Fabric Softener Market Growth: Latest Trends, Demand Analysis & Forecast

Art |

2026-05-27 08:25:37

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present a forward-looking introduction to our new Rugs and Carpets Market study. This briefing synthesizes the most consequential trends, regulatory shifts, commercial signals, and competitive moves that will shape executive choices in 2026. The analysis distills macro trajectory and high-impact strategic levers while preserving the granular segmentation tables and proprietary scenarios that appear in the full report — consider this a high-fidelity trailer designed to direct boards, corporate strategy teams, and investors to the primary research for transaction-grade detail.

Rugs and Carpets Market

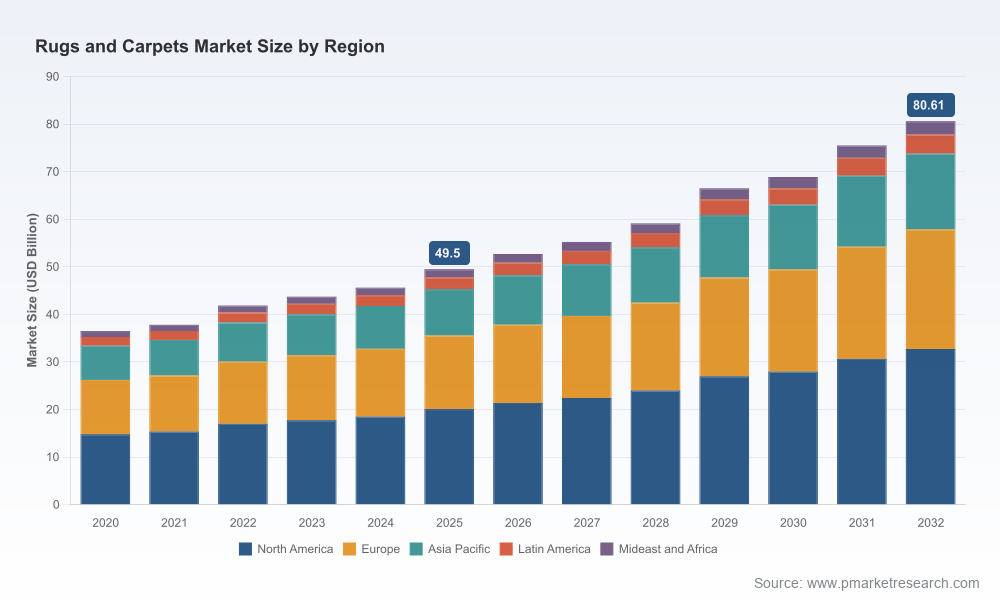

The global rugs and carpets market has entered a sustained growth phase. By our base year, 2025, the market size reached approximately USD 49.5 Billion, following steady expansion through the 2020–2025 period. Our modeling projects a compound annual growth rate (CAGR) of about 7.25% across the 2026–2032 forecast window, culminating in an estimated market north of USD 80 Billion by 2032.

Rugs and Carpets Market

What does this mean for leadership in 2026? Growth at this scale creates simultaneous opportunity and complexity: volume growth supports upstream investments and capacity expansion, while rising regulatory, sustainability, and design expectations require strategic investment in materials science, traceability, and new commercial models. The winners will be those that can convert top-line growth into defensible margin expansion through differentiated product strategies and operational agility.

Rugs and Carpets Market

Regulatory Acceleration on Chemicals and Transparency. Since late 2024, state-level and federal actions in major markets have accelerated restrictions and reporting obligations on per- and polyfluoroalkyl substances (PFAS). Several U.S. states have introduced bans and labeling requirements, and the EPA has signaled expanded reporting for chemical uses relevant to textiles. For manufacturers, this shifts PFAS from a compliance checkbox to a strategic input risk — affecting supplier selection, reformulation timelines, and product labeling strategies.

Certification and Indoor Air Quality Standards. Third-party labeling programs for low-VOC carpets and adhesives remain a primary route to specification in commercial projects and institutional procurement. Expect building-specifiers and ESG-mandated buyers to prioritize certified products, accelerating demand for certified materials and integrated documentation across the supply chain.

Trade Shows and Market Access Shaping Demand Signals. Expanded trade fair agendas and the rescheduling of major industry expos are increasing the velocity of trend dissemination and international sourcing. These events are already functioning as de facto product-accelerators for novel materials, circular economy pilots, and premium design collections — a practical channel for testing product-market fit ahead of full commercial rollouts.

Design and Consumer Preferences. Color palettes, texture innovation, and hybrid product formats (for example, modular tiles and mixed-fiber area rugs) continue to migrate from commercial specification into mainstream residential demand. Design-led collections remain a reliable margin lever for brands that can align marketing, distribution, and project-specification channels.

The competitive map is characterized by strong-capability peers, vertical integrators, and design specialists. Top global players range from multinational manufacturers with integrated upstream capacity to niche designer brands focused on high-end interiors. Market concentration remains relatively low compared with other floorcovering sectors — the top tier of firms accounts for a modest share of total revenue, leaving substantial room for regional leaders and specialized innovators.

Large integrated manufacturers (e.g., Mohawk Industries, Shaw Industries). These firms leverage scale across carpet, rug, and flooring portfolios to defend channel relationships, optimize global sourcing, and invest in stain-resistant and performance-fiber platforms. Their scale makes them first movers on supply-chain transparency programs and recycling initiatives.

Sustainable innovators (e.g., Interface, Tarkett, Forbo). Companies with early circularity programs and recycled-fiber products are converting sustainability credentials into specification wins in office and public-sector projects. Their playbook — combining take-back programs, recycled content claims, and lifecycle accounting — is instructive for manufacturers seeking to move beyond compliance to value creation.

Regional manufacturing champions (e.g., Oriental Weavers, Beaulieu). Vertically integrated supply chains and export networks enable these firms to capture price-sensitive markets and respond rapidly to trade shifts. Their strategies emphasize production flexibility and distribution partnerships.

Design-driven premium players (e.g., Stark Carpet, Masland). Designer and heritage brands continue to command premium pricing through customization, curated palettes, and project-focused sales channels. Recent product introductions underscore how color and storytelling can be used to maintain margin in a growing market.

For 2026, strategic choices by these players will set the competitive tempo: investments in circular manufacturing, product certification, and PFAS-free formulations will be primary differentiators. Our competitive profiles in the full report map capability gaps, partnership pathways, and acquisition targets for each archetype.

The full study is structured to be immediately operational for strategy teams, commercial leaders, and M&A desks. Key deliverables include:

Forecast models and scenario sets — baseline, accelerated adoption, and disruption scenarios covering 2026–2032 with sensitivity to raw material inflation and regulatory shocks.

Strategic playbooks tailored to manufacturers, distributors, and designers: capacity planning, supplier de-risking, and route-to-market optimization.

Regulatory & materials risk map — a pragmatic implementation guide for reformulation timelines, labeling updates, and compliance cost modeling tied to procurement calendars.

Commercial go-to-market tools — buyer personas, specification decision trees for architects and facility managers, and channel economics for premium vs. value segments.

Supply-chain archetypes & supplier matrix — profiles of upstream fiber producers, dye houses, and finishing partners with recommended diversification and nearshoring strategies.

M&A and partnership playbook — target screens, synergy models, and integration checklists for capabilities such as modular tile systems, recycling technology, and proprietary finishing chemistries.

Trade-show and innovation calendar — an actionable events roadmap aligned to product launch windows and specification cycles.

Prioritize chemical roadmap and traceability. Start immediate supplier audits and invest in validated test-and-trace systems. Regulatory lead times are shortening; product relabeling and reformulation projects should be treated as strategic investments, not tactical adjustments.

Define a differentiated sustainability narrative. Certification alone is table-stakes for institutional buyers. Combine certification with take-back pilots, verifiable recycled-content claims, and lifecycle cost calculators to win specification and justify premium pricing.

Segment product portfolios by route-to-market economics. Align high-touch design collections and customization services with premium channels, while optimizing cost and logistics for volume-oriented contract and retail lines.

Use trade shows strategically. Treat expanded expos as low-cost market experiments: pilot new materials, collect specifier feedback, and pre-sell accredited lines to mitigate launch risk.

Consider M&A to accelerate material capability. Acquiring technology or recycling partners can compress time-to-market for circular products and create defensible supply advantages.

Model price and margin under multiple stress tests. Use scenario planning to stress raw material volatility and regulatory compliance costs; embed hedging or strategic inventories into procurement playbooks.

Our study is built to inform decisions at three horizons: near-term compliance and go-to-market actions (0–12 months), medium-term capability and portfolio moves (12–36 months), and long-term structural choices (36+ months). The combination of market-scale forecasts, regulatory roadmaps, and actionable playbooks converts macro trends into operational milestones — essential for boards allocating capital, commercial leaders prioritizing SKUs, and private-equity teams sizing acquisitions.

Importantly, while this briefing lays out the strategic contours, the full report contains the segmented demand matrices, region-by-region scenarios, price and volume forecasts, and the detailed competitive benchmarking that operational teams require to execute with confidence. Those segmented tables and confidential unit economics are intentionally reserved for the full release to ensure that subscribers and active decision-makers have the complete, transaction-ready dataset.

If you are evaluating supply-chain resilience, R&D prioritization, or acquisition opportunities in 2026, use this study as the primary evidence base for board-level deliberations.

For procurement, R&D, and commercial teams, commission a tailored deep-dive (we offer bespoke modules) that maps your current product lines against the regulatory calendar, certification requirements, and the buyer-specification pathways we identify.

To access the full dataset, segmented forecasts, and the complete playbook, please consult the PW Consulting report page where the comprehensive annexes, downloadable models, and proprietary templates are available for subscribers and corporate clients.

In volatile regulatory and innovation climates, clarity trumps confidence. This study is designed to give you both — a clear map and the tools to act. PW Consulting stands ready to translate these insights into execution plans tailored to your role in the rugs and carpets value chain.

For detailed analysis of this topic, please visit the official page:Rugs and Carpets Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com