Propylene Carbonate (PC) Market — Strategic Primer for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused strategic introduction to our full Propylene Carbonate (CAS 108-32-7) Market study (base year 2025). This primer synthesizes the macro trajectory, competitive dynamics, and practical implications executives must prioritize in 2026. The full report contains the granular segmentation, supplier scorecards, modelled scenarios and playbooks that decision teams will need to execute — this article intentionally surfaces the directional conclusions and strategic options while preserving the detailed, proprietary splits and tables available in the complete study.

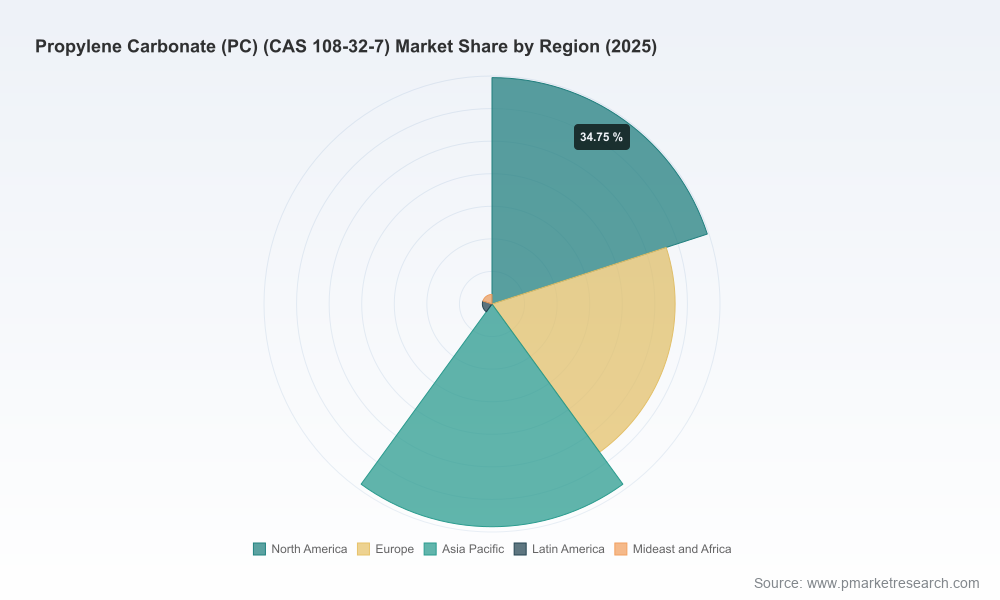

Propylene Carbonate (PC) (CAS 108-32-7) Market

Market at a Glance — A Resilient, Gradually Expanding Market

The PC market demonstrated resilience during 2020–2025, recovering from pandemic-era disruptions and shifting end‑market demand. Total market revenue expanded from roughly 376.6 Million USD in 2020 to about 448.7 Million USD in 2025, reflecting both cyclical moves and structural demand growth. Our forecast for 2026–2032 projects a steady compound annual growth rate (CAGR) of approximately 5.52%, lifting total market value toward the mid‑600 Million USD range by 2032. This mid‑single digit growth profile signals a market that is neither commodity‑style hyper‑growth nor static — it rewards operational excellence, feedstock strategy and product differentiation.

Propylene Carbonate (PC) (CAS 108-32-7) Market

Why Propylene Carbonate Matters for 2026 Strategy

- Versatility across value chains: PC is a polar aprotic solvent and intermediate used across coatings, personal care formulations, electronic and analytical chemistries, and increasingly in energy storage (battery electrolytes and capacitors). Its multi‑end‑use character means shifts in one sector (e.g., EV supply chains) materially influence overall demand.

- Regulatory and sustainability tailwinds: In 2025 regulatory updates reinforced PC’s profile as a low‑toxicity, biodegradable solvent under current REACH assessments, while manufacturers have marketed VOC‑exempt formulations to meet tightening solvent emission standards. These factors are accelerating substitution away from higher‑VOC alternatives in several end‑markets.

- Cost exposure to feedstocks: Propylene oxide (PO) is the principal upstream cost driver in PC production, accounting for a dominant share of operating costs. PO price volatility — itself correlated with crude oil price swings that ranged roughly in the US$50–90/barrel band during 2022–2024 — creates meaningful margin sensitivity for producers and pass‑through risk for consumers.

Market Dynamics: Drivers, Constraints and Structural Signals

Demand dynamics are a mix of secular and cyclical forces. Electrification and energy‑storage demand are a medium‑term structural upside for high‑purity PC grades used in lithium‑ion electrolytes; concurrently, regulatory tightening on VOCs and customer preference for low‑toxicity solvents underpin steady conversion in coatings and consumer segments. The market’s historical pattern shows a dip in 2022 followed by recovery through 2025, demonstrating both exposure to shorter‑term shocks and an underlying demand base that supports steady expansion.

Propylene Carbonate (PC) (CAS 108-32-7) Market

On the supply side, operating cost economics are dominated by feedstock sourcing and process efficiency. Given the high share of PO in total operating cost, suppliers that secure resilient PO feedstock — via integrated production, long‑dated contracts, or regional arbitrage — will hold durable advantage. Regional production strategies that leverage local feedstock availability (for example, localized CO2 or low‑cost propylene inputs) can also alter competitive dynamics without changing the fundamental demand outlook.

Competitive Landscape — Who Matters and Why

- BASF SE — With integrated Care Chemicals and Intermediates businesses, BASF combines scale with application development across coatings, personal care and battery electrolytes. Their advantage is deep customer relationships and technical service capability; competitors should assume BASF will continue to push higher‑value formulations and system‑level partnerships with OEMs.

- LyondellBasell Industries — Marketed Arconate PC as a VOC‑exempt solvent, positioning it for coatings and cosmetics segments sensitive to emissions. Their petrochemical scale provides feedstock optionality and enables competitive, specification‑driven volumes — expect continued brand positioning around regulatory compliance and formulation support.

- Huntsman Corporation — Focused on high‑purity PC for lithium‑ion electrolytes and specialty electronics applications. Huntsman’s value proposition is product specification and process control tailored to energy‑storage OEM requirements — a strategically important niche as battery chemistry adoption patterns evolve.

- Carl Roth GmbH — A laboratory and synthesis‑grade specialist, Carl Roth’s SOLVAGREEN® brand addresses research and precision synthesis users. Their business model emphasizes traceability, documentation and small‑lot flexibility — features that are increasingly valued by R&D and specialty chemical buyers.

- Taida Chemical — Represents a lower‑cost, regional producer using local feedstock benefits (including CO2‑based processing in some cases). Such players create pressure on traded prices in their served geographies and become logical partners for manufacturers seeking regional supply security.

- SMC Global & Silver Fern Chemical — Suppliers that emphasize biodegradable, low‑toxicity solvent positioning and servicing industrial cleaning, precision electronics and research markets. Their playbook centers on product stewardship and specialist application support.

Market concentration is moderate. The top three/five suppliers capture meaningful shares but do not create an oligopoly; this structure supports differentiated strategies (volume vs. specialty) and leaves room for targeted consolidation or partnership plays where fit is strong.

What Our Full Report Delivers — Practical, Transactional and Tactical

- Demand‑supply model with price and volume trajectories (2020–2032) and sensitivities to feedstock shocks and end‑market shifts.

- Cost‑to‑produce curve and PO exposure matrix, including breakeven scenarios under crude price stress testing.

- Supplier scorecards and procurement playbooks for sourcing teams (qualification checklists, dual‑sourcing templates, contract clauses for feedstock pass‑throughs and force majeure).

- Regulatory compliance matrix (REACH, VOC rules and regional registration timelines) with a checklist to accelerate market access and claim substantiation.

- Go‑to‑market blueprints for high‑purity electrolyte grades: required QA/QC, co‑development terms, and go‑to‑customer engagement steps tuned to battery OEMs.

- Scenario analysis (base, upside and downside) with quantified outcomes at a market level and guidance on hedging, inventory and CAPEX posture.

- M&A and partnership heatmap — target archetypes, valuation multipliers to expect in specialty vs. commodity segments, and integration flags.

Strategic Imperatives for 2026

- For Producers: Lock in feedstock contracts with cost pass‑through mechanisms or pursue backward integration into PO to stabilize margins. Allocate capacity to higher‑margin, high‑purity grades (electronics, battery electrolytes) while using modular production lines to flex between grades.

- For Buyers (manufacturers & formulators): Qualify at least two supply sources across regions, accelerate testing of alternative solvent blends where regulatory risk is high, and include indexation/hedging clauses in medium‑term contracts to mitigate raw‑material shocks.

- For Investors & M&A Teams: Prioritize assets with differentiated product specs, proprietary purification technology, or advantaged feedstock access. Moderate market concentration means acquisitions can rapidly scale revenue but require careful integration to protect margin structures.

- For R&D & Sustainability Leads: Leverage PC’s biodegradable profile and REACH confirmation to win formulation displacement in regulated end‑markets; invest in documentation and life‑cycle communication that maps to procurement sustainability scoring.

Risk Map and Scenario Sketch

- Base case — Mid‑single digit CAGR (≈5.5%) to 2032, steady adoption in regulated sectors and gradual penetration in electrolytes for energy storage.

- Upside — Faster EV and energy‑storage demand, paired with broader regulatory phase‑outs of legacy solvents, lifts premium high‑purity volumes and compresses commodity pricing volatility.

- Downside — A sustained spike in crude beyond historical ranges raises PO costs and compresses margins; combined feedstock shortages could shift production economics and incentivize temporary rationing or price escalations.

Conclusion — Where to Focus in 2026

The PC market in 2026 should be seen as a strategically attractive, structurally growing chemical with differentiated pockets of premium demand. Success hinges on feedstock strategy, product specification roadmaps for high‑value applications, regulatory and sustainability positioning, and disciplined commercial execution. Our full PW Consulting study equips commercial, procurement and M&A teams with the quantitative models, supplier benchmarks and transaction roadmaps necessary to translate the mid‑single digit market growth into outsized commercial returns.

To access the complete datasets, the full segmentation breakdown, and the operational playbooks referenced here, please consult the full PW Consulting Propylene Carbonate Market report on our website — the granular tables, model files and supplier scorecards are provided there for licensed subscribers.

For detailed analysis of this topic, please visit the official page:Propylene Carbonate (PC) (CAS 108-32-7) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com