Everything You Need to Know About a Lab Test at Home

Health |

2026-05-20 11:01:18

As global health systems pivot from emergency response to durable, programmatic immunization strategies, the polio vaccine market has entered a period of measured expansion and structural realignment. PW Consulting’s new market study — anchored to base year 2025 with a historical window of 2020–2025 and a forecast horizon through 2032 — translates complex epidemiology, procurement dynamics and supplier evolution into actionable guidance for 2026 corporate strategy. This briefing outlines why the study matters for decisions you will make this year, what high‑level numeric context underpins our analysis, and the practical frameworks contained in the full report. For competitive reasons, the in‑depth segment tables and granular regional breakouts are reserved for the full report online; this preview is designed to surface the strategic implications and highlight the decision levers leaders must prioritize in 2026.

Polio Vaccine Market

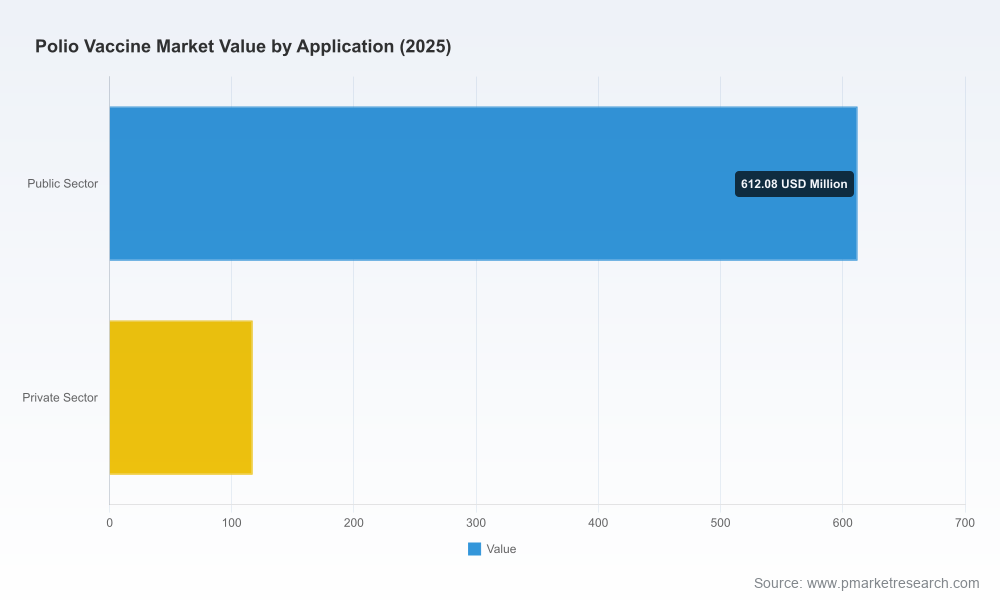

At the aggregate level, the polio vaccine market has demonstrated resilience and steady growth following pandemic‑era disruptions. Our sizing shows recovery from the early 2020s to a base‑year value of approximately USD 729 million in 2025. Under a central scenario the market is projected to expand at a compound annual growth rate of roughly 4.8% over the 2026–2032 forecast period, reaching a market value of about USD 1.01 billion by 2032. These headline numbers reflect a combination of sustained routine immunization demand, catch‑up campaigns in priority geographies, and evolving demand for novel formulations deployed in outbreak response.

Polio Vaccine Market

Three interlocking drivers dominate demand forecasts through 2032: immunization policy updates at the global level, procurement strategies of multilateral agencies, and the pace of eradication‑related campaigns. Notable policy actions include global recommendations to introduce a second IPV dose into routine schedules in remaining countries, and the explicit use of IPV in certain outbreak responses. These decisions materially increase baseline demand and change the cadence of procurement, favouring suppliers capable of multi‑year commitments and diversified vial presentations.

Polio Vaccine Market

At the same time, procurement by UNICEF/Gavi remains a central demand anchor. The weighted average price paid for IPV in UNICEF tenders has been on a downwards trajectory, creating pressure on supplier economics while enabling broader access. Manufacturers and investors must model both price erosion and volume growth when assessing investment cases for expanding fill‑finish capacity or entering new markets.

Recent years have seen meaningful changes in the supply landscape: expansion of WHO prequalified presentations (including multi‑dose and 10‑dose formats), full prequalification of novel OPV2 products for outbreak use, and new regional manufacturing partnerships. These moves increase supplier diversity for multilateral procurement and reduce single‑source risk in several regions. For manufacturers and contract manufacturers, the most consequential operational imperatives in 2026 are capacity flexibility, fill‑finish agility, and cold‑chain resiliency.

Companies considering greenfield capacity or M&A should test assumptions across three scenarios: conservative (slow campaign pace, flat price), baseline (moderate growth aligned with our 4.8% CAGR), and accelerated eradication failure (surge demand for outbreak response vaccines). Fill‑finish partnerships — particularly in regions with constrained cold‑chain infrastructure — offer a lower‑capex route to market, but require robust supply agreements and clear quality assurance pathways to satisfy WHO prequalification expectations.

The competitive set includes legacy multinational vaccine divisions, established vaccine manufacturers in emerging markets, and regional public manufacturers. Our report profiles each major player and assesses their strategic posture along three dimensions: manufacturing breadth (IPV, OPV, nOPV2, sIPV), regulatory footprint (WHO prequalification status and presentation approvals), and go‑to‑market posture (direct supply, partnerships, tender focus, regional manufacturing collaborations).

Recent headline developments — such as new WHO prequalifications for multi‑dose and 10‑dose vials, Sanofi’s regional partnership with Biovac, and Biological E’s elevation to a full nOPV2 manufacturer — have tangible commercial implications: they alter tender dynamics, change the competitive calculus for fill‑finish investments, and affect haste/priority in securing long‑term procurement contracts.

For senior executives evaluating portfolio, capacity, or M&A decisions in 2026, we recommend a focused set of actions:

The PW Consulting full report is structured for commercial and investment decision‑making and includes:

If your organization is considering capacity expansion, entering the polio vaccine market, or bidding for UNICEF/Gavi supply in 2026, immediate priorities are clear: lock in multi‑year offtake visibility, establish or vet regional fill‑finish partnerships, and align product presentations with the fastest‑moving WHO prequalification pathways. PW Consulting’s full report provides the quantitative granularity and implementation checklists to translate those priorities into executable plans. This preview highlights the strategic levers; the full dataset and supplier‑level intelligence are available through our report portal for teams preparing competitive bids, investment memoranda, or tender strategies in 2026.

For access to the complete dataset, downloadable models, and supplier‑level appendices (including the segment and regional breakdowns referenced above), please consult the PW Consulting Polio Vaccine Market report on our website.

For detailed analysis of this topic, please visit the official page:Polio Vaccine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com