Don't Let QuickBooks Error 1712 Disrupt Your Business—Fix It Now

Other |

2026-06-08 05:10:25

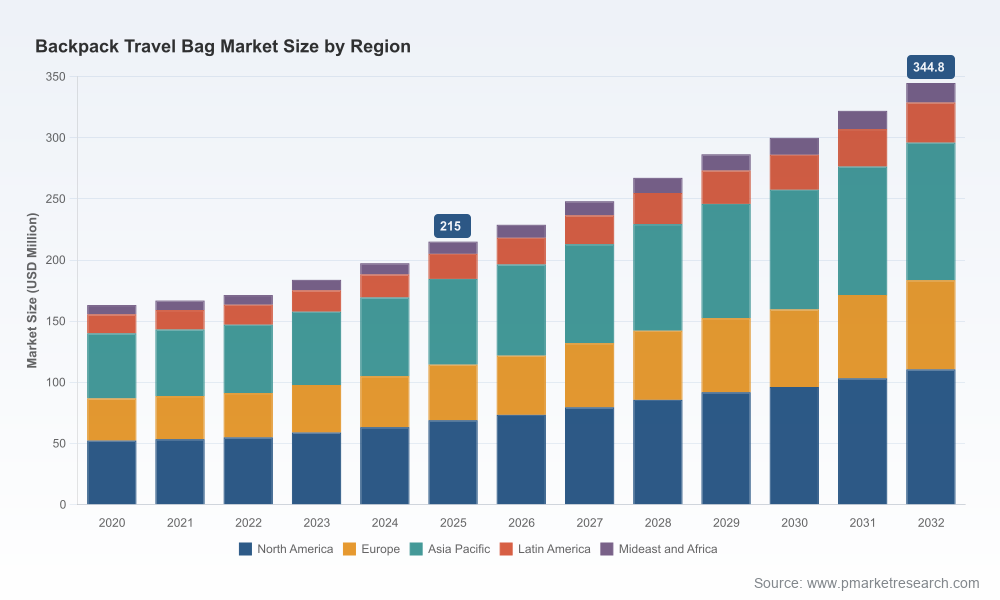

PW Consulting’s latest market study on Backpack Travel Bags positions commercial leaders to make high‑confidence choices in 2026 and beyond. Built on a 2025 base year with historical coverage from 2020–2025 and a forward view to 2032, the study quantifies the market’s structural momentum: after steady expansion through the pandemic recovery, the global Backpack Travel Bag market reached an identifiable milestone in 2025 and is expected to sustain growth at a compound annual growth rate of 6.98% across the 2026–2032 forecast window, reaching a materially larger market size by 2032 (figures expressed in USD Million). This trajectory reflects a durable intersection of travel normalization, product premiumization, and changing consumer packing behaviors.

Backpack Travel Bag Market

Corporate leaders face a compressed decision calendar in 2026: product roadmaps set now will roll into 2027 production cycles, retail partners are finalizing category assortments, and M&A windows hinge on near‑term visibility. Our study converts macro signals into decision‑grade intelligence by linking demand drivers (travel volumes, one‑bag adoption), supply shocks (material and wage pressure), and regulatory touchpoints (airline carry‑on constraints) into actionable scenarios.

Backpack Travel Bag Market

We designed the report to be a playbook for executives, not an academic compendium. Highlights of the deliverables include:

Backpack Travel Bag Market

Methodology blends primary interviews with manufacturers, retail buyers and travel‑heavy consumers, plus secondary trade flows, price scraping and on‑the‑ground factory cost checks. Importantly, while this article highlights the study’s strategic value, the full report contains the detailed segmentation tables, model files and appendices that enable scenario re‑runs.

The market remains fragmented, with top three and top five concentration metrics indicating ample room for differentiated plays (CR3 ≈ 24.6%; CR5 ≈ 26.2%). That fragmentation produces two simultaneous opportunities: scale‑driven margin capture for larger incumbents and niche premiumization for focused independents.

Recent product activity across several players (new compact and 2‑in‑1 formats, sustainability enhancements, and reinforced ballistic fabrics) demonstrates how innovation is primarily executional—materials, pack organization and airline compliance—rather than category‑redefining. This favors companies that can operationalize fast prototyping and tight retail feedback loops.

Based on our scenario work and supplier checks, we recommend the following prioritized actions for companies active in backpack travel bags this year:

Operational KPI discipline will separate winners from laggards. Track: year‑over‑year average selling price by model band, carry‑on compliance return rate, material cost index vs. realized margins, DTC conversion and repeat purchase within 12 months, and landed lead times from primary sourcing hubs. Use the report’s base scenario (6.98% CAGR) as the planning baseline; stress test upside drivers (rapid travel recovery, accelerated premiumization) and downside risks (material inflation, restrictive airline policy changes).

In this preview we deliberately refrain from publishing the full segmentation tables and per‑region or per‑application breakdowns—those granular splits are central to execution and are provided in the full report package available through PW Consulting. The report’s appendix includes downloadable model files so teams can re‑run scenarios under alternate cost and demand assumptions.

For 2026, decisions made now on sourcing contracts, SKU rationalization and channel investments will shape P&L outcomes through 2028. PW Consulting can support rapid‑turn tailored outputs: a two‑week SKU prioritization workshop, a material cost hedging playbook, or a M&A target shortlist filtered by production capability and brand fit. Contact our industry team to commission a strategic brief that maps your current book of business to the forecast scenarios and the tactical playbook summarized here.

For detailed analysis of this topic, please visit the official page:Backpack Travel Bag Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com