Allergan Botox in Dubai: A Non-Surgical Beauty Solution

Health |

2026-05-06 05:48:08

As PW Consulting’s senior industry analyst, I present a concise, decision-focused preview of our Solvent Naphtha Market study (base year 2025). The market has transitioned from a modest recovery phase into a structurally expanding sector: global revenue rose steadily over 2020–2025 and, at a projected compound annual growth rate (CAGR) of 5.72% over the forecast horizon, it is expected to continue expanding through 2032. For executives and strategy teams planning for 2026, this research is designed as an actionable intelligence toolkit — highlighting where to allocate capital, where to de-risk portfolios, and how to shape commercial responses in a market balancing commodity swings, regulatory tightening, and concentrated supplier power.

Solvent Naphtha Market

Timing and trajectory: With the market base anchored in 2025 and robust growth projected into the early 2030s, 2026 is a pivot year for translating medium-term forecasts into concrete investments — whether that means incremental capacity, targeted product development, or supply‑chain resilience measures.

Solvent Naphtha Market

Commodity volatility meets regulatory tightening: Recent price softness in naphtha and concurrent updates in hazard classification and registration frameworks mean operating cost trajectories and compliance burdens are shifting simultaneously. Firms that reconcile these dynamics early will secure margin and access advantages.

Solvent Naphtha Market

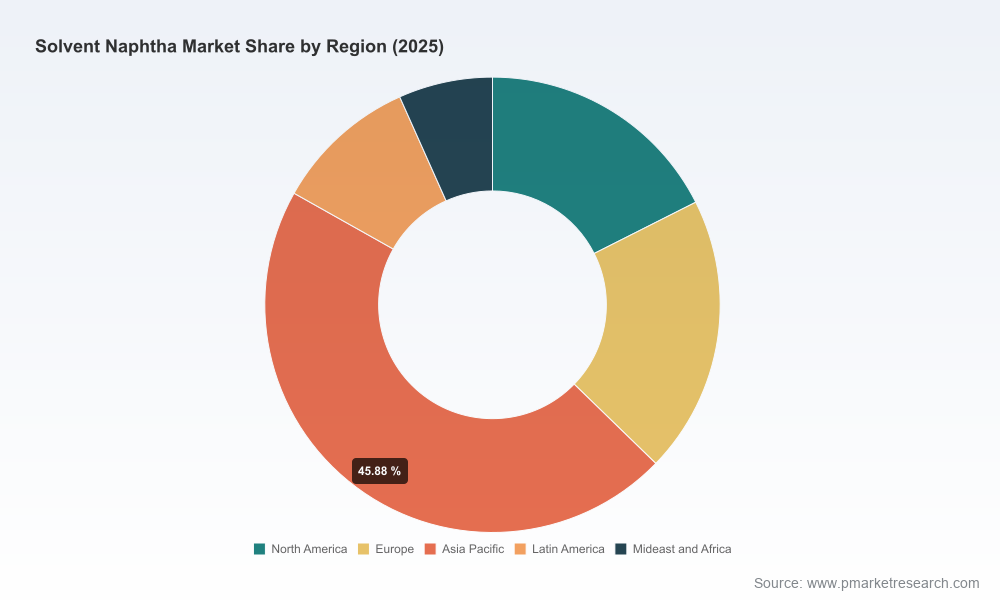

Concentration and consolidation signals: The sector exhibits a mid-to-high concentration profile, which has implications for pricing power, partnership strategies, and M&A opportunity sets. Our study situates these dynamics against competitive positions and likely strategic responses.

The full PW Consulting report is structured to move beyond descriptive market sizing into prescriptive actions. Highlights include:

High‑fidelity market sizing and forecast model (base year 2025) that translates top‑line growth into demand drivers and unit economics across the value chain.

Segmentation analytics framed for decision use — we evaluate product families, end‑use categories, and geographic demand archetypes with scenario overlays. (Note: the brief preview omits granular split numbers; the full dataset and interactive model are available in the source report.)

Supply‑chain heatmap and feedstock sensitivity analysis that link naphtha price swings to gross margin impacts and cover strategies for hedging, inventory policy, and feedstock diversification.

Regulatory and compliance tracker: a country-by-country view of hazard classification updates, REACH/registration obligations, and trade tariff implications for solvent naphtha trade flows.

Commercial playbook for producers and distributors: pricing playbooks, channel prioritization matrices, and customer profitability calculators tailored for industrial users (paints & coatings, cleaning, agrochemicals, polymers, etc.).

M&A and partnership dashboard: valuation multipliers, target archetypes, and integration risks informed by market concentration metrics and recent strategic activity across incumbents and niche specialists.

The market is populated by major integrated refiners and specialty producers, each with distinctive strategic levers. Our analysis profiles the leading players and their tactics for 2026:

Global integrated majors (examples include legacy oil & gas firms): often use solvent naphtha as part of a broader distillate/product portfolio and can leverage scale for feedstock integration and global distribution. Their strategy tends to prioritize margin capture through integrated refining-to-markets logistics and product standardization for large industrial buyers.

Refiners and specialty producers: these firms emphasize product differentiation (e.g., specialty aromatic grades, high‑purity streams) and more bespoke customer service for coatings, inks and adhesives markets. Their agility is a commercial advantage, enabling quicker response to regulatory formulation changes.

Pure-play specialty firms: smaller, focused companies compete on technical service, niche grades and local distribution networks. They can command premium pricing in specific end‑uses but are more exposed to feedstock price swings and regulatory compliance costs.

Key company profiles in the study include global majors and specialty manufacturers (selected names examined in depth). Each profile covers strategic positioning, product portfolio focus, supply footprint and potential near‑term moves (pricing posture, capacity investments, or partnership targets). The report’s competitive heatmap synthesizes these profiles against supplier concentration metrics to identify who is likely to lead price cycles, who is positioned for premiumization, and where white spaces exist for entrants.

Price environment: Naphtha prices in North America softened materially in early 2026, reflecting weaker petrochemical demand. For buyers, this can be an opportunity to lock favorable terms; for sellers, it calls for margin management and efficiency levers.

Hazard classification and labeling: Solvent naphtha has been subject to updated hazard categorization under recent COINCE guidelines, which affects labeling, transport and end‑user compliance costs. Anticipate reformulation and documentation demands from industrial customers as they internalize new labeling rules.

Registration and nomenclature: Hydrocarbon solvents fall under REACH and related registration regimes, with HSPA naming conventions applying to C9‑C12 aromatic variants. Compliance roadmaps are a must-have for anyone trading into regulated markets.

Trade policy: Specific tariff treatments for naphthas influence trade economics — customs duties and schedule classifications should be part of cross-border sourcing models and transfer pricing considerations.

Supply disruptions: Geopolitical or domestic stock concerns in important consuming countries have surfaced periodically. Firms should scenario‑test four‑month supply interruptions and maintain contingency plans for alternate feedstocks and logistics options.

Operational resilience: Move beyond inventory as a stopgap. Invest in dual‑sourcing, flexible blending capability and short‑term offtake agreements that allow rapid feedstock switching. Model the impact of price dips and spikes on cash flow under multiple demand scenarios.

Regulatory readiness: Prioritize compliance projects that reduce time‑to‑market friction (e.g., updated SDS management, REACH dossiers, and label templates). For manufacturers supplying industrial formulators, offer compliance support as a value‑added service.

Commercial sharpening: Reassess customer segmentation and profitability by application. Where possible, move up the value chain through technical service offerings and formulation partnerships to protect margins from commodity commoditization.

M&A and portfolio optimization: Given the sector’s concentration dynamics, 2026 is a window for bolt‑on acquisitions to secure technical capability or regional logistics. Our M&A dashboard identifies attractive target archetypes and integration pitfalls.

Sustainability positioning: Even commodity solvent markets are evolving under sustainability scrutiny. Develop low‑VOC, lower‑aromatic options and clearly communicate lifecycle impacts to industrial customers to preempt regulatory and customer-driven substitution risks.

This study is intended to be a working tool for strategy teams, commercial leaders and operations executives. Practical uses include:

Board and investment committee briefings that translate macro growth and concentration signals into capital allocation decisions.

Procurement playbooks for lock‑step hedging and tactical purchasing during periods of price weakness.

Regulatory compliance roadmaps to anticipate and budget for hazard labeling and registration costs impacting product lines.

M&A prioritization and valuation calibration using the report’s concentration measures and competitive positioning matrices.

For 2026, firms that translate growth expectations into operational and regulatory preparedness will outperform. Our Solvent Naphtha Market study provides the scenario‑tested playbooks, competitive intelligence and regulatory trackers needed to make those choices with confidence. This preview intentionally omits granular segmentation figures — the full report and its accompanying interactive models contain the detailed splits, regional and application breakdowns, and downloadable datasets that directly feed budgeting, commercial planning and M&A workflows.

Contact PW Consulting to access the full dataset and an executive briefing tailored to your portfolio. Use the findings to align your 2026 capex, procurement and commercial plans with a market whose trajectory is clear, but whose window for strategic advantage is time‑limited.

For detailed analysis of this topic, please visit the official page:Solvent Naphtha Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com