Run‑Flat Tires Market: Strategic Preview for 2026 Decision‑Makers

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I present a high‑level briefing that frames the strategic choices facing executives and investors in the run‑flat tire sector as they approach 2026. This preview highlights the market’s macro trajectory, the competitive dynamics that will shape supplier and OEM positioning, and the operational levers that determine winners and losers. It deliberately showcases analytical depth while withholding proprietary segment tables and granular revenue splits — an intentional “trailer” to guide you to the full report for complete, actionable data.

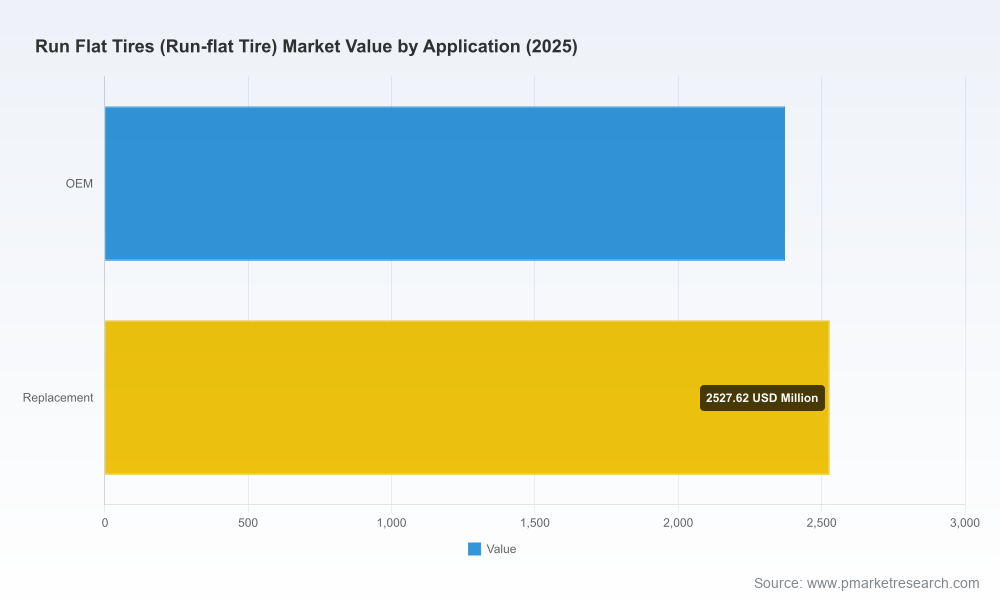

Run Flat Tires (Run-flat Tire) Market

Why this briefing matters for 2026

- Pace of adoption is moving from niche safety option to an increasingly mainstream specification across select vehicle classes. Procurement cycles, OEM platform refreshes, and aftermarket service strategies planned in 2026 will dictate share outcomes for the remainder of the decade.

- Capital allocation decisions — R&D investment in reinforced‑sidewall compounds, capacity expansions, and aftermarket distribution partnerships — must be calibrated to the market’s medium‑term growth profile and concentration dynamics.

- Regulatory and repair standards that continue to evolve in 2026 alter aftermarket economics and total cost of ownership arguments that fleet operators and OEM purchasing teams use to justify run‑flat fitment.

Market trajectory in macro terms

Using 2025 as the base year, the run‑flat tire market has demonstrated steady expansion through the 2020–2025 historical window, growing from the low‑4,000s (USD Million) to approximately USD 4,900 Million in 2025. Our forecast horizon (2026–2032) projects continued, above‑average growth with a compound annual growth rate (CAGR) of roughly 5.91%, taking the market toward the high‑7,000s (USD Million) by 2032 under the central case.

Run Flat Tires (Run-flat Tire) Market

That trajectory reflects a combination of structural and tactical drivers: incremental OEM-spec adoption for safety and space‑saving packaging (reducing reliance on spare wheels), rising consumer willingness to pay for convenience and mobility assurance, and specialized demand from security and military channels where run‑flat inserts and reinforced systems are mission‑critical. The overall market performance also reflects the premium nature of run‑flat technologies — reinforced sidewalls and high‑performance compounds materially raise manufacturing cost bases relative to commodity tire lines.

Run Flat Tires (Run-flat Tire) Market

What is changing beneath the surface

- Technology convergence and differentiation: Self‑supporting (sidewall reinforced) systems remain the most visible form factor on passenger vehicles, while support ring and insert systems continue to dominate certain commercial and defense applications. Suppliers are investing in compound science and structural design to close performance compromises (ride comfort, rolling resistance) historically associated with run‑flat designs.

- Aftermarket and OEM tension: The economics of fitting run‑flat tires at OEM vs. aftermarket create a persistent tension. OEM fitment supports long‑term adoption but requires alignment on validation protocols, vehicle integration, and warranty regimes. Aftermarket growth depends on technician competency, repairability standards, and clear TCO messaging.

- Regulatory and repair policy divergence: Repair guidance varies by technology and supplier. Some manufacturers allow repairs under strict conditions; others explicitly disallow repair after pressure loss. These policy differences materially affect aftermarket service models and residual value perceptions for vehicles equipped with run‑flat tires.

Strategic implications for core stakeholders

- OEMs: For platform planning cycles in 2026, run‑flat selection is no longer just a comfort vs. weight trade‑off. It is a systems decision that impacts chassis tuning, wheel architecture, spare storage strategies, and fleet appeal in safety‑sensitive segments. OEMs should model variant economics across three scenarios: conservative (limited fitment), selective (premium trims and specific model families), and aggressive (broader adoption tied to space‑saving design wins).

- Tier‑1 and tire manufacturers: The mid‑term premiumization of run‑flat technologies rewards focused investments in compound R&D, manufacturing process controls, and quality assurance systems. With market concentration indicating a small group of leading players holding a disproportionate share, challengers must pursue niche differentiation (e.g., weight reduction, comfort parity, improved rolling resistance) or secure exclusive OEM relationships to gain traction.

- Fleets and aftermarket service providers: Fleet procurement teams must evaluate run‑flat fitment not only on uptime benefits but also on repairability rules and lifecycle costs. Service networks need training, parts availability, and clear policies to avoid unwelcome downtime or warranty disputes.

- Defense and special‑use operators: Military and security users emphasize survivability and post‑damage mobility. Suppliers that pair ballistic materials with proven insert technologies retain an advantage; integration testing and certification (to relevant military standards) remain critical procurement gates.

Competitive landscape — who matters and why

The run‑flat segment demonstrates a concentrated supplier landscape that balances global OEM incumbents and specialized systems providers. Market concentration indicators point to a scenario where a handful of global tire majors capture a meaningful share of revenue, while a tier of specialized run‑flat systems companies dominates military and niche commercial applications.

- Global tire majors: Names such as Michelin, Bridgestone, Pirelli, Continental, Goodyear, Hankook, Yokohama and Nankang are active with technology variants (self‑supporting, ROF/EMT, ZPS, SSR) tailored to passenger and light commercial applications. Their strengths lie in integrated R&D, scale manufacturing, and established OEM relationships.

- Specialized system suppliers: Companies such as Hutchinson, Tyron, RunFlat International, and Runflat CBR operate in the run‑flat insert and wheel‑system niches. Their propositions emphasize extreme endurance, military certifications, and aftermarket retrofit capabilities that mainstream OEM suppliers do not always provide.

- Strategic observations: Established majors are extending run‑flat portfolios to meet both OE and aftermarket demand. Specialized suppliers retain strategic importance where application requirements exceed the technical envelope of conventional run‑flat tires (e.g., armoured vehicle mobility). Expect continued alliance activity — co‑development agreements, licensing, and JV models — as tire manufacturers and system specialists seek to broaden addressable applications.

Regulation, materials and operational constraints

Three non‑market factors will disproportionately shape 2026 decisions:

- Repair and safety regulations: Manufacturer guidance and national standards differ on whether run‑flat tires can be repaired after a pressure loss. These differences change the aftermarket playbook and will influence insurer and fleet policies.

- Raw material and cost structure: Run‑flat designs rely on heavier reinforcement, specialized rubbers and, in the case of military inserts, ballistic materials. These inputs raise per‑unit costs and create supply‑chain sensitivity to polymer price swings and availability. Procurement teams must secure continuity of supply or develop validated alternatives.

- Testing and validation complexity: The integration of run‑flat systems into vehicles increases vehicle‑level validation burden. Ride, NVH (noise/vibration/harshness), braking, and fuel efficiency impacts require iterative co‑engineering between tire and vehicle OEM teams.

What our full report delivers (high‑value, actionable elements)

The complete PW Consulting market study provides the granular intelligence that underpins confident 2026 decisions. High‑value deliverables include:

- Detailed market sizing and forecasting (historical 2020–2025, base year 2025, forecast 2026–2032) with scenario analyses reflecting alternative adoption curves and macro shocks.

- Segment‑level economics (type, application, region) with demand drivers, margin benchmarking, and price elasticity insights — presented in interactive models you can export to inform business cases.

- Comprehensive competitive intelligence dossiers: product portfolios, technology roadmaps, manufacturing footprints, strategic priorities, and M&A likelihood assessments for leading global players and specialized systems suppliers.

- Regulatory and repair‑policy playbook that translates manufacturer guidance and regional standards into practical aftermarket operating models and warranty clauses.

- Supply‑chain risk diagnostics and procurement levers to mitigate raw‑material exposure and secure critical inputs for reinforced sidewalls and specialized compounds.

- Commercial go‑to‑market strategies for OEMs and aftermarket players — channel design, pricing gap analysis, fleet engagement frameworks, and service network requirements.

- Investment and capex guidance: priority R&D areas, break‑even horizons for plant upgrades, and partnership archetypes that minimize time to market.

How PW Consulting helps you act in 2026

- Strategic due diligence: Tailored assessments for M&A targets or partnerships, including technology validation and integration risk mapping.

- Commercial launch support: Co‑development planning with OEMs, pricing architecture, and aftermarket roll‑out playbooks.

- Procurement and sourcing advisory: Hedging strategies for polymer price risk and supplier qualification frameworks for ballistic and high‑performance compound inputs.

- Operational turnarounds: Plant layout optimization and quality systems to reduce yield losses inherent in run‑flat manufacturing.

Conclusion — the decision calendar for 2026

The run‑flat tire market is at a strategic inflection point going into 2026: durable growth, concentrated incumbency, and divergent application needs combine to create both risk and opportunity. Firms that align product development, OEM engagement, and aftermarket economics to the market’s projected 5.91% mid‑term growth will capture disproportionate value. Conversely, firms that under‑invest in compound and structural innovation, fail to resolve repairability and service propositions, or neglect supply‑chain resilience will see margin compression as premium expectations harden.

This briefing is a gateway. For the complete dataset, proprietary segmentation matrices, and the tactical decision tools referenced above, access our full Run‑Flat Tires Market report on the PW Consulting insights portal. The full study contains the granular forecasts and executable recommendations necessary to convert 2026 strategy into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Run Flat Tires (Run-flat Tire) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com