Natural Source Vitamin E Market — Strategic Briefing for 2026 Decision Makers

Executive snapshot

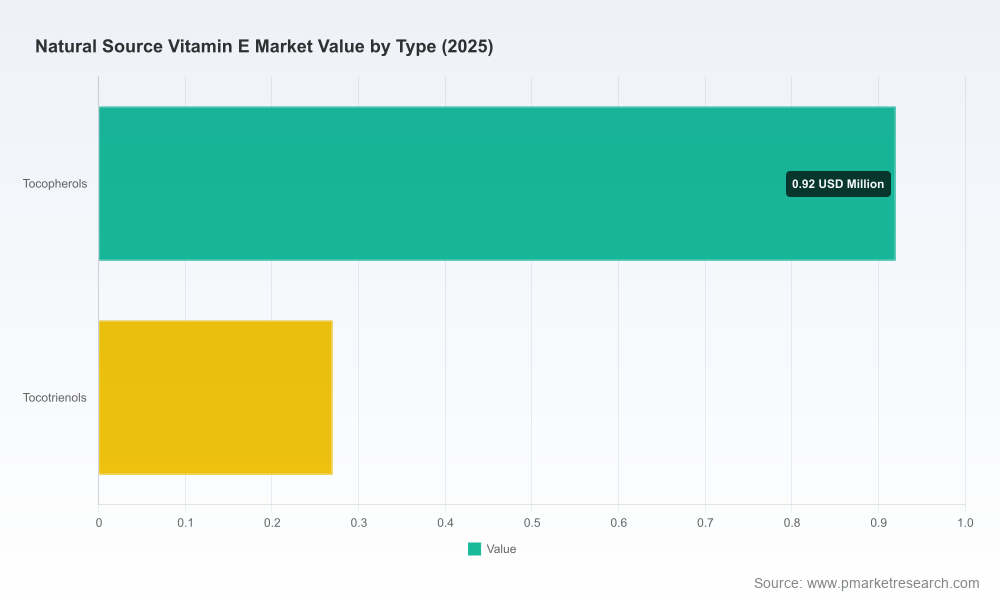

The global natural-source vitamin E market is at an inflection point. After a measured recovery across 2020–2025, our base-year assessment (2025) values the market at approximately USD 1.19 million (revenue unit: Million). PW Consulting’s forecast through 2032 models sustained expansion to roughly USD 2.00 million by 2032, reflecting a compound annual growth rate (CAGR) of 7.78% over the 2026–2032 forecast window. That trajectory is being driven by a mix of premiumization in supplements and personal care, cleaner-label demand in food ingredients, and technology-led product differentiation such as high-purity fractions and upcycled feedstock offerings.

Natural Source Vitamin E Market

Why this analysis matters for 2026 strategy

- Investment timing: The next 12–18 months are decisive for capex and M&A planning. With a mid-to-high single-digit CAGR, greenfield capacity decisions and bolt-on acquisitions must weigh near-term feedstock volatility against a structurally larger market in 2030–2032.

- Commercial positioning: Brands and ingredient suppliers can capture margin uplift by aligning claims (natural, non‑GMO, upcycled) with validated regulatory pathways and third-party certifications — now a differentiator in procurement and retail channels.

- Procurement & risk management: Feedstock and logistics shocks have created asymmetry between spot and contracted supply costs. Buyers that redesign sourcing contracts and hedging mechanisms for oil-derived distillates will protect margins and retain formulation flexibility.

- Product portfolio strategy: Molecular variants and concentration grades (e.g., mixed tocopherols vs. targeted high-purity fractions) are not interchangeable in commercial use-cases. Choosing which variants to prioritize affects R&D, quality systems, and go-to-market timelines.

- Regulatory readiness: Updated safety evaluations and regional approvals materially affect label claims and allowable use-levels. Companies that have a regulatory-forward roadmap will convert compliance into competitive advantage.

What the PW Consulting report delivers — practical, transaction-ready intelligence

- Top-down market sizing and growth scenarios (historical 2020–2025 and forecast 2026–2032) with sensitivity testing for feedstock price and demand shocks.

- Segment-level diagnostics (by type, application and geography) and scenario matrices that translate market movement into revenue and margin outcomes for suppliers, ingredient formulators and finished-goods manufacturers. Note: the full report contains the proprietary, granular splits and model outputs required for commercial planning.

- Supply-chain mapping from oilseed origin through deodorizer distillates to refined tocopherol/tocotrienol streams, highlighting single‑point failures, capacity hubs and alternative feedstock pathways.

- Company scorecards and capability assessments (manufacturing footprint, product portfolio, sustainability claims, certifications, and route-to-market), including primary-source verification and recent commercial/operational developments.

- Regulatory tracker and claims playbook covering EFSA, major APAC authorities and U.S. FDA practice — with scenario playbooks for claim substantiation and label risk mitigation.

- Commercial playbooks for formulators and brands: sample supplier negotiation tactics, contract structures (indexing vs. fixed), and pricing levers for premium and value tiers.

Competitive landscape — positioning and near-term moves to watch

The supplier base features established agribusinesses and specialty ingredient houses. Each player pursues a slightly different value proposition — from scale and upstream integration to clean-label and upcycling innovations. PW Consulting’s analysis covers strengths, near-term risks and partnership opportunities for each of the following providers:

Natural Source Vitamin E Market

- Archer Daniels Midland Company — leverages large vegetable oil processing scale and established Novatol® product lines for broad distribution across supplements and fortified foods. Strengths: integration, supply security, institutional customer relationships.

- Kensing, LLC — an emergent player differentiating on upcycled sunflower-derived tocopherol (Sun E®) and clean-label positioning. Recent commercialization and certification wins position it as a preferred supplier for mission-driven brands pursuing traceability and EFSA‑grade claims.

- Koninklijke DSM N.V. — brings a combination of high‑purity vitamin E fractions and formulation know‑how to nutrition and pharma customers, enabling tailored solutions where dosage form and stability are critical.

- BASF SE — a major producer with technical-grade acetates and refined tocopherols. Operational resilience and restart timelines following plant-specific disruptions are central to market stability and short-term availability.

- Louis Dreyfus Company (LDC) — expanding into plant-based vitamin E portfolios with a commercial focus on mixed tocopherols and derivative forms suitable for food ingredients and supplements.

- Cargill, Inc. — combines upstream oilseed sourcing with downstream extraction expertise; strong in feedstock access and commodity-channel relationships that support scale production for food and personal care sectors.

- Nutralliance — a specialty supplier emphasizing sunflower-derived, non‑GMO and allergen-free formats for clean-label market segments and smaller-batch customers seeking formulation flexibility.

- Qufu New Element Bioengineering Co., Ltd. — a high-purity producer with cost-competitive manufacturing in China, increasingly relevant for global buyers balancing price and quality.

Recent industry developments amplify strategic signals: in 2025–2026 several suppliers announced product launches and regulatory milestones (notably upcycled and phytosterol-validated offerings) while others navigated force‑majeure events and subsequent capacity restorations. Buyers should treat supplier news flow as an input into procurement scorecards rather than as a sole basis for strategic decisions.

Natural Source Vitamin E Market

Supply dynamics, regulatory noise and pricing implications

Raw material volatility is the dominant short-term driver. Crude vegetable oil price spikes and disruptions in key shipping routes have transmitted directly into ingredient transaction costs and spot market dislocations. Geopolitical risks and biofuel demand add a structural layer of uncertainty to oilseed availability. At the same time, natural-source product positioning commands a material premium relative to synthetic alternatives — an important commercial lever for differentiated products but a cost headwind for margin-sensitive categories.

On the regulatory front, recent evaluations have clarified safety positions for certain vitamin E derivatives, providing pathways for label claims and ingredient introductions in major markets. Regulatory outcomes will increasingly determine which claims (e.g., “natural,” “upcycled,” or specific formulation descriptors) can be reliably used in consumer-facing communications.

2026 strategic scenarios and recommended plays

- Base-case (moderate growth, periodic volatility): Prioritize flexible sourcing (multi-origin contracts), co-development agreements with specialty suppliers, and a two‑tier product strategy — premium natural SKUs with validated claims and cost-optimized formulations using blended inputs.

- Upside (accelerated premiumization + ingredient innovation): Accelerate investment in high-margin categories (nutraceutical concentrates, high-purity fractions, tocotrienol-enriched formulations) and secure exclusivity or early-access arrangements with innovative suppliers. Consider selective M&A to acquire differentiating tech or feedstock control.

- Downside (prolonged feedstock shock or regulatory tightening): Focus on rationalizing SKUs, renegotiating supply contracts to incorporate indexation and force‑majeure protections, and fast-tracking alternative feedstock qualification programs to mitigate single-source dependencies.

Practical next steps for 2026 execution

- Operational: Run dual-sourcing pilots for at least two critical vitamin E grades, with delivery KPIs and stress-test clauses.

- Commercial: Reclassify SKUs by margin and risk exposure; allocate R&D and marketing spend to high-return, claim-differentiated products.

- Finance & M&A: Use scenario-adjusted DCFs that incorporate feedstock price indices and capacity restart timelines when evaluating targets or greenfield projects.

- Regulatory & Quality: Maintain a rolling regulatory dossier and third-party validation plan for any new “natural” or “upcycled” claims to avoid costly relabelling and market interruptions.

How PW Consulting supports executive teams

- Decision-grade market models and a customizable financial model that allows you to stress-test procurement, pricing and investment options against feedstock and regulatory scenarios.

- Supplier diligence packs and negotiation playbooks tailored to vitamin E supply dynamics, including recommended contractual language for price pass-throughs and supply security clauses.

- Regulatory roadmaps and claim substantiation templates to accelerate product launches and minimize compliance risk.

- Advisory support for M&A and strategic partnerships, including target shortlist, valuation framework and integration checklist.

Conclusion — why read the full report

For 2026 planning, leaders need more than directional conviction; they need transaction-ready inputs: granular segment splits, supplier scorecards, scenario-tuned financials and a prioritized action plan that converts market growth into captured margin. This briefing highlights the strategic inflection points — supply risk, premiumization, regulatory clarity and supplier differentiation — but intentionally omits the proprietary segmentation tables and granular supplier metrics that underwrite executable decisions. PW Consulting’s full Natural Source Vitamin E Market report contains those controlled data sets, primary-source appendices and a calibrated model you can deploy immediately for procurement, product and M&A choices.

Contact PW Consulting to obtain the complete report and the model package for 2026 strategic planning.

For detailed analysis of this topic, please visit the official page:Natural Source Vitamin E Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com