Why Is Anti-Graffiti Coatings Market Gaining Importance in Urban Infrastructure Protection?

Networking |

2026-06-04 08:27:07

As the intimate apparel value chain moves from product engineering to systems-level sustainability and performance differentiation, corporate choices made in 2026 will decide who captures the faster-growing segments of the bra cups market over the rest of the decade. PW Consulting’s latest market research synthesizes historical performance (2020–2025), an actionable 2026 planning lens, and a seven-year forecast horizon (2026–2032). It is designed to inform procurement, innovation, M&A, and go-to-market playbooks without substituting for your proprietary commercial due diligence.

Bra Cups Market

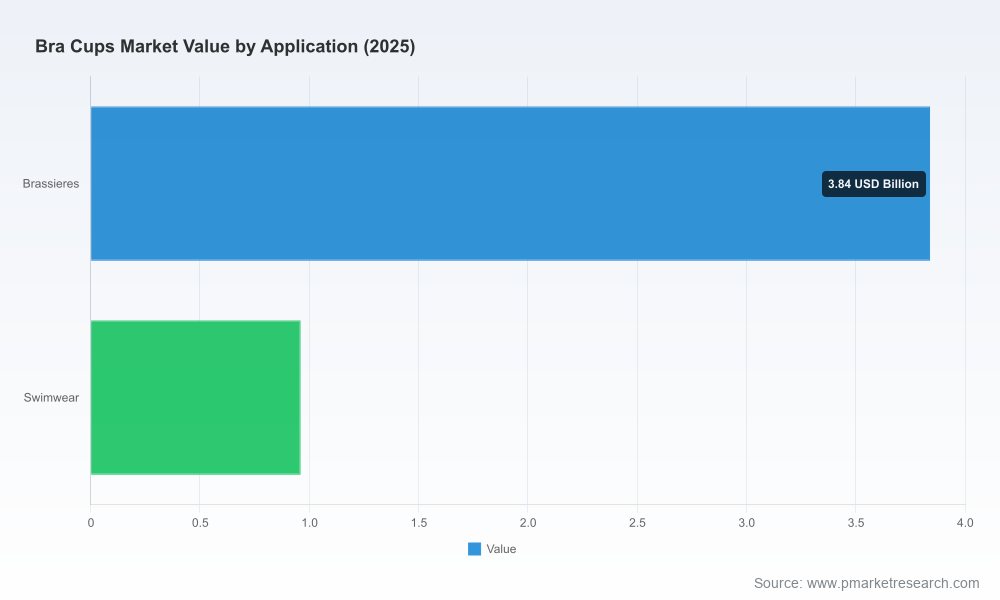

Market scale and momentum: the global bra cups market expanded from USD 3.35 Billion in 2020 to USD 4.80 Billion in 2025 (base year). Our forecast anticipates continued expansion to roughly USD 7.12 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.9% across the forecast window.

Bra Cups Market

Concentration and competitive tension: the market sits in a mid-consolidation zone — the top three firms account for just over 40% of the market, while the top five approach roughly half. This structure creates pockets of scale advantage for large incumbents and persistent opportunities for specialty innovators.

Bra Cups Market

Timing for action: 2026 is a pivotal year. Regulatory frameworks and supply-side material shifts accelerate adoption curves; first movers on mono-material recycling, bio-based polymers, and low-carbon foam solutions will enjoy sustainable cost and brand advantages by 2028–2030.

Procurement leaders need a forward-looking supplier map that ranks partners by technical readiness, scalability, and regulatory compliance — not just price. The cost of retrofitting product lines in response to new regulations and material bans will exceed the cost of earlier qualification in most cases.

R&D and product teams must prioritize materials with credible end-of-life solutions. The transition to mono-material designs and biopolymers, and the emergence of CO₂-derived foams, change tooling, assembly, and labeling requirements.

Strategy and M&A teams should view the market as a two-track ecosystem: consolidated scale players defending share through distribution and multi-category portfolios, and specialist material innovators seeking licensing and JV exits. Timing acquisitions or strategic partnerships in 2026 will determine access to next-generation IP and feedstock security.

Sustainability regulation moves from guidance to obligation. The European Union’s Ecodesign for Sustainable Products framework — expected to extend into apparel by 2027 — changes procurement specs and supplier scorecards. Chemical safety regimes in primary markets (EU, US, key Asian countries) further constrain material choices and speed qualification timelines.

Material innovation is both a challenge and an enabler. Recent commercial introductions — plant-based EVA polymers, mono-material spacer fabrics made from recycled polyester, and CO₂‑derived foam chemistries — create alternatives to traditional polyurethane foam and mixed-composition laminates. These options reduce lifecycle emissions and simplify recycling but demand process adaptation.

Channel and consumer expectations diverge. Performance and fit remain table stakes; sustainability credentials and inclusive sizing deliver differentiation. Retailers and DTC players that can credibly articulate circularity, regulatory compliance, and garment traceability will win higher margins and stronger loyalty.

Muehlmeier Bodyshaping (Germany): Positioned as an engineering-led supplier, Muehlmeier is commercializing mono-material approaches and bio-based spacer options. Their focus on recycled polyester for easier recycling demonstrates a playbook for partners seeking circularity without sacrificing scale. For brands: this supplier represents a lower-risk path to certification and closed-loop claims, but requires early integration into design and assembly processes.

Gelmart International (Brazil): Gelmart’s “plant-based” product line showcases a differentiated materials strategy centered on bio-sourced EVA. This is strategic for brands prioritizing biobased content and green marketing; it also signals opportunities for regional feedstock and sourcing advantages outside established petrochemical supply chains.

Fullstride Ventures (Austria): The carboncup™ launch — a CO₂-derived foam showcased at K Show 2025 — is emblematic of a high-impact technology route that can materially lower product carbon footprints. Early adopters partnering with Fullstride can access brandable sustainability credentials, but must manage supply risk and premium cost during scale-up.

Wacoal Holdings & Triumph International: These legacy intimates manufacturers are pursuing sustainable sourcing and process initiatives (e.g., water-conserving dye techniques, 2030 sourcing targets). Their control of brand, fit libraries, and channel access makes them attractive collaborators for suppliers with compliance-ready technologies.

Hanesbrands, Victoria’s Secret & PVH: These North American–centric players balance mass-market scale with innovation in performance and inclusivity. Their labs and in-house design capabilities make them important early customers for sports/active bra cup innovations and for validating mass production readiness of new materials.

Prioritize supplier qualification for mono-material and bio-based options now. Running concurrent trials across two or three vetted suppliers reduces risk of single-source failure as regulatory timelines tighten.

Embed regulatory scenario planning into product roadmaps. Assign cross-functional owners to track Ecodesign, restricted-substances lists, and labeling requirements to avoid late-stage reformulation.

Reassess cost-to-serve with a lifecycle lens. Incorporate circularity premiums, end-of-life logistics, and potential recycling credits into SKU-level contribution analyses.

Design partnerships not only for materials but for feedstock security. Long-term offtakes or joint investments with polymer suppliers, or licensing agreements with material innovators, can protect margin pools during scale-up.

Use channel segmentation to pilot innovations. Treat performance and DTC channels as low-risk testbeds for new cup constructions and sustainability claims before scaling to full retail assortments.

Validated historical market model (2020–2025) and forward-looking forecast (2026–2032) with scenario sensitivities to raw material price swings, regulatory adoption rates, and consumer premium tolerance.

Supplier and technology matrix that assesses technical readiness, scale pathways, and compliance posture for the leading material and foam innovations.

Commercial playbooks: SKU-level margin simulations, channel pilot templates, and product launch checklists tailored for brands, private labels, and OEMs.

Regulatory compliance roadmap and a restricted-substances crosswalk for key jurisdictions, plus recommended audit protocols and lab test specifications.

M&A and partnership prioritization framework identifying target archetypes, valuation levers, and integration risks for 2026 deal-making.

Practical recommendations for circularity pilots, including design-for-recycling guidance and suggested KPIs for year-over-year improvements.

Short-term (0–12 months): finalize supplier trials for at least two sustainable cup constructions, update spec sheets, and conduct regulatory gap analyses for all SKUs planned for 2027 release.

Medium-term (12–36 months): negotiate strategic procurement contracts with feedstock security clauses; launch controlled channel pilots and collect performance and return-rate data.

Long-term (36+ months): consolidate supplier networks around scalable, certified technologies; evaluate M&A opportunities to secure IP or expand capacity as adoption matures.

PW Consulting’s public preview highlights the directional forces and strategic choices facing leaders in 2026. To preserve the competitive utility of our analysis — and to help you make market-entry or scale decisions with full granularity — core segmentation data and proprietary supplier scoring matrices are reserved for the full report and client engagements. Accessing the complete study will provide the precise split analyses, supplier contact diligence packs, and the downloadable market model you need to underwrite 2026 investments.

Request the full report or a tailored briefing to get the detailed segmentation, supplier due diligence packs, and scenario files that operational teams need to execute.

Book a strategy workshop with our industry leads to convert insights into a 90‑day implementation plan focused on procurement, R&D, and channel pilots.

Decisions taken in 2026 — on materials, partners, and compliant product architectures — will determine not only near-term market share but the durability of sustainability claims and cost competitiveness through 2032. PW Consulting’s full Bra Cups Market study is structured to give you the quantified levers and executable playbooks to win that race.

For detailed analysis of this topic, please visit the official page:Bra Cups Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com