis on clean-label and plant-based options for food and beverage customers; strong customer intimacy and formulation support.

Ingredion Incorporated (Westchester, IL) — deep capabilities in starch and fermentation-derived thickeners, with a strategic focus on texture innovation for food and personal care segments.

Archer Daniels Midland (ADM) (Chicago, IL) — scale supplier of starch and corn-derived thickeners; competitive in price-sensitive industrial applications where raw-material integration pays.

Kerry Group (Tralee, Ireland) and Tate & Lyle (London) — strong in hydrocolloids, pectin, and specialty plant-based thickeners; both emphasize clean-label and functional co-creation with food OEMs.

CP Kelco (Atlanta, GA) — specialist in xanthan, gellan, and carrageenan with leadership in technical applications and recent investments in decarbonisation of pectin facilities.

Chemical and polymer majors such as BASF, Dow, and DuPont — supply synthetic polymers, cellulose ethers and acrylic thickeners for industrial, paints & coatings, and specialty personal care markets; focus on performance and regulatory compliance.

Specialty rheology players like Ashland, AkzoNobel, and Elementis — target product differentiation through formulation science, rheology modifiers, and application engineering services.

Together, the top three and top five firms control a meaningful portion of global demand, creating a market structure where scale, formulation capability, and regulatory readiness are decisive competitive advantages.

Decarbonisation and facility upgrades: Industry players have accelerated capital programmes to reduce emissions and strengthen process efficiency — an operational differentiator in tenders that emphasize lifecycle impact.

New product introductions for niche and small-scale applications signal diversification of revenue streams beyond conventional food/beverage channels.

Operational improvements at large mining and industrial sites continue to increase demand for engineered thickening solutions, reinforcing the need for partnerships between technology providers and end-users.

Regulatory and raw-material signals (including notable price movement in key biopolymers and faster adoption of biodegradable alternatives in certain regions) demand immediate scenario planning by procurement and R&D teams.

Embed sustainability as a product differentiator: Move beyond compliance checklists to demonstrate validated lifecycle benefits for bio-based thickeners across the supply chain.

Hedge and diversify feedstock exposure: Implement multi-sourcing, strategic inventories, and supplier partnerships to blunt price shocks and secure continuity for high-priority SKUs.

Pursue targeted M&A and partnerships: Use bolt-on acquisitions to add formulation capabilities or geographic access where scale barriers are high and lead times for greenfield capacity are prohibitive.

Reconfigure commercial terms: Introduce value-based contracts and risk-sharing mechanisms for customers sensitive to raw material volatility and regulatory transitions.

Accelerate application engineering and co-development: Shorten time-to-market for alternative thickener systems by investing in shared labs and pilot programs with key customers.

The thickener market’s trajectory through 2026 will be defined by how businesses manage the intersection of regulatory pressure, feedstock volatility, and customer demand for cleaner solutions. The sector offers attractive growth, but it requires disciplined strategy: the right mix of product innovation, supply-chain resilience, and commercial agility.

For executives preparing budgets, M&A screens, or product roadmaps for the 2026 planning cycle, the full PW Consulting Thickener Market report provides the granular segmentation, supplier scorecards, and downloadable financial models necessary to convert this strategic imprimatur into executable plans. Access the complete dataset and actionable annexes on our report page to unlock regional splits, application-level forecasts, and ready-to-deploy Excel tools designed for immediate decision-making.

For detailed analysis of this topic, please visit the official page:Thickener Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com