Electro-Medical Devices in Alzheimer?s Treatment Market Industry Report Covering Market Dynamics & Competitive Insights

Health |

2026-05-26 13:33:23

As global industrial and cryogenic systems scale to meet energy transition, carbon capture, and next‑generation gas processing needs, brazed and plate‑fin heat exchangers are at the center of an engineering and commercial inflection. This preview synthesizes the strategic implications from PW Consulting’s full Plate‑fin Heat Exchanger Market study (base year 2025) and shows how executives should translate market dynamics into high‑confidence decisions through 2026 and beyond.

Plate-fin Heat Exchanger Market

Timing: With 2025 established as the base year, our forecast window begins in 2026 — the pivotal planning year for CAPEX cycles, supplier contracts, and standards compliance programs across the industry.

Plate-fin Heat Exchanger Market

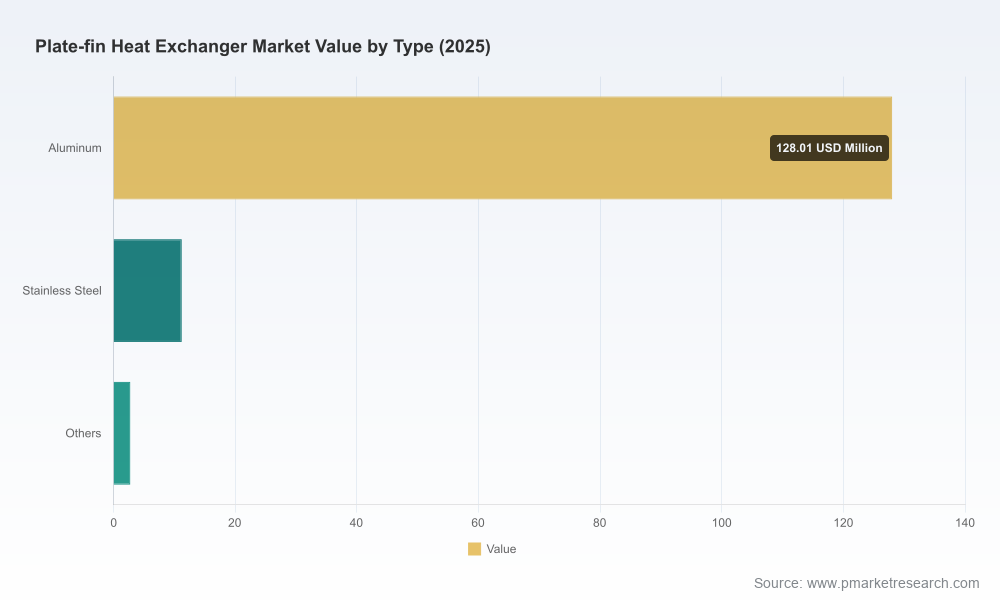

Scale and momentum: The PFHE market has expanded steadily over the last half decade, rising from roughly USD 113 million in 2020 to about USD 142 million in 2025. Our model projects continued expansion through 2032, reaching just under USD 198 million under the central case. The forecast period (2026–2032) embeds a compound annual growth rate of 4.9% — a material underlying trend that should influence capacity planning, inventory strategy, and R&D prioritization.

Plate-fin Heat Exchanger Market

Concentration and competition: Market concentration is meaningful but far from monopolistic — the top three suppliers account for around 30% of the market, and the top five roughly 35%. That profile supports both scale advantages for major OEMs and persistent opportunity windows for challengers via specialization, regional focus, or vertical integration.

Standards and regulatory momentum: ALPEMA’s recent activity — including responses to the 2nd Edition of API 668 and publication of the 4th edition of ALPEMA Standards and associated FAQs — is shifting buyer expectations for integrity management, inspection regimes, and documentation. Compliance is no longer an operational afterthought: procurement, engineering and HSE functions must now bake updated integrity operating windows into specifications.

Raw material dynamics and supply‑chain geography: Aluminium and key component suppliers exert medium influence on PFHE availability. Tariff frictions have accelerated supply‑chain localization and near‑sourcing strategies, especially among manufacturers targeting U.S. and regional buyers. Expect continued capital investment in regional brazing and assembly capacity as manufacturers reduce exposure to cross‑border tariff volatility.

Application tailwinds: Electrification, hydrogen and LNG infrastructure projects, petrochemical modernization, and industrial gas production underpin steady demand. These drivers favor technical differentiation — exchangers that deliver higher effectiveness per unit mass, lower pressure drop, and longer life under cyclic loads command a premium.

Technology and product innovation: Materials science (coatings, corrosion mitigation), advanced brazing techniques, and digitally enabled lifecycle services are the primary innovation vectors. Firms that combine product improvements with service monetization (e.g., predictive maintenance, inspection-as-a-service) will capture outsized margin expansion.

PW Consulting’s full report is designed to be directly actionable for corporate strategy, procurement, and product teams. Key deliverables include:

Demand modeling calibrated to historic 2020–2025 performance and multiple scenarios through 2032, enabling stress‑testing of CAPEX and working‑capital assumptions.

Supply‑side mapping that traces brazing capacity, critical component suppliers, and bottlenecks — including a quantified view of material‑risk exposure and route options for localization.

Vendor benchmarking and playbooks: in‑depth profiles of global incumbents and challengers, including technology positioning, geographic footprints, product families, and decision criteria for partner selection.

Regulatory and standards annex that synthesizes ALPEMA guidance, API updates, and practical compliance checklists tailored to engineering and procurement teams.

Commercial models and pricing framework: a modular template to forecast selling prices, margin sensitivity, and the impact of raw‑material pass‑through mechanisms under different contract types.

M&A and partnership screening: prioritized target lists and integration playbooks informed by capability gaps, cost synergies, and customer access potential.

Operational tools: CAPEX/OPEX benchmarking, expected lead‑time matrices, and sample contractual clauses to mitigate tariff and quality risk.

The PFHE market blends heritage technology providers with diversified heat‑transfer specialists. The full report includes expanded vendor dossiers; below is a concise orientation to the core competitors covered:

Linde Engineering (Munich, Germany) — A leading supplier of brazed aluminum plate‑fin heat exchangers with deep domain experience and a long installed base. Linde’s legacy scale and ALPEMA involvement position it strongly in large cryogenic and industrial projects.

Chart Energy & Chemicals / Chart Industries (La Crosse, Wisconsin, USA) — Known for vacuum‑brazed PFHEs across cryogenic and processing markets, Chart is a major ALPEMA member with strong aftermarket presence in North America.

Kobe Steel, Ltd. (Takasago, Japan) — Produces high‑performance PFHEs for petrochemical, LNG and industrial gas sectors. Technical pedigree and regional supply chains make Kobe Steel a pivotal player in Asia and global EPC programs.

Sumitomo Precision Products (Takarazuka, Japan) — Specialist in aluminum PFHEs for cryogenic and industrial applications with tight quality controls and engineering depth.

Alfa Laval (Lund, Sweden) — A global manufacturer of compact PFHE solutions serving HVAC, refrigeration, food processing and industrial thermal management; strong brand and distribution networks enable broad reach.

Eaton Corporation (Dublin, Ireland) — Supplies custom vacuum‑brazed PFHEs for automotive, aerospace and industrial liquid‑to‑liquid/air systems; differentiated by systems integration capabilities.

These vendors demonstrate the strategic choices available to buyers: contract with large incumbents for scale and global after‑sales, or partner with specialized suppliers to capture performance or regional advantages. The full report contains an expanded SWOT and supplier scorecard to support vendor selection and negotiation strategies.

Prioritize standards alignment now: Integrate ALPEMA 4th edition requirements and API 668 responses into procurement specs and capital project documentation. Delaying compliance integration will increase retrofit and qualification costs later in the project lifecycle.

Hedge material and tariff risk: Implement a three‑tier sourcing strategy — domestic capacity (for critical projects), regional partners (to shorten lead times), and strategic imports with hedged contracts. Consider inventory cushions for long‑lead components while adopting JIT for commoditized parts.

Develop a product‑service monetization pathway: Pilot predictive inspection services and extended warranties on a subset of installed units. These programs reduce downtime risk for customers and create recurring revenue streams.

Align R&D to proven value levers: Focus development resources on corrosion mitigation, brazing reliability under cyclic loads, and exchanger compactness where grams per kW matter. Prioritize incremental performance gains that shorten payback for end users.

Explore bolt‑on acquisitions thoughtfully: Targets that expand brazing capacity, provide regional aftermarket networks, or deliver digital inspection capabilities provide rapid strategic lift. Use PW Consulting’s M&A screening in the report to evaluate targets against integration risk and synergies.

Structure contracts to allocate inflation and material risk: Incorporate escalation clauses tied to aluminium indices and define quality acceptance criteria aligned to ALPEMA guidance to avoid disputes during commissioning.

CFOs — Integrate the market forecast and scenario outputs into three‑year capital planning. The 4.9% forecast CAGR through the decade implies moderate growth; prioritize investments that preserve optionality (scalable cell capacity, modular brazing lines).

CPOs — Reconfigure supplier scorecards to weigh standards compliance and regional capacity more heavily. Negotiate multi‑year supply agreements with performance SLAs tied to ALPEMA‑aligned inspection regimes.

Heads of Engineering — Update procurement specifications and FAT protocols to include ALPEMA 4th edition checks. Use our technical annex to translate standards into test procedures and acceptance criteria.

This preview presents the strategic contours and executable recommendations from the full PW Consulting Plate‑fin Heat Exchanger Market study. To preserve the value of our proprietary work — and to follow our “trailer” principle — detailed segment‑level tables, regional and application breakouts, vendor revenue breakdowns, price curves, and full scenario datasets are available only in the paid report. These granular assets are designed to feed internal financial models and procurement adjudication processes directly.

For executives preparing 2026 plans, the immediate step is to integrate the policy, sourcing, and product recommendations above into Q1 planning workshops. If you require the full data pack (segment tables, company financials, scenario models, and vendor scorecards) to support board‑level decisions, contact PW Consulting to obtain the complete Plate‑fin Heat Exchanger Market report and tailored advisory services. Our analysts can also deliver a short executive workshop to apply the report’s outputs to your portfolio and programs.

In markets defined by standards evolution, material volatility and modular innovation, informed action is the difference between reactive cost mitigation and proactive value creation. This study equips decision‑makers to do the latter in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Plate-fin Heat Exchanger Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com