Colposcopy Market 2026: Strategic Imperatives from PW Consulting’s Market Introduction

As healthcare systems and device manufacturers confront accelerating shifts in diagnostics, our newest Colposcopy Market research — with a 2025 base year and a 2026–2032 forecast horizon — offers a timely, decision-grade view for executives planning 2026 investments. The global colposcopy market is on a steady upward trajectory (2025 baseline ~USD 610 Million, expanding toward roughly USD 960 Million by 2032 at an approximate 5.0% CAGR). That macro rhythm masks important inflection points tied to technology, reimbursement, and channel economics that will determine winners and losers over the next 18–36 months.

Colposcopy Market

Why this analysis matters for 2026 corporate decision-making

- Translate market momentum into capital allocation: with a mid-single-digit CAGR and clear upsides tied to digitalization and AI, firms must decide now whether to prioritize incremental product upgrades or invest in platform-level transformations that capture the higher-margin digital workflow.

- Optimize go-to-market before reimbursement windows shift: payment codes and add-on reimbursements meaningfully affect procedure economics; timely engagement with payors and coding authorities can unlock near-term ROI on new digital capabilities.

- Shape M&A and partnership posture: elevated fragmentation (CR3 ~25%; CR5 ~32%) signals opportunity for strategically targeted acquisitions and distribution alliances to rapidly build addressable share without long, costly organic ramps.

What the report delivers — practical modules for immediate action

We designed this report as an operational playbook, not an academic survey. Key deliverables included for executive teams and strategists:

Colposcopy Market

- High-confidence market sizing and model — historical (2020–2025) and a granular 2026–2032 forecast built on procedure-volume drivers, device ASP dynamics, and service/repeat-revenue assumptions.

- Regulatory and reimbursement intelligence — mapping relevant CPT codes, reimbursement levels, and the practical implications for device pricing, bundling, and clinical evidence generation strategies.

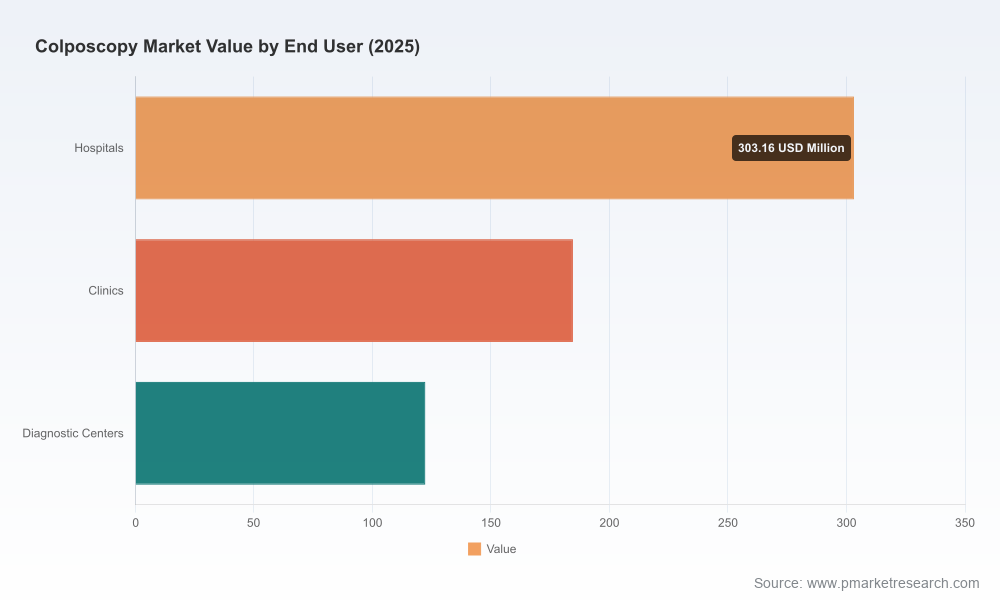

- Technology and clinical adoption heatmap — scored assessment of optical vs. digital systems, AI-enabled diagnostic adjuncts, and ancillary consumables, with a pragmatic runway for adoption in hospital, clinic, and diagnostic center settings.

- Competitive landscape with playbooks — profiles and strategic positioning for leading incumbents and fast followers, opportunity matrices for M&A, distribution, and co-development.

- Commercial frameworks — pricing templates, channel economics, and a go-to-market decision tree for market-entry, expansion, and segmentation strategies across mature and growth markets.

- Scenario planning and sensitivity analysis — upside and downside cases reflecting reimbursement shocks, regulatory delays, and accelerated AI acceptance; runway implications for revenue, margins, and free-cash-flow timelines.

To preserve the report’s proprietary value, granular regional and application-level splits are summarized in the full deliverable. The introductory analysis here signals strategic direction while encouraging access to the source for detailed segment outputs and downloadable worksheets.

Colposcopy Market

Market dynamics shaping near-term commercial outcomes

- Reimbursement is a lever, not just noise. Current CPT-level reimbursements materially influence procedure economics in key markets. For 2026, commonly used colposcopy procedure codes are associated with defined Medicare averages (for example, non-biopsy colposcopy and biopsy-inclusive codes), and certain advanced digital adjuncts carry add-on reimbursement that can materially improve the economic case for higher-cost devices. Companies that engage earlier with payors and coders — and that design bundled service propositions rather than one-off hardware sales — will capture disproportionate margin expansion.

- Regulatory and standards compliance remains table stakes. FDA clearance pathways and ongoing ISO equipment standards create predictable timelines for market entry; however, digital and AI-enabled elements add complexity around clinical validation and post-market surveillance. A clear regulatory playbook is indispensable when launching software-driven colposcopy solutions.

- Technology transition is both a risk and an opportunity. Optical systems retain strong demand for their cost-effectiveness and simplicity, while digital colposcopes and AI-assisted interpretation are capturing premium pricing and broader workflow integration. The transition pace will vary by payer environment and clinician comfort, creating pockets of rapid uptake and others of prolonged legacy-device loyalty.

- Fragmentation creates acquisition windows. With measured concentration among top players and a dispersed field of smaller device and accessory vendors, strategic buyers can target bolt-on acquisitions to accelerate digital capability, distribution reach, or consumables recurring revenue.

Competitive landscape — positioning and strategic implications

The market is defined by a mix of large platform players and specialized manufacturers. Several incumbent profiles — and their strategic playbooks — matter for 2026 planning:

- Hologic Inc. — leverages a vertically integrated cervical-health portfolio (HPV testing, cytology integration, and colposcopy) and is actively embedding AI into diagnostic workflows. For competitors, Hologic’s approach underscores the advantage of platform convergence: cross-selling opportunities and tighter clinical workflows that increase switching costs.

- Karl Storz SE & Co. KG — a diagnostics and optics specialist whose VITOM™ systems demonstrate how surgical-grade visualization can be repurposed for colposcopic and procedural applications. Their strength is optical excellence and integration into procedural suites, which suggests that mid-to-high-end clinical settings will remain a key addressable segment.

- CooperSurgical, Inc. — known for pragmatic product portfolios including modular colposcopes with clinical ergonomics in mind. Their breadth illustrates the importance of range offering: companies that can serve both entry-level and premium tiers reduce churn across hospital systems and clinics.

- MedGyn Products, Inc. — a nimble innovator delivering HD digital video systems and disposable procedure kits, and recently expanding distribution in Latin America. This profile exemplifies how focused product innovation and regional partnerships can rapidly scale adoption in emerging markets.

- Olympus Corporation and ATMOS MedizinTechnik — represent established medical-imaging players emphasizing single-handed operation, extended magnification, and video integration for efficient office workflows. Their strengths lie in brand trust and durable service networks.

Recent industry moves reinforce strategic themes. In 2025, Hologic launched an AI-integrated colposcopy device; Apgar Danmark’s acquisition of DYSIS in early 2025 highlights consolidation around digital cervical mapping; and region-focused distribution deals (e.g., MedGyn in Latin America) show the power of local partnerships to accelerate market penetration.

Strategic priorities for 2026 — tactical playbook

- Prioritize clinical evidence for AI and digital adjuncts. For premium pricing and payer acceptance, prospective studies demonstrating improved sensitivity, workflow efficiency, or reduced follow-up procedures are decisive.

- Design reimbursement-first product strategies. Map device features to billable codes and build commercial bundles (device + subscription + training) that improve payer economics and provider cash flows.

- Pursue targeted M&A and distribution deals. Use the fragmented structure to acquire complementary digital tech, expand consumables portfolios, or secure local distribution in underpenetrated regions.

- Segment GTM by customer economics. Differentiate approaches for high-volume hospitals, mid-size clinics, and diagnostic centers: pricing models, financing, and service packages should mirror each segment’s procurement cadence and utilization patterns.

- Invest in service and training. Adoption of digital/AI tools is as much about clinician trust as technological capability. Scalable training programs and outcome-driven service contracts will accelerate clinician conversion.

Risk factors and mitigations

- Reimbursement uncertainty — regularly model scenarios with both code changes and add-on removal; maintain payer-engagement plans and flexible pricing to manage revenue shocks.

- Regulatory delays — front-load regulatory resources and adopt modular validation strategies for software updates to avoid full re-submissions.

- Adoption inertia — deploy early-adopter pilots with quantifiable KPIs and clinician champions to accelerate diffusion.

- Competitive price pressure — protect margins by building service and consumable revenue streams that are harder to replicate than hardware alone.

Next steps — how to use this insight

PW Consulting’s Colposcopy Market report equips strategy and commercial teams to make high-confidence choices in 2026: whether to greenlight R&D investments in AI-enabled imaging, pursue bolt-on acquisitions, restructure channel incentives, or recalibrate pricing against payer realities. The full report contains the proprietary segmentation matrices, granular regional and application models, and downloadable financial templates that transform these strategic imperatives into executable plans.

Our introduction is intentionally selective: it demonstrates the analytic framing and immediate strategic takeaways while preserving detailed segment-level intelligence for the full deliverable. Contact PW Consulting to access the complete dataset, forecast files, and our executive briefing workshop that will convert market insight into an operational 2026 roadmap.

For detailed analysis of this topic, please visit the official page:Colposcopy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com