Spintronics Market: Insights and Competitive Analysis

Other |

2026-04-08 08:35:50

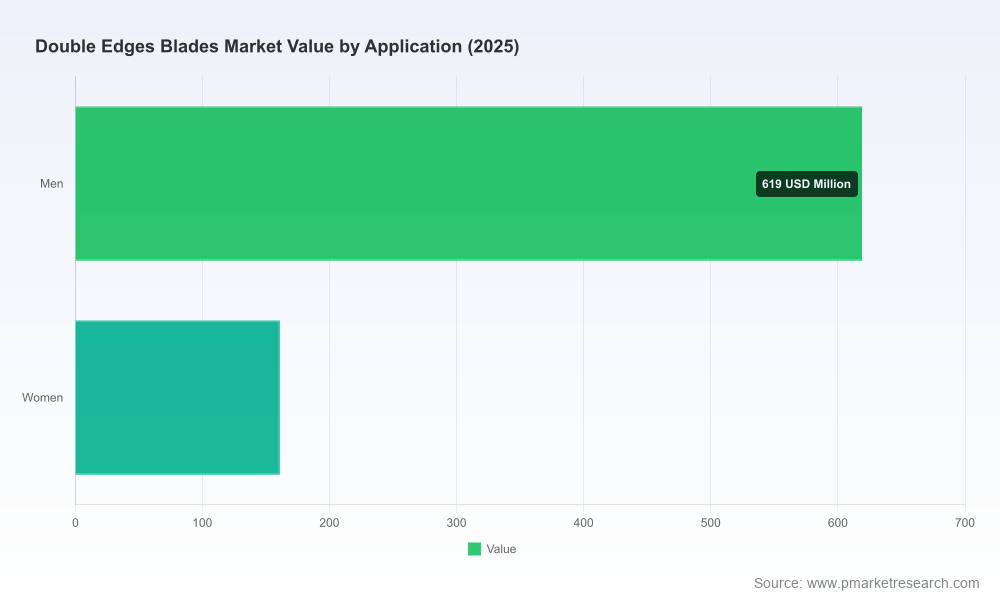

The double edges blades market has entered a decisive phase. After a period of steady recovery and structural change, the global market reached approximately USD 780 million in 2025 and is projected to accelerate from 2026, tracking a compound annual growth rate (CAGR) of 9.0% across the 2026–2032 forecast window. By the end of that horizon the market is expected to approach USD 1.48 billion, driven by a blend of premiumization in mature markets, renewed interest in traditional wet-shaving among younger cohorts, and regulatory-led shifts in packaging and materials. For executives planning investments, portfolio pivots, or go-to-market changes in 2026, these topline dynamics create both urgency and opportunity: the growth runway is clear, but success will depend on deep operational and regulatory readiness rather than simple volume playbooks.

Double Edges Blades Market

Our Double Edges Blades Market report is built as an operator’s handbook for 2026 decision-making. It contains:

Double Edges Blades Market

The market showcases a duality: established global brands with scale and marketing muscle coexist with highly specialized, smaller manufacturers that command strong loyalty among wet-shaving enthusiasts. Market concentration metrics underline this dynamic: the top three competitors capture roughly a quarter of the market (CR3 ~24.6%), and the top five only modestly more (CR5 ~26.2%). This distribution signals a fragmented ecosystem with room for both scale consolidation and niche differentiation.

Double Edges Blades Market

Practically, this means:

Key names that shape competition and capability sets include legacy champions with mass-market penetration (Gillette, BIC, Schick), premium and technically focused manufacturers (Feather Safety Razor Co., Kai Group, Merkur/Mühle), and high-volume producers and suppliers across Asia (Dorco, Super‑Max, Treet, Xirui). Each archetype invites a different strategic response—acquihire for technical IP, co-manufacturing to scale, or targeted premiumization campaigns.

Regulation is a material driver of 2026 strategy. In key markets, razor blades fall under medical device classifications that impose registration and labeling requirements. Compliance with ISO 3558 safety testing, CE marking where applicable, and tightening packaging requirements in the EU (aimed at reducing non-recyclable plastic by 2030) are already forcing product and packaging redesigns.

For product teams and procurement, the takeaways are straightforward: design for compliance as a default, contractually secure traceability of steel and coatings, and prioritize packaging vendors who can deliver recycled or mono-material solutions. Delays in certification or misaligned packaging changes can materially slow new product introductions or create costly repackaging cycles.

Stainless steel and coating technologies remain the primary input factors that determine unit economics, performance claims, and shelf positioning. Manufacturers with robust metallurgical know-how and ISO-certified processes command a price premium and lower reclamation/reject rates. In 2026, buyers should pursue a dual-track sourcing strategy: secure contractual coverage for core stainless suppliers to stabilize costs, while qualifying smaller specialist coaters and finishing houses to support premium SKUs and limited editions.

Market activity at global trade events is an immediate indicator of sourcing momentum — leading exporters and contract suppliers continue to use trade fairs to establish channel relationships and test new coatings and packaging formats. For commercial teams, trade-show participation and supplier audits in 2026 should be treated as high-priority sourcing windows.

This preview is designed to orient C-suite and business-unit leaders on the strategic levers that will matter in 2026. The full PW Consulting Double Edges Blades Market report contains the granular segmentation tables, regional and application-level splits, supplier shortlists, and downloadable financial models you need to operationalize the playbook. If you are preparing a budget, revising your sourcing strategy, or evaluating acquisitions in 2026, the full dataset and scenario tools will convert this strategic preview into executable initiatives.

For teams that require an accelerated roll-out, we also offer a 60‑day implementation concierge to map compliance, supplier contracting, and go-to-market pilots to your existing product-development cadence.

For detailed analysis of this topic, please visit the official page:Double Edges Blades Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com