Anechoic Chamber Industry Expansion Driven by Connected Device Adoption

Other |

2026-05-22 09:35:17

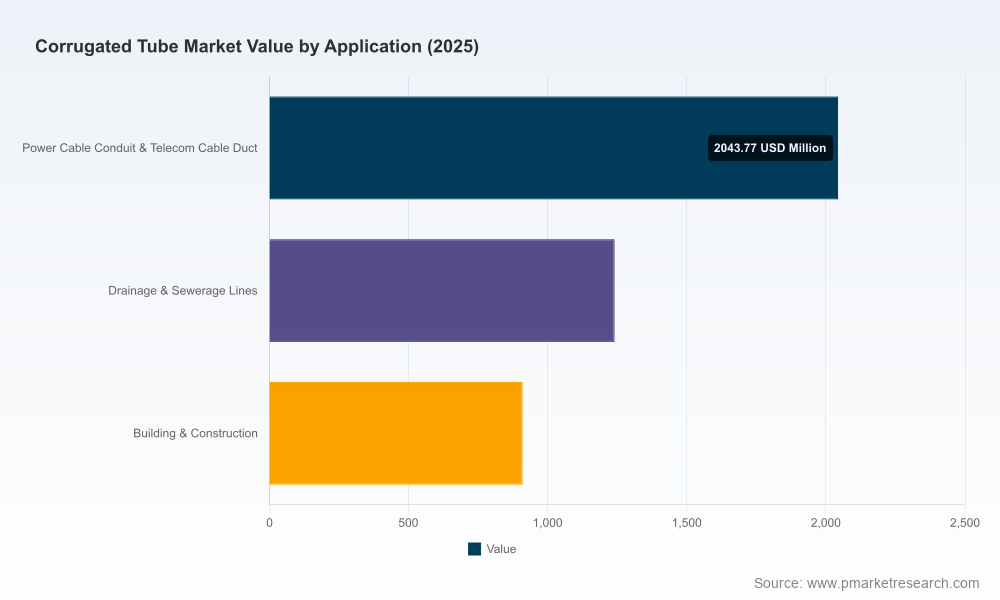

As organisations prepare capital allocation and market-entry strategies for 2026, the corrugated tube market presents a mix of predictable macro growth and concentrated operational risks. PW Consulting’s latest market study (base year 2025, historical window 2020–2025, forecast 2026–2032) frames that picture with quantified topline sizing and forward-looking scenarios: the global market expands from an estimated USD 3,487.5 Million in 2020 to USD 4,194.67 Million in 2025, and is projected to reach approximately USD 5,279.72 Million by 2032, reflecting a compound annual growth rate (CAGR) of 3.36% across the forecast horizon. This briefing synthesises the study’s strategic relevance for 2026 decision-makers — highlighting where to invest management attention, where to conserve optionality, and where the report’s detailed datasets provide the next level of actionable insight.

Corrugated Tube Market

Timing of strategic moves. The market’s steady mid-single-digit CAGR masks near-term pockets of supply-side volatility and regulatory-driven product redesigns. Companies planning plant expansions, pricing resets or product R&D in 2026 need a short, evidence-based runway to justify capex and to model margin scenarios under different raw-material and regulatory outcomes.

Corrugated Tube Market

Risk-informed resource allocation. Our analysis couples top-line growth projections with stress-tested scenarios for polymer-price shocks, labour constraints, and tightening recyclability mandates. This combination allows procurement, operations and commercial teams to prioritise hedging, localisation or diversification strategies aligned to corporate risk appetite.

Corrugated Tube Market

Competitive differentiation paths. The report separates commoditised drainage and conduit applications from higher-value engineered corrugated-tube applications (e.g., corrugated-tube heat exchangers), enabling leaders to weigh margin expansion through product engineering and services instead of purely volume-led plays.

Validated market sizing and forecast model (2020–2032): comprehensive topline figures by year, with baseline, upside and downside scenarios reflecting commodity price shocks and regulatory inflection points.

Segment-level anatomy (types, applications, regions): qualitative and quantitative frameworks to assess product-to-market fit. Note: detailed segment allocations and regional breakdowns are available in the full dataset to support deal diligence and route-to-market planning.

Cost-to-serve and margin mapping: build-your-own models that incorporate polymer indices, energy and logistics inputs so you can stress-test margin recovery levers under a variety of procurement strategies.

Competitive benchmarking: profiles of incumbent and specialist players, capacity footprints, technology plays and strategic initiatives — designed to identify partners, acquisition targets and defensive moves.

Regulatory impact assessment and design-to-recycle playbook: practical steps for reformulating products and supply chains to meet emerging recyclability requirements without eroding commercial viability.

Implementation roadmap and KPIs: a 12–36 month action plan tailored for manufacturers, system integrators and OEMs outlining priority levers, staffing needs and investment sizing (with templates for board-level presentation).

The corrugated tube sector remains a mix of established industrial manufacturers focused on drainage, conduit and infrastructure, alongside niche engineering specialists who commercialise corrugated geometries for thermal and process applications. Market concentration metrics indicate a fragmented marketplace: the top three players do not control the majority of the market, and the top five also leave significant share distributed among regional and specialist firms (CR3 ~26.4%; CR5 ~30.2%).

Advanced Drainage Systems (Columbus, Ohio, USA, https://www.adspipe.com/) — market leader in thermoplastic corrugated drainage systems. Their scale and channel relationships make them the default partner for large infrastructure projects and utilities procurement. For competitors, ADS’s strengths stress the need to differentiate on logistics, product variants or service-level guarantees.

Baughman Tile Company (Paulding, Ohio, USA, https://www.baughmantile.com/) — a regional manufacturer with deep ties to civil infrastructure contractors. Baughman’s playbook is operational excellence and proximity to contractors; it exemplifies the value of regional manufacturing to control lead times and installation outcomes.

HRS Heat Exchangers (Belgium, https://www.hrs-heatexchangers.com/) — a specialist in corrugated-tube heat exchanger technology. HRS demonstrates that corrugated geometries can unlock performance premiums in thermal systems, and that IP-rich engineering businesses can command higher margins and more resilient demand from industrial customers.

Kinam Engineering Industries (Sion, India, https://kinam.in/) — a vertically integrated manufacturer with in-house R&D. Kinam’s recent technical presence at India Energy Week 2026 underscores accelerating dissemination of corrugated-tube heat-exchanger know-how in Asia, and signals potential partnership and licensing opportunities for western OEMs seeking cost-competitive engineering supply.

Filson Filters (China, https://www.filsonfilters.com/) — an example of a regional specialist translating corrugated-tube geometries into filtration and heat-exchange applications for process industries. Filson illustrates the competitive dynamic where commodity players compete on price while specialists differentiate through integration with adjacent technologies.

Raw-material volatility: polymer indices (including HDPE) experienced notable swings in 2025, materially affecting production cost bases for corrugated tubing manufacturers. Procurement teams must layer price-hedging and multi-sourcing strategies to protect margin forecasts.

Regulatory pressure: the EU’s move to mandate recyclable product designs with verified recycled content has shifted product roadmaps toward redesign and authenticated supply chains. Firms that proactively embed recycled-content validation and recyclability-by-design will convert regulatory compliance into a competitive advantage; others risk costly after-the-fact re-engineering.

Installation labour constraint: industry data indicate a shortage of certified installation technicians, causing measurable delays at construction sites across mature markets. This creates an opportunity to monetise installation services, training programs and plug‑and‑play product configurations that reduce labour intensity.

Application bifurcation: commoditised drainage and conduit segments remain volume-driven and highly price-sensitive, while engineered corrugated-tube applications (heat-exchangers, specialised process equipment) trade on engineering IP and service depth. A one-size-fits-all commercial strategy will underperform; portfolio segmentation is necessary.

Fast-track recyclability pilots: run 6–9 month pilots that combine recycled-content formulations with third-party verification. Capture the cost delta, cycle time and quality impacts so commercial teams can articulate value to specifiers and procurement buyers.

Insulate margins from polymer volatility: implement a layered procurement approach combining short-dated physical coverage, index-linked contracts and strategic reserves at regional hubs. Use the supply-side stress tests in the report to size the optimal hedge and buffer inventory.

Invest selectively in service-led differentiation: training and certified installation programs convert a market-wide labour shortage from a liability into a premium service offering. Consider franchised installation networks or certified contractor programs tied to product warranties.

Evaluate bolt-on M&A and engineering partnerships: target small IP-rich players in corrugated heat-exchanger design and specialist filtration applications to capture margin accretion without starting from scratch. The report’s target screening tool helps prioritise targets by revenue density and technology moat.

Geographic and product hedging: avoid over-committing to single-region expansions without a clear plan for regulatory compliance and labour capability. Use flexible asset strategies (contract manufacturing, tolling, licensing) to retain market access while limiting fixed-cost exposure.

Consider this article the strategic trailer: it outlines the market dynamics and the strategic choices that executives must make in 2026. The full report contains the primary models and proprietary datasets you will need to operationalise those choices — including downloadable forecasts by year, scenario-adjustable cost models, a cadenced M&A target list, and templated slides for board-level approvals. To preserve the consulting value and the integrity of buy-side diligence, detailed segment tables, regional splits and the proprietary competitive scoring matrices are available within the full report package.

Executives who pair the topline growth context (2020–2025 historic, USD 3,487.5 Million to USD 4,194.67 Million; forecast to ~USD 5,279.72 Million by 2032 at a 3.36% CAGR) with the tactical playbook above will be best positioned to convert 2026 investments into durable commercial advantage. For procurement officers, product leaders and corporate development teams looking for the underlying spreadsheets, scenario engines and deal-screen filters, the full Corrugated Tube Market study from PW Consulting provides the operational toolkit to move from strategy to execution.

To explore the datasets, interactive models and company profiles referenced in this briefing, access the full study through PW Consulting’s report portal. The detailed segment and regional allocations, along with the competitive scoring that underpin M&A prioritisation and pricing strategies, are made available to subscribers and clients for diligence and planning.

For detailed analysis of this topic, please visit the official page:Corrugated Tube Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com