Polyisoprene (PI) Surgical Gloves Market Dynamics: Key Drivers and Restraints

Other |

2026-06-22 11:58:11

PW Consulting’s 2025 base-year estimate positions the global offshore containers market at approximately USD 0.35 Million (revenue unit: Million), with a compound annual growth rate (CAGR) of 7.2% baked into our 2026–2032 forecast. Under our central scenario the market climbs steadily through the forecast horizon, reaching an estimated USD 0.57 Million by 2032. These headline numbers frame a market that is small in headline dollar terms but strategically dense — a capital- and standards-intensive segment whose commercial dynamics amplify the impact of even modest shifts in demand, regulation or input costs.

Offshore Containers (Shipping Containers) Market

For corporate leaders making allocation decisions in 2026, offshore containers are no longer a peripheral procurement line-item. Three concurrent trends make the coming 18–36 months decisive:

Offshore Containers (Shipping Containers) Market

Together, these forces make supplier selection, supply-chain strategy and product specification decisions materially more consequential in 2026 than in prior cycles.

Offshore Containers (Shipping Containers) Market

This research is designed as a decision-support tool for procurement chiefs, engineering leads, M&A teams and product managers. Rather than academic segmentation alone, the report is engineered to be operationally actionable:

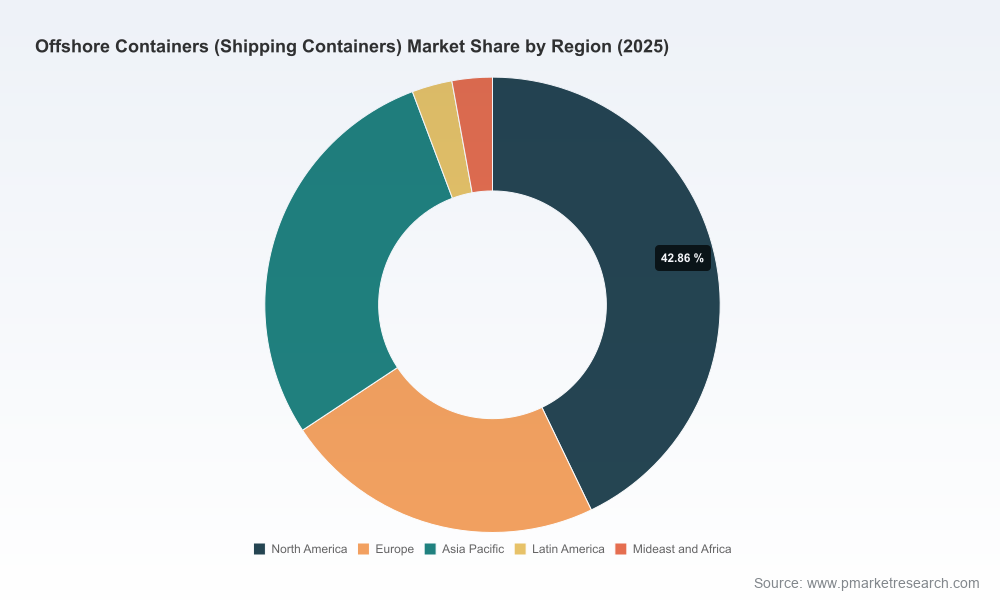

The market organizes along familiar vectors — container type, application and region — but these are evolving. Type innovation now spans classic closed units to specialized pressurized and fire-suppressed modules; applications range from equipment and supplies transport to niche roles in pipeline work and waste handling. Regionally, supply chains and demand drivers are asymmetric: geographic concentration of energy projects, proximity to fabrication hubs, and local regulatory regimes create distinct supplier advantages. PW Consulting’s full report contains the granular split by subsegment and region; this introduction intentionally omits those granular figures to preserve the strategic value of the full study.

The offshore container market exhibits an oligopolistic structure where a small set of specialized manufacturers and service providers dominate certification, aftermarket service and global reach. Key player archetypes and strategic positions include:

Recent market activity illustrates consolidation and strategic expansion: strategic acquisitions and private-equity-backed transactions have accelerated capabilities expansion (e.g., additions to container portfolios and specialized project capabilities); product launches are addressing new energy applications; and trade-show activity in 2026 signaled supplier readiness to capture next-wave demand. These dynamics push negotiating power toward suppliers with demonstrable certification pipelines and aftermarket footprints.

Regulation is a non-negotiable commercial variable. The DNV-ST-E271 and updated EN/ISO offshore container standards set design, testing and inspection thresholds that materially affect manufacturing cost and time-to-deployment. Recent ISO standard updates refine lifting-set requirements and extend marking/testing obligations for certain gross-mass classes. For buyers and OEMs, this raises two operational imperatives: (1) front-load compliance in specifications and acceptance testing, and (2) require traceable documentation and lifecycle inspection records from suppliers.

On inputs, marine-grade steel is a dominant cost component in certified steel offshore containers, accounting for a substantial share of manufacturing expense. Historical spot-price volatility has been significant, producing margin compression and transfer-price friction between suppliers and end-users. Procurement teams must therefore bake material-price risk into contract structures (indexation, hedging windows, and cadence-based price reviews) rather than rely on annual fixed-price models.

For executives and functional leads, the following prioritized actions will convert insight into defensible outcomes in 2026:

This article is purposely selective: it surfaces the strategic implications, competitive dynamics and the tactical playbook executives need to start acting in 2026, while withholding proprietary subsegment tables, supplier scorecards, and model workbooks that are part of the paid deliverable. The full PW Consulting Offshore Containers report contains the granular regional and application splits, downloadable financial models, supplier-level pricing band estimates, and editable procurement templates that procurement, engineering and M&A teams use to execute decisions with confidence.

For strategy teams preparing budgets, procurement teams renegotiating contracts, or corporate development evaluating acquisitions, the study converts market intelligence into executable next steps — reducing risk, shortening procurement cycles, and identifying value-accretive opportunities in a market where certification, supply-chain resilience and input-cost management determine winners and losers.

For detailed analysis of this topic, please visit the official page:Offshore Containers (Shipping Containers) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com