Hydrogen Sulfide (CAS 7783-06-4) Market — Strategic Briefing for 2026 Decisionmakers

Executive preview

As organizations finalize 2026 strategies, understanding the near-term trajectory of the Hydrogen Sulfide (H2S) market is a strategic imperative. PW Consulting’s latest study — based on a 2025 base year and covering the historical period 2020–2025 with a forecast through 2032 — shows a resilient market expanding from roughly USD 110 million in 2020 to USD 143.1 million in 2025, and continuing toward just under USD 198 million by 2032. The study’s central outlook is driven by a compound annual growth rate (CAGR) of 4.9% over the forecast window. This briefing highlights why those topline dynamics matter for C-suite and business unit decisions in 2026 without disclosing the granular segment tables reserved for subscribers.

Hydrogensulfide (CAS 7783-06-4) (Hydrogen Sulfide) Market

Why this research matters for 2026 decisions

- Procurement and supply continuity: H2S remains a critical feedstock and process intermediate across refining, chemical manufacturing, and specialized industrial uses; small shifts in supply or pricing can materially affect margins and operational continuity.

- Capacity and capex planning: Given the projected steady growth through 2032, capital investments in storage, handling, or on-site generation should be evaluated against multi-year demand curves rather than single-year forecasts.

- M&A and competitive positioning: The market exhibits notable concentration among a handful of global suppliers — an important context for both acquirers and targets when valuing scale, access to customers, and distribution capabilities.

- Regulatory and safety investments: Evolving safety regulation and community scrutiny raise the bar on compliance and social license to operate; investment in best-in-class handling and monitoring is both a risk mitigator and commercial differentiator.

- Pricing and contracting strategies: The combination of predictable growth and concentrated supplier capacity creates opportunities to redesign procurement contracts to include dynamic pass-throughs, risk sharing, and strategic allies.

Market trajectory and implications for strategy

The market’s expansion from about USD 110 million in 2020 to USD 143.1 million in 2025 reflects recovery dynamics and structurally steady demand among core end markets. The 4.9% CAGR through 2032 indicates that while H2S is not a high-growth commodity, it is far from stagnant — creating a multi-year runway for strategic initiatives such as process integration, supply-chain optimization, and product-line extension.

Hydrogensulfide (CAS 7783-06-4) (Hydrogen Sulfide) Market

For decisionmakers, this trajectory translates into three practical implications:

Hydrogensulfide (CAS 7783-06-4) (Hydrogen Sulfide) Market

- Horizon planning: Multi-year procurement commitments and mid-life CAPEX should be stress-tested against the base-case CAGR and two alternative scenarios (downside: slower oil & gas activity; upside: accelerated chemical demand and increased sulfur recovery projects).

- Risk layering: Price and availability risk should be managed through a layered approach combining spot flexibility, strategic inventory, and preferred-supplier agreements with capacity guarantees.

- Value capture: Given modest but steady growth, value capture is more likely through operational excellence (logistics, safety) and product differentiation (purity grades, packaging formats) than through broad market expansion alone.

Segmentation lens — what the preview reveals (and withholds)

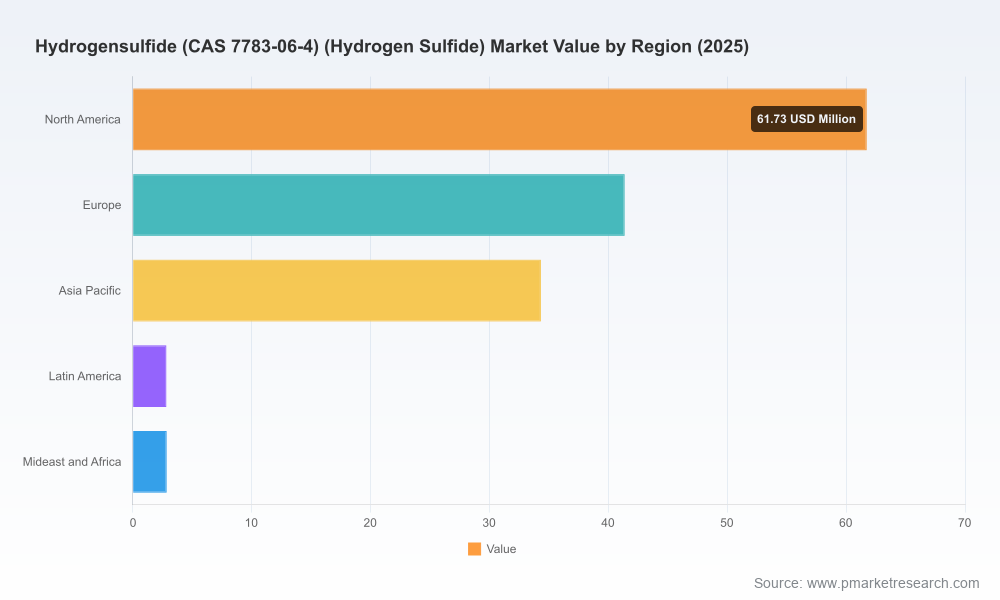

The market segmentation used in the full study covers three primary axes: by region (global geographies), by product type (e.g., gaseous, liquefied and other formats), and by application (including oil & gas, chemical manufacturing, pulp & paper, water treatment, and other industrial uses). In this preview we outline the structure and the strategic implications of each axis, but we intentionally withhold granular percentage or monetary splits to preserve the value of the full report.

- By region: Geographic demand and logistics dynamics vary materially; regional regulatory regimes and refining/chemical industry footprints are key determinants of local pricing and availability.

- By product type: Different handling, storage, and transportation requirements for gaseous vs. liquefied H2S create distinct cost and safety profiles — a critical factor for procurement and on-site decisions.

- By application: End-market dynamics (e.g., refinery sulfur recovery vs. specialty chemical synthesis) influence acceptable purity grades, contract terms, and supplier selection criteria.

Market structure and concentration

The H2S market is markedly concentrated. Our assessment identifies high market-share capture by the top three and top five global suppliers, implying notable barriers for new entrants and meaningful pricing power for incumbents. Specifically, CR3 and CR5 metrics indicate that the largest suppliers collectively command a dominant share of global supply. For buyers, this concentration raises the strategic importance of supplier risk assessment; for potential entrants and investors, it highlights the premium on strategic differentiation and niche specialization.

Competitive landscape — incumbent profiles and strategic postures

The competitive map is shaped by global industrial gas majors alongside specialized regional suppliers. The full report contains supplier-level scorecards; here we summarize the strategic positioning of core players:

- Advanced Specialty Gases (USA): A focused player known for offering high-purity hydrogen sulfide in cylinders targeted at industrial and analytical customers. Their strength lies in agility, niche purity offerings, and close customer relationships—attributes that make them an attractive partner for laboratories and precision chemical manufacturers.

- Air Liquide (France): A diversified industrial gas leader that positions H2S within broader process gas portfolios, supplying H2S as a process intermediate and for sulfur production via the Claus process. Their scale and integrated service model support large refinery and chemical complex contracts.

- Praxair / Linde (USA origin): Operating with global reach and deep distribution networks, they supply H2S in cylinders and other formats for refinery sulfur recovery and chemical feedstock use. Their extensive logistics and storage capabilities reduce delivery risk for large-scale consumers.

- Air Products (USA): Offers H2S for organosulfur synthesis and petroleum refining, leveraging industrial gas expertise to bundle supply with related gases and services, which can drive customer stickiness.

- Linde (global): Supplies anhydrous hydrogen sulfide for sulfuric acid production and various feedstock applications; Linde’s advantage is in integrated industrial gas solutions and multinational account management.

For buyers and competitors, each profile suggests distinct negotiation levers: boutique providers offer flexibility and niche purity; global majors provide security of supply, integrated services, and contractual sophistication.

What the full report delivers — practical components

PW Consulting’s full market study is purposely structured to be operationally actionable for 2026 deployment. Key components include:

- Comprehensive historical data (2020–2025) and forward projections (2026–2032) with scenario bands and sensitivity testing around feedstock and refining cycles.

- Supplier-level profiles and a procurement playbook: contract templates, negotiation levers, and contingency clauses tailored to H2S supply.

- Cost-to-serve and delivered-price modeling by product format and region, inclusive of transport, storage, and compliance burden estimates.

- Regulatory risk matrix and safety-compliance checklist with jurisdiction-specific triggers for investment.

- M&A & alliance screening toolkit: valuation multiples, integration risk checklists, and a roll-up playbook for building scale in a concentrated market.

- Operational readiness framework: inventory sizing heuristics, emergency response templates, and CAPEX optimization models for on-site handling and treatment.

Priority actions for 2026

Based on the market trajectory and competitive dynamics, we recommend executives prioritize the following actions in 2026:

- Lock in layered supply: Blend longer-term contracts with defined flex windows and spot capacity to balance price certainty and responsiveness to market swings.

- Invest in handling and safety: Upgrade on-site monitoring and incident response capabilities to meet rising regulatory expectations and reduce insurance and incident risk.

- Assess vertical options: Evaluate downstream integration opportunities (e.g., sulfur recovery partnerships) that can convert H2S exposure into higher-margin products.

- Targeted M&A or partnerships: For firms seeking scale, pursue bolt-ons that add distribution reach or specialty-purity capabilities rather than large, undifferentiated capacity.

- Embed scenario-based planning: Use the report’s scenario outputs to stress-test working capital, inventory, and capex decisions under fluctuating oil & gas activity.

How to read this preview — and next steps

This briefing intentionally demonstrates analytical depth while reserving the complete granular datasets and supplier-level volumes for the full report. Subscribers will obtain the segmented tables, regional and application breakdowns, delivered-price curves, and supplier scorecards — the exact inputs corporate planners need to convert strategic intent into executable 2026 plans.

For teams preparing budgets, negotiating supplier agreements, or evaluating strategic transactions in 2026, the full PW Consulting H2S market report provides the empiric backbone and transaction-ready tools to act decisively. To obtain the complete dataset and the practical toolkits referenced here, access the full study through PW Consulting’s market intelligence portal.

Closing

Hydrogen sulfide is a mature yet strategically important industrial commodity. Its steady growth, concentrated supplier base, and application-critical nature make disciplined planning and supplier engagement essential in 2026. This preview maps the strategic contours — the full report equips your team with the granular evidence and operational playbooks needed to convert insight into advantage.

For detailed analysis of this topic, please visit the official page:Hydrogensulfide (CAS 7783-06-4) (Hydrogen Sulfide) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com