Feeding the Blue Economy: Aquafeed Market Set to Hit $136.8 Billion by 2036

Other |

2026-04-27 06:18:45

As the shale gas sector enters a pivotal phase in 2026, executives and investors require clarity on long-term trajectories while preserving agility for near-term shocks. PW Consulting’s Shale Gas Market study — grounded on a 2025 base year with a 2020–2025 historical review and a 2026–2032 forecast horizon — provides that clarity. The market’s macro trajectory is unambiguous: having expanded from approximately USD 61.15 Billion in 2020 to USD 92.8 Billion in 2025, the sector is projected to continue growing at a compound annual growth rate (CAGR) of roughly 5.98% across the forecast window, reaching an estimated USD 143.32 Billion by 2032. These headline figures frame the strategic choices firms must make in 2026 — the year when capitalization plans, portfolio repositioning and commercial contracts will determine who captures value through the 2030s.

Shale Gas Market

Timing and capital allocation: With the market roughly doubling from the early 2020s to the early 2030s, 2026 will be a decisive year for committing incremental capital. The report translates macro growth into actionable capital-efficiency targets — not by selling static benchmarks, but by modeling range-bound scenarios that map capex timing to price, takeaway capacity and technological adoption.

Shale Gas Market

Price-sensitivity and hedging: Public forecasts from the U.S. Energy Information Administration (EIA) point to Henry Hub price averages in the mid-single dollars per MMBtu across 2025–2027, with short-term seasonal softness expected in 2Q 2026. PW’s models synthesize these price paths with basin-level breakeven curves so companies can design hedging and contracting strategies that protect margins without foregoing upside participation.

Shale Gas Market

Operational productivity and midstream optimization: Recent operator disclosures — including production guidance revisions and midstream optimization success stories — underline that gains in per-well productivity and logistics efficiency are as impactful to enterprise value as new drilling. The study converts reported efficiency improvements into portfolio-level outcomes, illuminating which operating practices deliver the largest ROI in 2026.

Competitive posture and consolidation opportunities: Market concentration metrics show a market where leading players command a meaningful share of output; top‑three and top‑five concentration statistics indicate oligopolistic tendencies that shape pricing power and M&A dynamics. Our analysis helps buyers and sellers size asymmetries, anticipate regulatory friction and structure deals that create scalable synergies.

Dynamic scenario toolkits: Multi‑scenario supply-demand models that stress-test portfolios under alternative price, demand and policy paths; each scenario links to recommended tactical moves for 12-, 24- and 36‑month horizons.

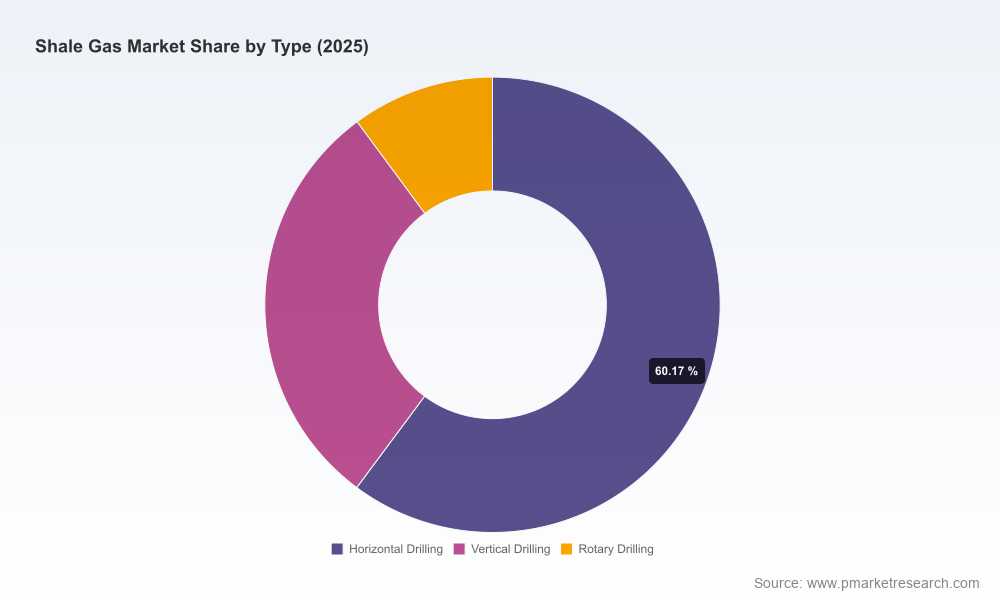

Cost and break-even mapping: Drilled-down cost curves and full-cycle breakeven ranges by technological pathway and operating model — presented so teams can prioritize retrofit vs greenfield investments. (Note: specific regional and application splits are summarized in the full report to preserve strategic exclusivity.)

Midstream capacity and bottleneck analysis: Flow constraints and capital requirements for takeaway and storage that materially affect realized wellhead value; includes practical mitigation strategies, contract structures and project-outcome sensitivities.

Commercial frameworks and contracting templates: Negotiation playbooks for long-term offtake, tolling and tolling-plus services that protect margins during periods of price volatility.

Regulatory stress tests and policy decks: Scenario planning for evolving environmental and fiscal regimes, translating policy risk into P&L and balance-sheet exposures.

M&A and partnership playbooks: Target screening criteria, valuation overlays, and integration checklists tailored for divestitures, bolt-ons and infrastructure JV structures.

The market is concentrated, with the top three players commanding a material portion of output and the top five consolidating an even larger share. This structure has three strategic consequences: (1) leading firms set the tone on pricing and infrastructure investment, (2) mid-tier operators face pressure to specialize or partner, and (3) capital markets reward demonstrable cost discipline and returns per dollar invested.

EQT Corporation (Pittsburgh, PA) — A primary shale gas producer focused on core dry-gas formations. EQT’s recent operational disclosures illustrate the power of technical uplift and midstream optimization: the company raised its 2025 production guidance in late 2025 and published full‑year results that informed its 2026 sales-volume outlook. For peers and investors, EQT’s playbook offers a template on combining drilling efficiency with downstream capacity coordination to increase realized prices and lower unit costs.

ExxonMobil Corporation (Spring, TX) — A vertically integrated major with exposure to both associated and non-associated gas in shale and tight formations. ExxonMobil’s scale and balance-sheet flexibility enable multi-asset optimization across basins, and its approach to integrating shale gas into global gas and LNG portfolios is a bellwether for price linkage and off-take strategies.

Chevron Corporation (San Ramon, CA) — Active across key plays, Chevron blends upstream discipline with a focus on lowering per-unit emissions intensity. The company’s capital-allocation philosophy and technology adoption curve help define competitive thresholds on returns required for large-scale acreage development.

ConocoPhillips (Houston, TX) — An upstream-centric operator that leverages operational scale to manage volatility. ConocoPhillips’ approach to prioritizing high-margin inventory and rightsizing rig counts is instructive for mid-tier operators balancing growth and cash returns.

Occidental Petroleum (Houston, TX) — Significant participant in shale and associated plays, with a clear focus on integrated solutions that capture oil‑linked gas value and downstream optionality. Occidental’s strategic moves highlight the interplay between petrochemical and power-sector demand and how operators can capture value beyond the wellhead.

Price baseline and volatility regime: Official EIA projections model Henry Hub pricing in the mid-single dollars per MMBtu during 2025–2027, with a seasonal trough expected in 2Q 2026. For 2026 decision-makers, this implies limited near-term upside in spot realization and elevates the importance of operational cost decreases and contractual price protection.

Midstream bandwidth as a value lever: The next wave of value capture will come from optimizing takeaway capacity, blending services and flexible offtake terms. Operators who can synchronize drilling schedules with midstream investments will mitigate discount risk and accelerate cash conversion.

ESG and financing conditionality: Debt and equity providers increasingly price emissions intensity and transition plans into cost of capital. 2026 transactions will be evaluated against decarbonization roadmaps, with financing terms favoring operators with measurable progress on methane intensity and flaring reductions.

Technology and productivity: Incremental recovery and per‑well productivity gains — from frac optimization to completions sequencing — can materially shift the return profile of drilling programs. The report isolates the operational levers with the highest ROI and models their effect across portfolios.

Board-level scenario briefings: Convert the report’s scenarios into board-ready options that link capital plans to market outcomes under three prioritized price paths.

Investment committee inputs: Use the cost-curve diagnostics and breakpoint analysis to set hurdle rates, approve drilling budgets and design contingent spend triggers tied to realized price and midstream availability.

Commercial negotiations: Leverage the offtake and tolling templates to reduce downside exposure in contracts signed in 2026, while preserving upside via market-indexed collars and flexible take-or-pay structures.

M&A and portfolio optimization: Apply the target-screening filters and integration checklists to evaluate bolt-on acquisitions and carve-outs where scale or infrastructure control offers outsized value capture.

This briefing intentionally showcases macro-scale market sizing, trajectory and the strategic frameworks embedded in PW Consulting’s work while withholding granular split tables and proprietary sub‑segment models that are core to transactional decision-making. Those detailed regional, type and application breakdowns — along with downloadable scenario spreadsheets, basin-level break-evens and interactive midstream maps — are available through the full report package.

For executives preparing 2026 board packages, investment committees, or M&A strategies, PW Consulting offers tailored workshops to convert this analysis into prioritized action plans. Our advisors can run a focused one‑day scenario lab using your balance-sheet and portfolio to produce an executable 90‑day playbook aligned with risk appetite and capital strategy.

Contact PW Consulting to schedule a briefing and obtain the full Shale Gas Market study and companion analytics — the detailed segmentation, downloadable models and proprietary dashboards that solidify the choices that will define market leadership through 2032.

For detailed analysis of this topic, please visit the official page:Shale Gas Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com