Chlorhexidine Gluconate (CHG) Solution Market: Strategic Outlook for 2026 Decision‑Making

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused executive narrative intended to orient corporate leadership for decisive action in 2026. Our proprietary market model—anchored on a 2025 base year and a historical window covering 2020–2025—shows a steady, resilient CHG solutions market expanding from the low‑hundreds of millions in 2020 to a mid‑hundred million base in 2025, with projections indicating a continuation of this momentum through the 2026–2032 forecast period. The modeled compound annual growth rate (CAGR) for the forecast window is 5.85%, and our long‑range scenario set suggests a market approaching the high hundreds of millions by 2032. These headline dynamics sit atop a market with moderate concentration: the top three suppliers account for roughly one‑third of volume, while the top five collectively approach the mid‑forties percent — a structure that creates clear opportunities for challengers and consolidation plays alike.

Chlorhexidine Gluconate (CHG) Solution Market

Why this research matters for 2026

Chlorhexidine Gluconate remains a frontline antiseptic across clinical and consumer settings. In 2026, leaders will need to make investment, sourcing, and portfolio choices against a backdrop of: regulatory flux in Europe, episodic supply and quality events, active M&A and product innovation, and persistent cost‑management pressures in procurement channels. Our study synthesizes these flows into pragmatic, decision‑grade insight: not only what the market looks like on paper, but how operational levers—manufacturing capacity, distribution partnerships, regulatory readiness, and product differentiation—translate to market share and margin trajectories.

Chlorhexidine Gluconate (CHG) Solution Market

Market dynamics shaping strategic priorities

- Growth driven by infection‑prevention momentum. Continued prioritization of surgical site infection mitigation, expanded procedural volumes in many healthcare systems, and increasing adoption of CHG in preoperative, peri‑operative and peri‑catheter care underpin steady demand growth.

- Regulatory and quality risk as a strategic constraint. Recent regulatory action in Europe that restricts certain alcoholic CHG formulations, as well as high‑visibility product recalls and manufacturing discontinuations, have created near‑term access and reputational risks for both suppliers and buyers.

- Supply chain concentration and API dynamics. A small number of specialized manufacturers and API suppliers drive critical upstream capacity. Strategic partnerships or vertical integration with API and contract manufacturing specialists materially de‑risk supply and can yield margin improvement.

- Consolidation and product innovation. Accelerated deal activity and product launches signal that incumbents are seeking to secure channel control and broaden differentiated offerings (for example, CHG‑impregnated dressings and alternative delivery forms), creating windows for bolt‑on acquisitions and platform plays.

- Price and reimbursement pressure. Public and private payers continue to scrutinize antiseptic pricing. Observed retail and payer benchmarks suggest meaningful sensitivity among purchasers, which feeds into contracting strategies and product positioning.

Competitive landscape — what incumbents and new entrants must know

The competitive topology is a mix of specialist chemical manufacturers, large diversified medical suppliers, and firms that straddle consumer and clinical channels. Key strategic profiles we track:

Chlorhexidine Gluconate (CHG) Solution Market

- Contract manufacturers and API specialists. Established contract manufacturers with deep CHG experience are vital nodes for companies that prioritize speed‑to‑market without heavy capital investment. The largest API suppliers in this space are strategic allies for securing upstream continuity and pricing stability.

- Large diversified medical and infection‑control players. Firms with broad infection‑prevention portfolios leverage channel breadth and complementary product sets to accelerate adoption—especially when pairing CHG solutions with application devices or consumables.

- Regional producers and exporters. Manufacturers based in high‑capacity production geographies provide both cost and supply advantages for global buyers, but require rigorous quality governance and regulatory alignment when scaling to stringent markets.

Recent moves by several firms illustrate the practical implications of these archetypes. Strategic acquisitions and portfolio reconfigurations are expanding scale in high‑growth geographies and securing product lines that complement CHG solutions. Product innovations—such as CHG‑impregnated dressings designed for mobility and convenience—signal where clinical demand is evolving. Conversely, discrete events (product recalls and licensed product discontinuations) highlight persistent vulnerabilities: when a trusted SKU is removed from the market, downstream buyers feel the pain immediately.

Strategic implications and recommended actions for 2026

Leaders need a prioritized, time‑phased playbook. Below are high‑impact moves we counsel, structured for immediate, medium, and strategic horizons.

- Immediate (0–90 days): Run a rapid supply‑chain audit. Identify single‑source exposures to critical CHG grades and API suppliers. Establish contingency agreements with at least two qualified contract manufacturers and initiate quality audits where recall or contamination risk is credible.

- Near term (3–12 months): Revisit product portfolio choices through a value lens. Differentiate where possible via delivery form, packaging, and adjacent product bundling (e.g., pairing antiseptic solutions with device solutions). Leverage observed payer price benchmarks to negotiate outcome‑linked contracts or volume tiers.

- Medium term (12–36 months): Pursue selective M&A or JV transactions to secure upstream capability or to fill product gaps—particularly where regulatory change has created vacuums in certain formulations. Invest in non‑alcoholic or alternative CHG formulations to hedge regulatory variability, and accelerate clinical evidence generation to support adoption in procedural protocols.

- Strategic (36+ months): Consider vertical integration for critical APIs or enter long‑term supply partnerships with capacity reservation clauses. Build an evidence generation engine (real‑world data, KOL engagement) to support premium positioning and counter commoditization pressures.

What our report delivers — operational, not ornamental

Our full market study is intentionally tactical. It contains the following components designed for immediate application by commercial, procurement, and corporate development teams:

- Validated market sizing and a transparent forecasting model (base year 2025; forecast 2026–2032) with scenario variants reflecting regulatory shocks, accelerated consolidation, and demand‑side surges.

- Regulatory tracker and compliance playbook that maps current restrictions and likely future vectors in major regulatory jurisdictions.

- Supply‑chain heatmaps and a roster of qualified contract manufacturers and API suppliers, including risk‑scoring and recommended contractual clauses for resilience.

- A competitive playbook that profiles incumbent strategies, product pipelines, and M&A targets, supported by recent development timelines and impact assessments.

- Commercial tools: pricing benchmark sets, procurement negotiation scripts, and go‑to‑market tactics for differentiated CHG products across clinical and consumer channels.

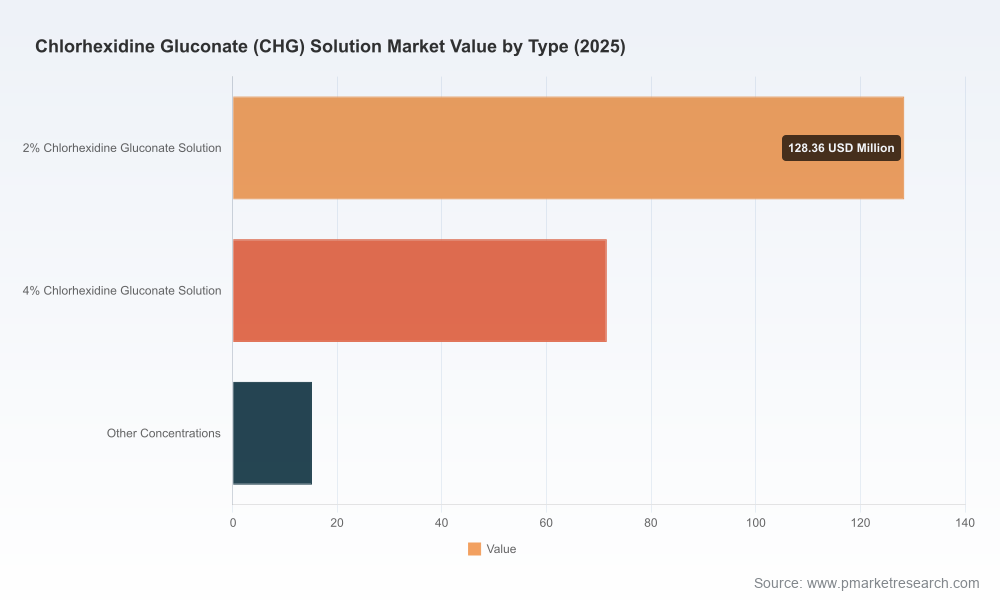

Importantly, while this executive overview highlights trends and strategic imperatives, granular segmentation — including the detailed splits by region, concentration by formulation strength, and application‑level demand curves — are reserved for the full report. That granular intelligence is the foundation for optimized investment decisions and is available through our publication portal.

Scenario thinking: two plausible 2026 shocks and responses

- Regulatory restriction expansion. If further European or other national authorities impose limits on alcoholic CHG formulations, demand will reallocate rapidly to compliant alternatives. Response: accelerate reformulation programs and pre‑emptive regulatory filings in affected markets.

- Supply disruption at an API node. A contamination event or factory outage at a major API supplier can create acute shortages. Response: invoke contingency contracts, deploy strategic buffer inventory, and prioritize product allocations to high‑value channels through contractual prioritization clauses.

Closing — turning insight into advantage in 2026

The CHG solutions market in 2026 will reward organizations that combine operational rigor with strategic agility. Market size and growth fundamentals are favorable, and the level of market concentration leaves room for both disciplined challengers and acquisitive incumbents to expand. Yet the interplay of regulatory change, supply fragility, and payer pressure means that mere product availability is not sufficient; companies must demonstrate supply reliability, regulatory foresight, and measurable clinical value.

PW Consulting’s CHG solutions market study provides the data architecture, risk diagnostics, and transaction tools to convert those imperatives into executable plans. For teams preparing capital allocation decisions, supply re‑contracts, or product launches in 2026, the full dataset and operational playbooks in our report are designed to shorten the path from insight to impact.

To access the complete analysis, including detailed segmentation, supplier maps, and our downloadable forecasting model, please visit the PW Consulting report page or contact our strategy desk for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Chlorhexidine Gluconate (CHG) Solution Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com