How Much Time Can AP Automation Really Save?

Other |

2026-07-06 09:05:39

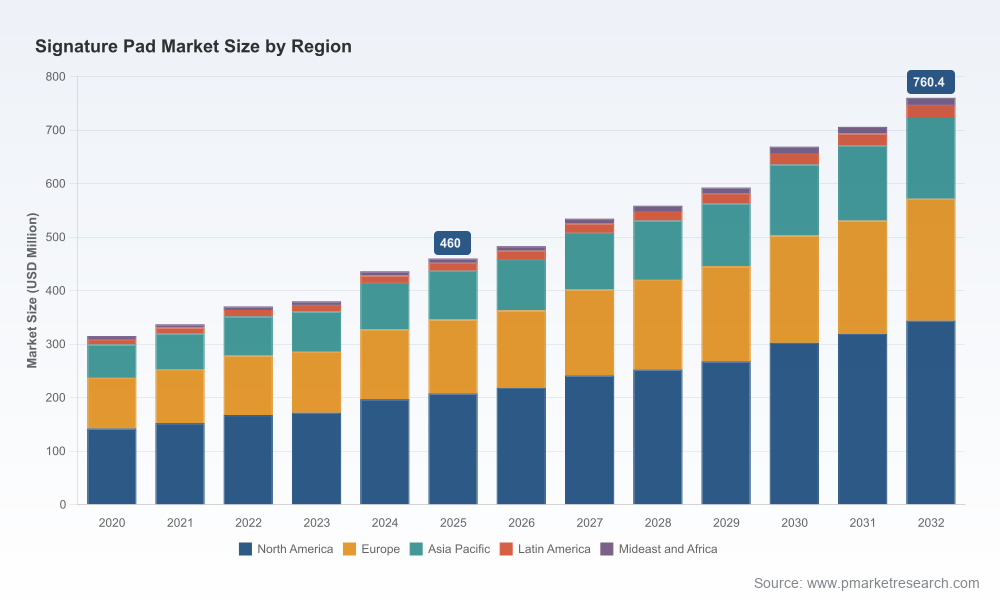

As organizations accelerate the digitization of front‑line interactions—patient intake, point‑of‑sale transactions, insurance onboarding and government services—the humble signature pad has reemerged as a mission‑critical endpoint. PW Consulting’s Signature Pad Market research (base year 2025) illuminates how buyers, vendors and investors should position themselves in 2026 and beyond. Our analysis shows the global market grew from roughly USD 315 million in 2020 to USD 460 million in 2025, and is projected to expand at a compound annual growth rate (CAGR) of 7.48% through the 2026–2032 forecast window, reaching approximately USD 760 million by 2032. For leaders making procurement, product and investment decisions in 2026, the implications are clear: hardware matters, integration matters more, and timing matters most.

Signature Pad Market

Operational ROI trumps reimbursement headlines. Federal updates in 2025 did not introduce new CPT, HCPCS or DRG codes tied to signature capture, so near‑term adoption will be driven by operational efficiency, compliance risk reduction and patient/consumer experience gains rather than new billing pathways.

Signature Pad Market

Regulatory clarity reduces technical uncertainty. The FDA has not mandated a specific electronic signature method for clinical consent processes; this creates latitude for health systems and device suppliers to compete on workflow, integration and infection‑control features rather than on narrow regulatory compliance claims.

Signature Pad Market

Security, hygiene and integration are primary purchase criteria. Hospitals and pharmacies will prioritize devices that can be disinfected safely, integrate with electronic health records (EHRs) and deliver tamper‑resistant data captured in real time. These preferences shape product roadmaps and procurement frameworks.

Scale and steady CAGR mean predictable but competitive growth. A 7.48% CAGR across the 2026–2032 period signals a market that rewards incremental innovation, cost optimization and strategic partnerships over disruptive, single‑bet plays.

Market sizing and trajectories: a validated historical series (2020–2025) and scenario‑based forecasts for 2026–2032 that support budget planning and portfolio prioritization.

Buyer personas and procurement playbooks tailored to healthcare, finance, retail, government and insurance buyers—covering RFP language, evaluation criteria and service‑level requirements.

Vendor scorecards and competitive positioning: qualitative and quantitative measures of product robustness, SDK maturity, integration footprint, distribution channels and compliance posture.

Total cost of ownership (TCO) models and sensitivity analysis that capture acquisition, integration, lifecycle maintenance, consumables (including approved disinfectants) and end‑of‑life replacement scenarios.

Technology and product roadmaps with a focus on usability, antimicrobial materials, display durability, encryption standards and mobile convergence strategies.

Commercial go‑to‑market playbooks for OEMs and distributors that cover channel management, service offers, certification strategies and pilot-to-scale templates.

Our analysis profiles incumbents and niche players to help buyers and partners identify gaps and opportunities without overemphasizing market share mechanics. Highlights:

Topaz Systems (Simi Valley, CA) — well known for durable electronic signature capture pads built for clinical front desks. Their product line emphasizes infection control features and deep EHR integration, making them a frequent choice where hygiene protocols and interoperability are non‑negotiable.

Wacom (Japan) — offers high‑end color and monochrome devices with robust LCDs and hardened glass. Wacom’s strength is in premium durability and OEM relationships where display quality and longevity are prioritized for patient consent and retail scenarios.

Scriptel Corporation (Columbus, OH) — recognized for reliable, widely compatible signature pads adopted across healthcare settings. Scriptel’s value proposition centers on straightforward integration and cleaning protocols suitable for clinical environments.

Evolis (France) — focuses on compact pads with secure, high‑resolution capture and encryption. Their product set appeals to medical and regulated environments that require lightweight, secure endpoints.

Selectum LLC (USA) — a distributor and integrator that brings stock availability, SDK support and logistics advantages to buyers, particularly in the U.S. market.

These firms illustrate common competitive vectors: hardware robustness, SDK and EHR integration maturity, supply chain responsiveness and infection‑control suitability. The full report contains vendor heat maps and decision matrices to support supplier selection without disclosing proprietary market splits here.

Procurement: Standardize on a small family of devices across facilities to minimize integration variance and servicing complexity. Use unit TCO models to justify multi‑year contracts that include spare‑parts, disinfectant protocols and firmware update guarantees.

Product development: Prioritize antimicrobial or easily disinfectable surfaces, sealed electronics, and hardened touch surfaces. Address a practical cleaning protocol—many hospital users require EPA‑registered wipes such as those listed in vendor user guides—and design for compatibility with those agents.

Integration: Build or acquire robust SDKs and middleware that directly map signature capture into EHRs and back‑end systems with secure, auditable logs. Interoperability will be the top differentiator when FDA does not enforce a single technical approach.

Commercial: For OEMs and distributors, lean into channel partnerships with EHR vendors and managed service providers. Offer subscription‑based hardware services with defined cleaning/certification schedules to convert capital spend into predictable operational revenue.

Risk management: Model scenarios that include material cost inflation and supply chain constraints; ensure sourcing alternatives for key components to defend margins during cyclical raw material shifts.

Regulatory shifts remain a wildcard. While current guidance grants flexibility in method selection, state or institutional mandates for authenticated electronic consent could change procurement priorities rapidly.

Cybersecurity events. Signature capture devices that fail to meet evolving cryptographic expectations or that expose APIs may become commercial liabilities. Plan for secure firmware update paths and certified encryption.

Hygiene expectations. Institutional buyers demand validated cleaning regimens. Vendors that document compatibility with EPA‑registered wipes and provide cleaning-friendly designs will win procurement decisions.

Competitive substitution from mobile devices and secure tablet apps. Where operational workflows permit, mobile capture may cut into dedicated hardware sales, emphasizing the importance of integration, durability and infection control as hardware differentiators.

Week 1–2: Convene a cross‑functional decision forum (IT, procurement, clinical ops, security). Align on top three business outcomes (efficiency, compliance, experience).

Week 3–6: Run two rapid pilots—one clinical (hospital front desk) and one commercial (retail/finance)—using devices from different vendor archetypes outlined above. Capture integration effort, cleaning SOPs and user feedback.

Week 7–10: Model TCOs for each pilot outcome, incorporating lifecycle cleaning, spare parts, SDK licensing and integration costs.

Week 11–12: Negotiate a pilot‑to‑scale contract with preferred vendor(s) that includes SLA, software updates and a field cleaning/certification plan.

PW Consulting’s full Signature Pad Market report provides the granular segmentation, regional splits, application breakouts and vendor scorecards necessary to execute these steps with confidence. We deliberately keep those segment tables and vendor share figures off this trailer to protect the report’s strategic value; if you are preparing a 2026 procurement, product roadmap or investor memo, the full dataset and decision tools will materially shorten your time to value.

To obtain the complete report, including downloadable TCO models, vendor heat maps and regional outlooks that support negotiation and product planning, please visit our web page (link available in the release) or contact your PW Consulting representative. In a market growing steadily at an above‑average rate, the companies that pair hardware durability with seamless, secure integration will capture the most durable share of the projected upside.

For detailed analysis of this topic, please visit the official page:Signature Pad Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com