PW Consulting Report: Linear Sorter Market to Expand from USD 3,240.5 Million in 2025 to USD 5,289.27 Million by 2032 at a 7.25% CAGR

Other |

2026-07-02 12:43:46

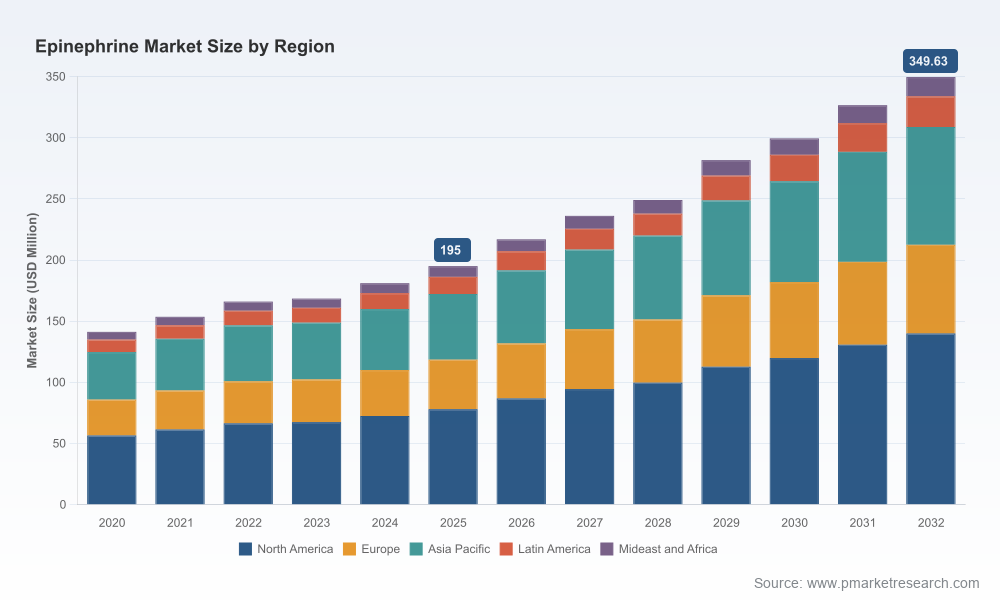

As lead industry analyst at PW Consulting, I present a concise strategic brief that frames the commercial, regulatory, and operational levers companies must command in 2026 to win in the epinephrine market. Our latest study, anchored on a 2025 base year and projecting through 2032, shows a robust market trajectory: from a global market of approximately USD 195.0 Million in 2025 to a projected USD 349.6 Million by 2032, representing a compound annual growth rate (CAGR) of about 8.8% over the forecast period. This brief highlights the strategic insights derived from that analysis while intentionally withholding granular segment tables to encourage engagement with the full report.

Epinephrine Market

Epinephrine remains the frontline therapeutic across acute allergic reactions, cardiac arrest interventions, and diverse emergency settings. Demand dynamics are being reshaped simultaneously by device innovation (needle-free and smart auto-injectors), hospital pharmacy workflow changes (premixed IV bags), and an increasingly complex regulatory and supply environment.

Epinephrine Market

The market is growing at a mid-to-high single-digit pace and is characterized by moderate concentration: approximately 42.5% of global revenues are held by the top three players and about 55.2% by the top five—enough concentration to reward scale but not so consolidated that disruption is improbable.

Epinephrine Market

Shortage risk and regulatory attention remain high. Epinephrine's placement on vulnerable/shortage lists and intermittent supply alerts continue to influence purchasing behavior, pricing strategies, and contracting practices across health systems and payers.

Quantitative market sizing and forecasts (2020–2025 historical base; 2026–2032 projections) with transparent methodology and scenario sensitivity that captures supply-constrained and accelerated-adoption paths.

Go-to-market playbooks for product formats that matter to buyers (ambulatory auto-injectors, needle-free alternatives, hospital-ready premixed IV solutions), including channel economics, margin modeling, and payer negotiation levers.

Supplier risk heatmap that maps critical raw material, manufacturing site, and regulatory bottlenecks—designed to guide sourcing and inventory decisions at the enterprise level.

Competitive benchmarking and strategic profiles of incumbent and emerging competitors, with implied threat/opportunity matrices for licensing, M&A, and co-promotion.

Operational playbooks for hospital pharmacy adoption of premixed IV products, and commercial tactics for manufacturers targeting pediatric and school-based markets.

Investor-oriented intelligence including valuations, exit scenarios, and prioritized deal targets based on a proprietary scoring framework.

New generic and premixed hospital products entered the market in 2025, increasing options for institutional buyers and compressing certain price points while simultaneously exposing persistent supply fragility.

Needle-free and alternative-route innovations have crossed regulatory milestones for pediatric use, expanding the addressable market beyond traditional auto-injectors and creating new product substitution vectors for payers and institutions.

Regulatory filings and resubmissions for sublingual or alternative delivery formats are ongoing; these binary events (approvals or negative actions) will act as growth accelerants or headwinds for targeted formats.

Large legacy manufacturers continue to defend market share through portfolio breadth (branded products, authorized generics) and customer programs that reduce patient out-of-pocket costs. These tactics protect volume and blunt price erosion in certain channels.

Specialists with differentiated device features—voice guidance, needle-free delivery, or compact form factors—are carving out defensible niches. These innovations are particularly relevant for pediatric dosing, school adoption policies, and emergency responder kits.

Generic entrants and authorized generics are raising competitive intensity in commodity channels (hospital vials and basic auto-injectors). Their presence compresses margins but also increases overall market accessibility, which can expand total addressable volume.

Hospital-focused players introducing premixed IV bags are changing procurement dynamics—those products shift how hospitals manage stock and dosing, and they reframe cost drivers for institutional buyers.

Manufacturers (branded and generic): Prioritize portfolio differentiation and supply resilience. Maintain tiered offerings—premium devices with clinical differentiation (e.g., needle-free, pediatric-approved formats) alongside cost-competitive vials—to defend against both premium and commoditized threats.

Commercial leaders: Reassess pricing strategies by channel. Use value-based messaging for differentiated devices while negotiating volume-based contracts and contingency clauses with payers and group purchasers to guard against shortage-driven price volatility.

Supply chain and operations: Implement multi-sourcing strategies for critical components, increase safety stock for high-risk SKUs, and consider contractual premix supply relationships with hospital systems to lock in demand and smooth production scheduling.

Hospitals and health systems: Evaluate clinical and operational trade-offs of premixed IV bag adoption versus on-site compounding. Premixed solutions reduce bedside risk and preparation time but carry different cost profiles and supplier dependency considerations.

Investors and M&A teams: Focus on assets that offer device differentiation, pediatric-market clearance, or hospital workflow integration—these attributes command multiples in a market where scale matters but innovation can reshape share quickly.

Regulatory milestones: FDA actions (approvals, CRLs, vulnerability listings) for novel delivery formats and market entries.

Supply chain alerts: real-time shortage listings, supplier site inspections, and raw material lead-times for premix and device components.

Commercial signals: payer formulary changes, school and public-access program adoptions, and unit economics shifts tied to generic market entries.

Adoption metrics: hospital conversion rates to premixed IV products, pediatric uptake for needle-free devices, and distribution penetration into emergency services.

Our modeling synthesizes historical market activity (2020–2025), primary interviews with manufacturers, payers, and hospital pharmacy directors, plus proprietary shipment and pricing data. The study contains granular segmentation by geography, product format, and application across multiple scenarios, along with downloadable financial models and a 40+ slide strategic playbook designed for executive briefing. In this public brief we have deliberately refrained from publishing detailed regional or application-level splits and other proprietary segment tables; these are included in the full report and the accompanying data workbook available on our website.

Embed scenario-driven forecasts into budgeting and inventory planning: stress-test P&L under both supply-constrained and accelerated-adoption scenarios.

Prioritize short-listing of M&A or licensing targets that accelerate differentiated device capabilities or hospital workflow integration.

Operationalize shortage mitigation: convert strategic supply relationships into contractual assurances and create playbooks for rapid channel reallocation during disruption.

Engage payers early on value definitions for differentiated products—this is where premium pricing can be defended through demonstrable reductions in downstream emergency costs or improved adherence.

PW Consulting’s epinephrine market analysis translates rapid market growth, product innovation, and persistent supply fragility into clear strategic imperatives for 2026. Whether you are a manufacturer deciding where to invest R&D dollars, a hospital system evaluating premix adoption, a payer reassessing coverage policy, or an investor sizing M&A targets—this study provides the scenario-tested intelligence, tactical playbooks, and risk-monitoring framework necessary to act with confidence. For access to the full segmentation, downloadable modeling, and tailored workshops that unpack the exact implications for your organization, please visit our report page.

For detailed analysis of this topic, please visit the official page:Epinephrine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com