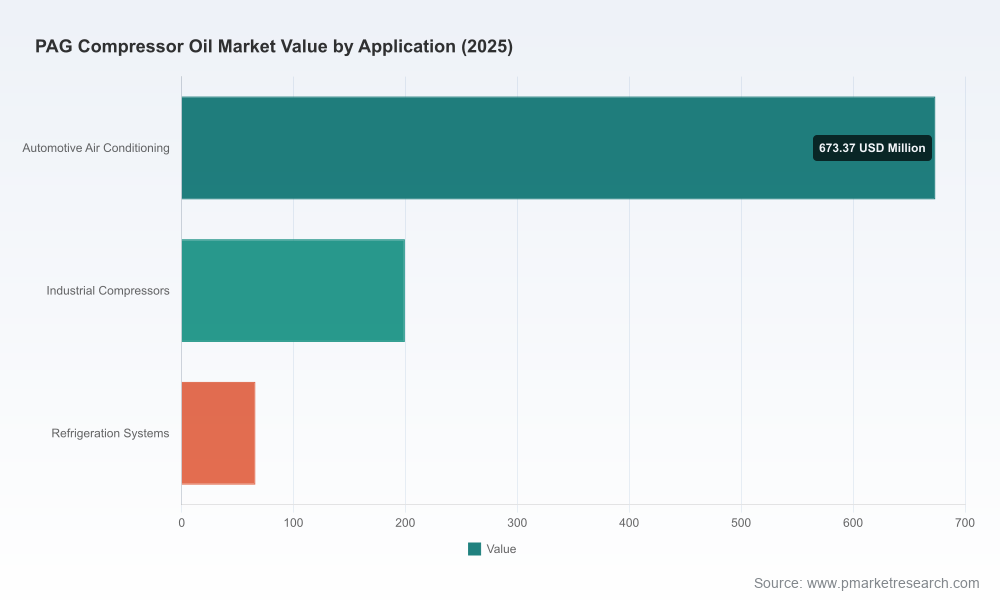

PW Consulting: PAG Compressor Oil Market Poised to Reach USD 1,459.09 Million by 2032 at a 6.51% CAGR — Asia Pacific Leads with USD 397.9M

Other |

2026-07-13 13:45:00

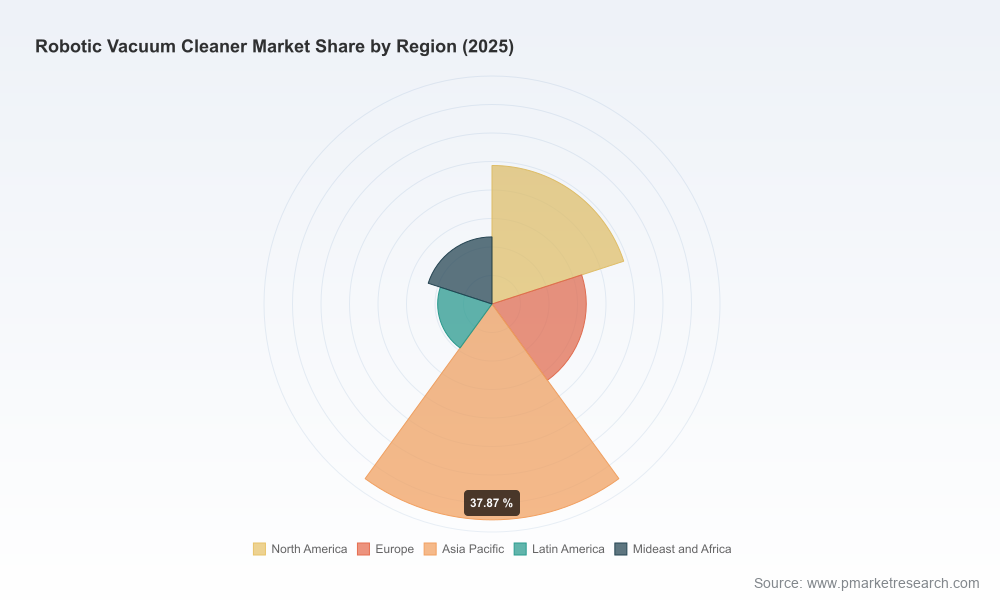

As senior industry advisors at PW Consulting, we prepared this strategic introduction to our Robotic Vacuum Cleaner Market research to help executives make decisive moves in 2026. The research uses 2025 as its base year and spans a historical window from 2020–2025 with forward-looking projections through 2032. At the macro level the market exhibits robust expansion — a compound annual growth rate of 12.45% — with the total market reaching approximately USD 4,980 million in 2025 and an expected trajectory that more than doubles by the end of the forecast period. These headline metrics are more than vanity figures: they signal materially different investment, product, and go-to-market choices for incumbents and new entrants alike.

Robotic Vacuum Cleaner Market

Investment prioritization: The growth runway and technology inflection points make it essential to re-weight R&D and capital allocation towards capabilities that protect margin while enabling premium pricing (AI navigation, hybrid cleaning systems, service ecosystems).

Robotic Vacuum Cleaner Market

M&A and partnerships: With a moderately concentrated supplier base (top-three firms command a clear majority share and the top-five firms hold a substantial portion), acquisitive growth and targeted partnerships will be the fastest route to capability expansion and market access.

Robotic Vacuum Cleaner Market

Regulatory and lifecycle risk mitigation: Emerging battery-handling and lifecycle regulations require immediate product redesign and supply-chain adjustments to avoid non-compliance costs and reputational risk.

Commercial model reconfiguration: Rapid innovation in hardware-software integration and subscription services implies new pricing, after-sales, and channel strategies to capture recurring revenue.

The market’s strong headline CAGR masks several structural shifts that will determine winners and losers over the next three to five years. Our analysis identifies five converging dynamics:

Technology convergence: AI-driven navigation, advanced mopping and suction systems, and hybrid designs are displacing single-function devices. Notable innovation themes include machine vision, sensor fusion, and creative locomotion that enable new use-cases (for example, multi-level homes and mixed flooring types).

Platform and ecosystem competition: Players that integrate vacuums into smart home ecosystems and deliver ongoing value via updates, consumables, and services will see higher lifetime value and lower churn.

Consolidation pressure: Market concentration metrics show that leading players exercise meaningful share and influence on standards, component supply, and retail access. This elevates the strategic importance of alliances, white-label deals, and selective acquisitions.

Regulatory and sustainability constraints: Customs classifications, dangerous-goods and lithium-battery labeling, and an accelerating push toward automated disassembly for battery removal are already shaping product design and reverse-logistics. The EU’s lifecycle-focused regulations remain a critical compliance frontier for global suppliers.

Channel and service evolution: Retail and e-commerce remain important, but service networks, subscription consumables, and trade-in/repair propositions are emerging as primary profit centers beyond initial device sales.

The competitive map combines rapid product innovation with strategic ecosystem plays. At the forefront are established OEMs and fast-scaling challengers deploying differentiated hardware architectures and software platforms. A snapshot of core competitors — and the strategic implications — follows.

Roborock Technology Co., Ltd. (Beijing, China) — Roborock’s recent introduction of a wheel-leg architecture demonstrates a bold move to eliminate traditional constraints of mobility (stairs and steep slopes). This capability broadens addressable homes and supports premium positioning. Strategic implication: mobility innovation is a defensible moat if matched with navigation software and service support.

Ecovacs Robotics Co., Ltd. (Suzhou, China) — Through its DEEBOT series, Ecovacs emphasizes suction performance and intelligent navigation. Their strength is in balancing cost-performance for mass adoption. Strategic implication: scale-oriented players will compete on component sourcing and retail partnerships while pursuing adjacent services.

Dreame Technology Co., Ltd. (Suzhou, China) — Dreame focuses on mechanical innovation (retractable leg mechanisms) and high-suction systems for efficient home cleaning. Strategic implication: mechanically novel designs can seize shelf space and differentiate in mid-premium segments but require manufacturing sophistication and strong after-sales networks.

Anker Innovations / eufy (Changsha, China) — Eufy’s Omni series combines high-suction performance with self-cleaning and hydrojet mopping. Their product roadmaps indicate a tilt towards integrated base-station intelligence and service automation. Strategic implication: incumbents that integrate dock-side intelligence reduce user friction and lock in consumable revenue.

Samsung Electronics Co., Ltd. (Seoul, South Korea) — Samsung’s Bespoke AI Jet Bot line demonstrates how household appliance leaders leverage chip and ecosystem advantages (SmartThings, AI processors) to deliver premium user experiences. Strategic implication: companies with broader consumer electronics ecosystems can rapidly bundle services, accelerating household adoption and margin capture.

Recent product announcements at CES 2026 underscore these shifts. Examples include wheel-leg mobility, extendable steam and mop capabilities driven by on-device AI processors, and multifunctional base stations with self-cleaning and sanitization features. These launches are not incremental; they point to differentiated value stacks where hardware, software, and consumables converge to produce sustainable revenue streams.

Tariff and customs: Robotic vacuums are categorized under specific tariff lines that affect landed costs and can change sourcing economics. Carefully model tariff sensitivity in your cost and pricing simulations.

Battery handling and packaging: Dangerous-goods packing regulations and mandatory lithium labeling are non-negotiable for distribution, particularly for air freight. Compliance failures lead to shipment rejections and brand damage.

End-of-life and disassembly requirements: Policy momentum toward automated disassembly for battery removal is increasing. Product teams should prioritize modular battery architecture and serviceable components now to avoid redesign costs later.

Lifecycle environmental standards: The EU’s lifecycle-driven rules remain active and will likely become a template for other jurisdictions — factor environmental compliance into product roadmaps and supplier selection.

The full PW Consulting report is a hands-on toolkit designed for boardrooms and operating leaders. Highlights include:

Scenario-based market forecasts and stress tests calibrated to realistic technology adoption curves and economic sensitivities.

Competitive positioning maps and capability scorecards for the leading suppliers, with action-oriented strategic moves tailored to different player archetypes (incumbent, challenger, channel partner).

Product feature-to-value matrices and prioritized R&D roadmaps that show which investments unlock premium pricing versus scale economics.

Go-to-market playbooks for retail, direct-to-consumer, and service-as-a-product models, including channel economics, margin models, and partner selection criteria.

Regulatory compliance checklists, reverse-logistics and battery EoL blueprints, and supplier qualification templates targeted at minimizing compliance and environmental risk.

M&A screening frameworks and a methodology for valuing capability targets (software, mobility, base-station intelligence) rather than revenue multiples alone.

Interactive financial models: TCO calculators, pricing elasticity simulators, and ROI templates to evaluate product and service launches over 3–5 year horizons.

Note: segment-level tables, regional breakouts, and granular pricing datasets are deliberately withheld from this preview to protect the strategic integrity of the analysis and to guide stakeholders to the full research package available through our portal.

0–90 days: Run a rapid SKU and cost-to-serve audit focused on battery, dock, and consumable economics. Initiate regulatory gap analysis for shipping, labeling, and recycling obligations.

3–9 months: Pilot mobility or hybrid prototypes in two representative markets; test subscription bundles tied to base-station services. Begin supplier qualification for battery redesign and modularization.

9–18 months: Lock in channel partnerships for premium service distribution, accelerate software integration with major smart-home ecosystems, and deploy reverse-logistics pilots for battery EoL handling.

18+ months: Execute targeted acquisitions or strategic alliances to secure AI navigation IP, servicing networks, or proprietary base-station technologies identified in your M&A screening.

For executives deciding the fate of product portfolios, capital allocation, and partnership strategies in 2026, the imperative is clear: act early on modularity, regulatory compliance, and software-enabled service monetization. The market’s compound annual growth of 12.45% and the projected expansion from a mid-market base in 2025 to a materially larger market by 2032 create attractive opportunities — but only for firms that align R&D, operations, and go-to-market strategies with the structural shifts described above.

This preview is intended to frame strategic choices and highlight practical next steps. For full access to the dataset, regional and segment-level modelling, competitive scorecards, and downloadable financial templates, please consult the complete PW Consulting Robotic Vacuum Cleaner Market report on our research portal. The full package contains the detailed intelligence that operational leaders need to execute confidently in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Robotic Vacuum Cleaner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com