Plastic Pails (Plastic Bucket) Market — Strategic Outlook for 2026 Decision-Making

Executive preview

As PW Consulting’s senior industry analyst, I present a concise strategic introduction to our forthcoming Plastic Pails (Plastic Bucket) Market study. The market trajectory is steady and investment-grade: from a base of approximately USD 3.5 billion in 2020 the industry expands to roughly USD 4.5 billion in our base year (2025), and our model projects growth to about USD 6.1 billion by 2032. That implies a mid-single-digit compound annual growth rate (CAGR) of roughly 4.5% over the forecast horizon (2026–2032).

Plastic Pails (Plastic Bucket) Market

This article is a teaser: it surfaces the critical business implications, competitive dynamics, regulatory headwinds and opportunities that will shape procurement, product development and M&A choices in 2026 — while reserving the granular segmentation tables and proprietary scenario matrices for subscribers.

Plastic Pails (Plastic Bucket) Market

Why this study matters for 2026 corporate strategy

- Timing of regulatory inflection: 2026 is a watershed year for packaging policy in several major markets. New EU Packaging and Packaging Waste Regulation requirements come into force in August 2026 and the UK’s plastic packaging tax has been materially increased as of April 2026. These moves create immediate compliance costs and rework decisions for packaging specifiers and brand owners.

- Sustainability is now a structural procurement variable: Legislation and buyer expectations are making recycled content and end‑of‑life circularity core spec requirements rather than differentiation. Our base‑case assumes increasing incorporation of post‑consumer recycled (PCR) HDPE in pail manufacture — current field observations show PCR levels deployed in new production commonly range from ~10% up to around half of resin content in advanced implementations.

- Operational and sourcing implications: Rising recycled content mandates, tax incentives and volatility in virgin resin feedstock mean that supply chain flexibility and verified PCR sourcing will be decisive in 2026 capital and sourcing decisions.

Market trajectory at a glance

From 2020 to 2025 the market expanded at a steady pace, reaching our base-year valuation in 2025. Looking into the forecast window (2026–2032), the modeled CAGR of ~4.5% reflects a balance of growth drivers (industrial demand, foodservice and DIY segments in developing markets, and product substitution) and constraints (raw material price volatility, regulatory compliance costs, and competitive downward pressure on low-end commoditized buckets).

Plastic Pails (Plastic Bucket) Market

For executives, three takeaways are immediate: (1) the market is large enough to support premium and value tiers simultaneously, (2) sustainability-driven product premiums exist but require credible chain‑of‑custody and certification, and (3) aggregate growth does not eliminate the need for portfolio optimization — growth pockets will vary by end-use and material strategy (e.g., HDPE vs. PP and higher‑value specialty variants).

Regulatory and materials context shaping 2026 choices

- Policy accelerants in 2026: UK plastic packaging tax increases and the activation of the EU’s PPWR in 2026 materially change cost calculus for non‑recycled content. In the US, state-level requirements (for example, California’s AB 793 that set minimum PCR levels for beverage packaging) demonstrate that jurisdictional heterogeneity will persist; manufacturers and brand owners must model multi‑jurisdictional requirements into product specifications and pricing strategies.

- Resin dynamics: HDPE remains the dominant resin for pails, and conversion to higher PCR blends is well underway. However, PCR availability, quality variability and cost differentials will be the gating constraints for rapid substitution. Our on‑the‑ground supplier interviews confirm PCR content in commercially available pails ranges widely; therefore, active procurement of certified PCR and investment in testing/validation will be necessary to avoid non‑compliance penalties and reputational risk.

- Tax and incentive effects: The UK tax step-up and other lean‑toward‑recycling fiscal policies create a two-speed environment: suppliers with validated recycled-content capabilities can capture margin expansion opportunities; those without will face cost compression or must absorb compliance costs.

Demand drivers and strategic imperatives

- End‑use diversification: Demand is driven by industrial chemicals, paints and coatings, foodservice and emerging direct-to-consumer (D2C) specialty packaging. Each channel has divergent requirements for food‑contact approval, UN‑rating, color and surface finish, and these technical differences create defensible product niches.

- Premiumization vs. commoditization: While a baseline market for standardized HDPE buckets remains highly price-sensitive, opportunities in lightweighting, barrier performance, tamper-evident features and integrated dispensing exist for margin expansion. Investing in application-specific R&D or strategic partnerships to deliver certified food-contact and high-barrier pails can yield disproportionate returns.

- Supply chain resilience: Suppliers adopting multi-sourcing for PCR, vertical integration into resin reprocessing, or localizing production close to major demand centers will gain a structural advantage in 2026 and beyond.

Competitive landscape — what to watch in 2026

The market structure is moderately fragmented: the top three suppliers account for a little over one-third of global revenue, while the top five capture under half. This concentration profile indicates room for both scale-driven players and agile regional specialists.

Key players merit differentiated strategic readouts:

- Global integrated producers (example: Berry Global, Mauser Packaging Solutions): These firms compete on breadth of offering — from standard HDPE pails to PCR-blended and UN-rated solutions. Their scale enables investments in sustainable resin sourcing and certification programs, positioning them well for large B2B contracts and global brand relationships.

- Specialist rigid-packagers (example: Jokey Group, Ugur Teneke): Firms with deep injection‑moulding expertise and recyclable-design credentials are capturing value in segments where tailored closures, IML labeling and high aesthetic standards are required. Sustainability awards and trade‑show presence in 2026 underscore their strategic focus on circularity and design for recyclability.

- Regional and contract manufacturers (example: Encore Plastics, Affordable Buckets, C.L. Smith, The Cary Company): These suppliers are often preferred for domestic sourcing, reconditioning programs and fill-line integration. Their proximity to customers and flexibility make them key partners for rapid product iterations and small‑batch specialty runs.

Recent industry developments — from sustainability awards to product exhibitions at major packaging shows in 2026 — reinforce that brand owners and OEMs are actively re‑specifying packaging to meet policy and consumer expectations. Expect the next 12–18 months to be a period of supplier consolidation, certification investments and commercial renegotiation.

What the full PW Consulting study delivers (practical, actionable content)

- Scenario-based commercial models that quantify margin implications under alternative PCR price/fraction and tax regimes for 2026 procurement cycles.

- Decision frameworks for sourcing strategy (insource vs. outsource PCR, local vs. global supply) that align with five typical corporate archetypes (e.g., global brand, regional co‑packer, industrial buyer).

- Supplier selection matrix integrating technical certifications (food-contact, UN-rating), sustainability credentials (chain-of-custody, third‑party audit status) and operational metrics (lead times, minimum order quantities, regrind capacity).

- Playbooks for product innovation: lightweighting, tamper evidence, IML and multi‑material hybrid designs — including go-to-market case studies and estimated time-to-market for each option.

- Regulatory impact dashboards that translate new rules (including the UK tax increase and PPWR) into actionable compliance checklists and capital planning triggers.

How strategic buyers should use this intelligence in 2026

- Integrate PCR availability and certification verification into RFPs now — cost projections that ignore the new 2026 policy landscape will understate total cost of ownership.

- Prioritize supplier audits and dual-sourcing for PCR feedstock to mitigate single‑point exposure as price and quality will vary widely in 2026.

- Pursue targeted differentiation: invest selectively in premium features where regulatory or performance barriers raise switching costs; commoditized SKUs are candidates for strategic sourcing consolidation.

- Model scenarios for 3–5 year product roadmaps that incorporate legislative timelines (e.g., PPWR effective dates) to time CAPEX and certification investments efficiently.

Final note — what you will not find here (and why)

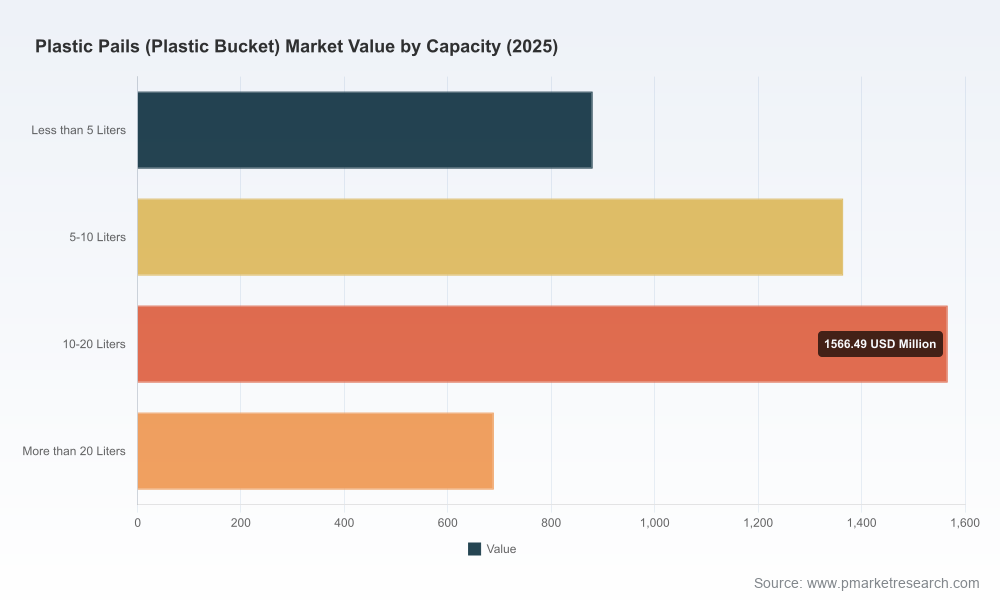

To preserve the “trailer” character of this piece, we’ve intentionally withheld the granular breakdowns — including detailed regional, material and capacity segment tables and point‑by‑point pricing matrices — that underpin our revenue and scenario models. These proprietary segment-level analytics, together with supplier scorecards and downloadable financial models, are available in the full PW Consulting report.

Next steps

If your 2026 strategy depends on packaging cost exposure, recycled-material sourcing or supplier selection, the comprehensive playbook and modeling tools in the full report will convert high‑level strategy into executable action. Contact PW Consulting to obtain the complete study, the supplier due-diligence toolkit, and a 90‑minute executive briefing tailored to your portfolio and procurement posture.

For detailed analysis of this topic, please visit the official page:Plastic Pails (Plastic Bucket) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com