PW Consulting: Viscose Staple Fiber Market to Hit USD 25,900 Million by 2032 at 6.98% CAGR

Other |

2026-07-12 03:43:55

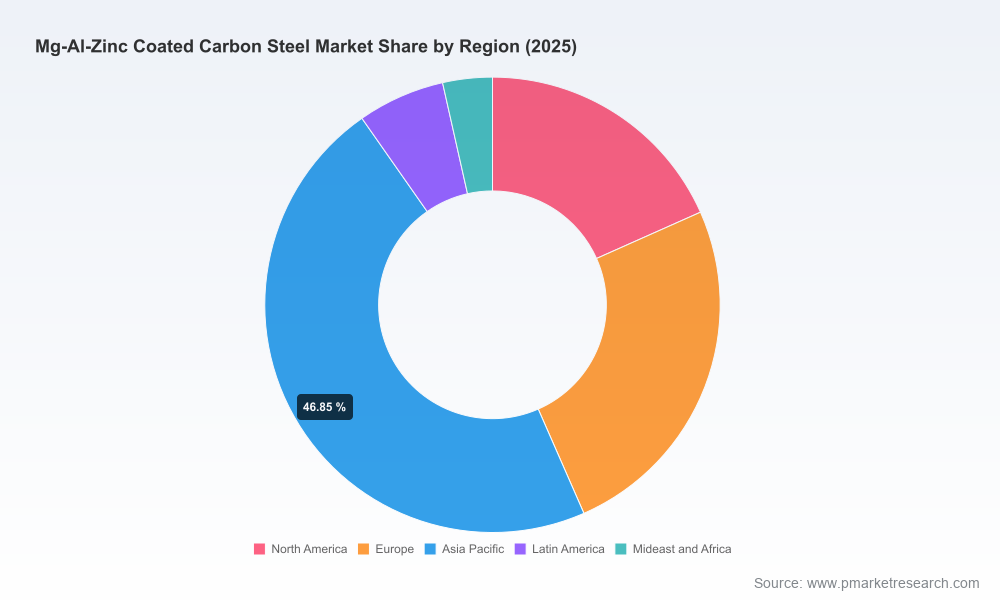

As PW Consulting’s Senior Strategy Consultant and Chief Industry Analyst, I present a focused briefing on the Mg-Al-Zn (magnesium‑aluminum‑zinc) coated carbon steel market that foregrounds the critical strategic choices executives must make in 2026. This is a “trailer” for our full market study: we reveal the high‑value implications, structural dynamics, and actionable guidance drawn from our proprietary modelling, while preserving the granular segmentation and scenario tables for subscribers to the full report.

Mg-Al-Zinc Coated Carbon Steel Market

The Mg‑Al‑Zn coated carbon steel market has transitioned from niche innovation to a mainstream corrosion‑resistant alternative across multiple end uses. On a macro scale, the market expanded from roughly USD 8.3 billion in 2020 to about USD 10.8 billion in our 2025 base year, reflecting steady adoption across construction, automotive and industrial applications. We forecast continued expansion through the 2026–2032 horizon at a compound annual growth rate of about 5.5%, reaching an anticipated market size of approximately USD 15.7 billion by 2032.

Mg-Al-Zinc Coated Carbon Steel Market

Why does this matter for 2026? The market size and mid‑single digit growth profile indicate a maturing industry where volume growth now coexists with increasing emphasis on margin preservation, differentiation through coating performance and formability, and logistics resilience. Companies that calibrate 2026 investments to capture premium applications (e.g., EV body architectures, PV mounting systems, and coastal infrastructure) while hedging commodity and regulatory risk will gain outsized returns.

Mg-Al-Zinc Coated Carbon Steel Market

Concentration and competitive pressure — The market exhibits moderate concentration: our competitive concentration metrics show the top three firms control a meaningful majority share, and the top five expand that dominance. This structure creates both partnership opportunities for scale and squeeze points for independent producers on procurement and downstream pricing.

Raw material exposure — Zinc is the dominant cost driver in coating chemistry, representing an estimated majority of coating material cost. LME zinc price volatility (roughly USD 2,500–3,200/tonne across recent years) combined with fluctuating magnesium and aluminum inputs periodically compresses producer margins and complicates fixed‑price contracts.

Regulatory overlay — Emerging environmental rules, particularly in the EU under evolving Industrial Emissions Directive interpretations, have produced compliance delays that materially affected production volumes in recent years. Simultaneously, trade measures (e.g., tariffs and anti‑dumping probes) continue to reshape cross‑border flows and sourcing footprints.

Product innovation as a differentiation axis — New product introductions emphasize enhanced corrosion resistance and forming performance, targeting EV, renewable‑energy and coastal construction segments. These product features, not just price, are becoming the deciding factor for OEM and specifier selection.

Robust market sizing and validated demand scenarios: historical (2020–2025) reconstruction and three forward scenarios through 2032 driven by end‑use demand, policy shocks, and raw‑material trajectories.

Price and cost modelling: input‑cost pass‑through matrices, zinc price sensitivity analysis, and margin stress tests for integrated mills versus toll‑coating operators.

Supply‑chain risk maps: node‑level supplier concentration, contractual exposure to tariff regimes, and logistics contingency playbooks for near‑term disruption.

Commercial playbooks: go‑to‑market options for premium coated products (segmentation of technical specs, OEM value propositions, and specification migration strategies).

Investment and M&A guidance: prioritized capex opportunities, brownfield vs greenfield tradeoffs, and acquisition screening criteria aligned with concentration dynamics and demand corridors.

Regulatory impact assessment: quantified production impacts from emissions rules, compliance timelines, and recommended mitigation measures (process upgrades, alternative coating formulations, and permitting strategies).

Supplier scorecards and benchmarked KPIs: production cost curves, technology readiness, service levels, and ESG compliance metrics to support sourcing decisions.

The competitive map is dominated by large steelmakers and specialized coated‑steel divisions. Leading firms combine global production footprints with proprietary coating technologies and OEM partnerships. A concise, non‑exhaustive strategic read:

ArcelorMittal (Luxembourg) — Strengths: global scale, integrated supply chain, and recent contract wins with major automotive OEMs. Strategic posture: leveraging scale to secure long‑term platform supply agreements for EVs and mobility platforms.

Nippon Steel (Japan) — Strengths: high‑performance product lines focused on formability and corrosion resistance. Strategic posture: targeting coastal and high‑spec outdoor applications where product performance commands price premiums.

POSCO (South Korea) — Strengths: engineering focus on corrosion resistance and forming; recent strategic partnerships expand technical collaboration for EV bodies. Strategic posture: combining co‑development and volume commitments to penetrate automotive value chains.

Tata Steel, thyssenkrupp, voestalpine, JFE, Nisshin, BlueScope, Salzgitter, Baowu, JSW, and U.S. Steel — Each brings regional leadership, differentiated product portfolios, or scale advantages. Collectively they shape regional availability, technology diffusion and price benchmarks.

Recent corporate moves underscore the market’s direction: product launches that enhance corrosion and formability, capacity expansions in high‑growth markets, and strategic partnerships to accelerate supply for EV and renewable applications. These trends tighten competition in premium segments while opening partnership pathways for suppliers and OEMs.

Procurement and hedging: implement zinc exposure hedges tied to contract structures; transition key supplier contracts to indexed pricing with clear pass‑through thresholds and performance clauses to protect margins during metal price swings.

Product and R&D prioritization: accelerate adaptation of coating chemistries that balance lower zinc content with comparable performance where regulatory pressure exists; fast‑track formability trials for EV body integration.

Capability and footprint decisions: prioritize flexible coating lines near high‑value demand centers that reduce tariff and logistics risk; consider toll‑coating partnerships to de‑risk capital intensity while retaining market access.

M&A and partnerships: target bolt‑on assets that close gaps in coastal corrosion testing, slitting/coating capacity, or regional tariffs exposure. Strategic partnerships (e.g., co‑development with OEMs) can be faster to market than greenfield expansion.

Regulatory preparedness: allocate budget for emission control retrofits and alternative coating R&D; prioritize jurisdictions where compliance timelines risk material supply interruptions.

Commercial and specification strategy: shift commercial conversations from price‑only to total cost of ownership and lifecycle performance; develop pilot programs with OEMs and large specifiers to accelerate adoption.

Raw material shocks: abrupt zinc price spikes or supply disruptions that rapidly compress margins or force price renegotiations.

Trade and policy moves: new tariffs or anti‑dumping actions that require fast reconfiguration of supply chains.

Regulatory compliance: emission rules that delay or curtail output in key production hubs.

Technological substitution: competing coating technologies or surface treatments that undercut Mg‑Al‑Zn value propositions in specific segments.

For executive teams, the 2026 inflection point is clear: scale and product performance matter, but so do supply‑chain agility and regulatory foresight. Our full Mg‑Al‑Zn coated carbon steel study provides the quantitative backbone (historic reconstruction, market sizing to 2032, price sensitivity matrices, and concentration metrics) and the practical playbooks (procurement templates, investment scoring, and regulatory mitigation plans) to inform board‑level decisions.

We have demonstrated the market’s magnitude and growth trajectory here—highlighting a market that has grown from roughly USD 8.3 billion in 2020 to USD 10.8 billion in 2025 and is projected to continue expanding to an estimated USD 15.7 billion by 2032 at a CAGR of about 5.5%—while intentionally withholding full segment tables and granular regional/application breakdowns to preserve the strategic value of the complete analysis. For organizations that need executable recommendations, supplier scorecards, and the exact segmentation data to model 2026 scenarios, the full report contains the necessary proprietary detail.

Engage PW Consulting to translate these insights into prioritized actions: optimize sourcing, de‑risk supply, unlock premium applications, and align capex to the highest‑return opportunities in the evolving Mg‑Al‑Zn coated steel landscape.

For detailed analysis of this topic, please visit the official page:Mg-Al-Zinc Coated Carbon Steel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com