Disodium Nucleotide Market Size, Analytical Overview, Growth Factors, Demand, Trends and Forecast By 2031

Other |

2026-02-09 10:16:00

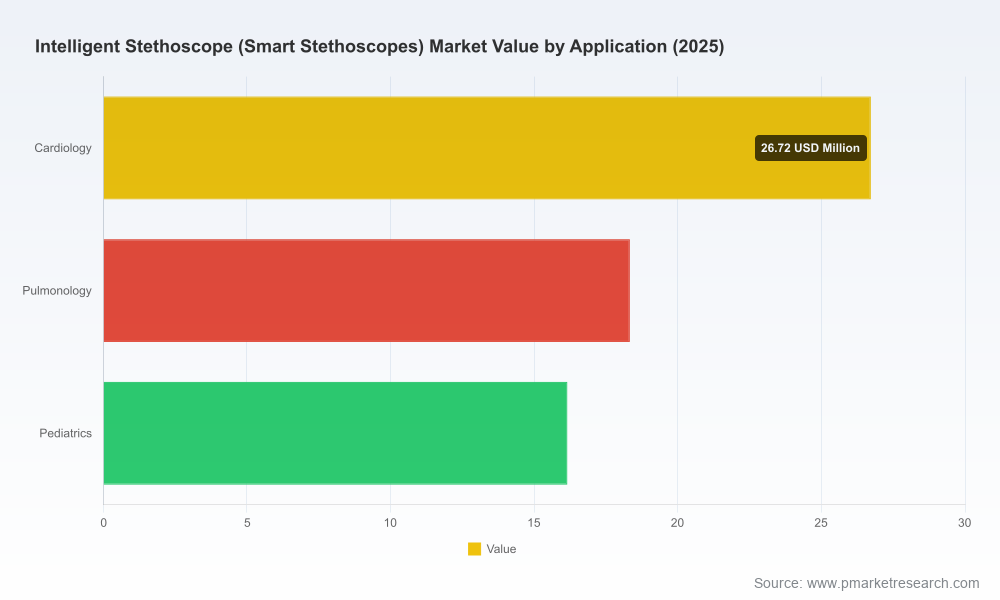

The intelligent (smart) stethoscope market has moved firmly from clinical curiosity to commercial contention. Measured on a consistent USD-million basis with 2025 as our base year, the market expanded from approximately 45.3 million in 2020 to 61.2 million in 2025. PW Consulting’s forward view projects continued growth into the forecast horizon (2026–2032), reaching roughly 99.0 million by 2032 at a compounded annual growth rate of 6.98% for the projection period. The 2026 estimated market midpoint sits above the 2025 base, signaling an inflection period where clinical validation, regulatory clarity, and reimbursement traction collectively drive enterprise-level investment decisions.

Intelligent Stethoscope (Smart Stethoscopes) Market

From pilot to procurement: Health systems and telehealth platforms that ran pilots in 2022–2024 face procurement and deployment choices in 2026. The market trajectory suggests a window for scale decisions before larger competitive consolidation accelerates.

Intelligent Stethoscope (Smart Stethoscopes) Market

Evidence as a moat: Clinical outcome data and real-world performance are now gating factors for adoption. Vendors that can demonstrate validated improvements in diagnostic yield or workflow efficiency will capture premium positions.

Intelligent Stethoscope (Smart Stethoscopes) Market

Regulatory and reimbursement timing drives ROI horizons. Clearance of AI modules and mapping to billable workflows are decisive variables for CFOs when modelling payback periods for device rollouts in 2026.

Partnering beats solo-play in the medium term. Interoperability with telehealth platforms and EMRs is the dominant operational requirement; vendors who secure platform partnerships can shortcut adoption friction.

Regulatory regime maturity: Digital stethoscopes and their AI modules are not one-off clearances. In major markets, 510(k) pathways and ongoing post-market surveillance remain necessary for US market access, while CE-mark pathways and national filings affect European deployment timelines. Organisations must budget for regulatory maintenance as an ongoing operating cost (sources: FDA, company releases).

Clinical validation is now demonstrable: Recent large-scale studies and NHS-led pilots have moved evidence from small cohorts into pragmatic clinical settings. Vendors with peer-reviewed performance—especially in cardiac murmur detection and pulmonary sound classification—gain preferential consideration from purchasing committees (Eko/NHS and academic collaborations, January–February 2026).

Telehealth integration is table stakes: AI-enabled auscultation is consistently being embedded in telehealth workflows that require real-time waveform display, clinician co-listen, and asynchronous review. Platform integration decisions—APIs, latency, security—shape which devices are operationally feasible for large health systems.

Reimbursement is evolving from anecdote to structure: Coding frameworks and telehealth-adjacent E/M guidance already include pathways for electronic stethoscope use with AI augmentation. Stakeholders who can align device use-cases with billable codes will materially accelerate adoption in ambulatory and remote settings.

Market concentration signals competitive structure: The market shows measurable concentration around a small number of established players; top vendors together account for a majority share, with the top-five consolidating an even larger portion of commercial revenue. This concentration has practical implications for pricing, channel access, and partnership dynamics.

Eko Health (San Francisco, CA): Eko’s CORE product family (CORE 500, CORE 300) combines digital auscultation, integrated 3‑lead ECG, real-time waveform visualization and AI-driven murmur detection. Recent clinical results—reported in early 2026—show materially improved detection rates for valvular heart disease in clinic settings and significant NHS-centered real-world evaluation activity. For buyers, Eko represents a strong clinical-evidence play with established telehealth integrations.

TytoCare (Herzliya, Israel): TytoCare’s Stethoscope is positioned as a core remote-exam asset within a broader kit, enhanced by an AI add-on for lung-sound identification. Regulatory progress (European clearance for the lung‑sound AI add-on in March 2026) and the 2025 launch of a Smart Clinic Companion—built on a large multimodal dataset—underscore TytoCare’s strategy: platform-plus-module, focused on primary care/remote clinic use-cases and rapid geographic expansion across CE-marked markets.

Thinklabs (Centennial, CO): Thinklabs One emphasizes high-fidelity amplification, Bluetooth transmission, and a clinician-focused sound library. Its value proposition centers on clinical-grade acoustics for bedside and telehealth scenarios; Thinklabs is commonly selected where sound fidelity and practical workflow integration are the procurement priorities.

3M / Littmann (St. Paul, MN): Littmann CORE’s hybrid analog/digital functionality, significant amplification and active noise cancellation place it as the incumbent bridge between traditional auscultation and AI-enabled workflows. 3M’s channel strength and brand trust make Littmann a default consideration for large-scale rollouts where vendor risk mitigation is prioritized.

Eko’s 2026 clinical publications and NHS collaborations accelerate buyer confidence in AI-enabled cardiac detection (Eko / Imperial College / NHS studies, Jan–Feb 2026).

TytoCare’s CE clearance for a lung-sound AI module (March 2026) and earlier launch of a Smart Clinic Companion (Oct 2025) signal a push to embed auscultation AI inside primary‑care workflow bundles.

Across vendors, expect increased investment in post-market surveillance and model-update governance to satisfy regulators and purchasing organizations.

Validated market sizing and scenario-based forecasts (base year 2025; historical 2020–2025; forward view 2026–2032) with sensitivity analyses for adoption velocity and reimbursement changes.

Regulatory pathway playbook: region-specific clearance dynamics, post-market surveillance requirements, and tactical timelines for AI module submissions.

Reimbursement and coding map: CPT/HCPCS alignment, telehealth billing pathways, and payer engagement templates for commercial and public payers.

Vendor competitive scorecards and go-to-market implications: technical strengths, clinical evidence, channel strategies, and partnership opportunities for device OEMs and digital health platforms.

Deployment playbooks for health systems: procurement evaluation checklists, integration roadmaps (telehealth + EMR), clinician onboarding outlines, and ROI calculators for phased rollouts.

Investor and M&A lens: thesis-ready due diligence frameworks, valuation sensitivity to clinical evidence strength, and a shortlist of attractive acquisition archetypes.

Device manufacturers: Prioritise peer-reviewed clinical trials and clear, reproducible performance claims. Invest in post-market evidence generation and partner with established telehealth platforms to shorten procurement cycles.

Digital-health platforms and EMR vendors: Establish certified integration pathways and co-commercial pilots with top clinical vendors. Offer bundled workflow modules to health systems that include documentation templates aligned with reimbursement codes.

Health systems: Move from point pilots to phased deployments tied to clinical KPIs (diagnostic yield, fewer referrals, telehealth visit completion rates). Insist on data portability and interpretability of AI outputs.

Investors and private equity: Focus on companies with verifiable clinical evidence, regulatory clearance traction, and defensible integration partnerships. Watch for consolidation opportunities where top vendors seek to round out portfolios with complementary sensor or analytics capabilities.

PWConsulting’s market synthesis for intelligent stethoscopes frames 2026 as a decision-rich year: evidence generation, regulatory clarity, and reimbursement alignment will determine which vendors scale and which become niche suppliers. The headline market growth and concentration trends provide a directional compass; the operational levers—trial design, regulatory sequencing, partnership architecture, and coding alignment—are the tactical levers that determine competitive outcomes.

Note on content scope: This article intentionally presents high-level market sizing, growth trajectory and competitive dynamics while withholding granular subsegment-level figures and proprietary scenario matrices (by region, application and device-type). PW Consulting reserves the detailed breakouts, segment-level forecasts and downloadable financial models for the full report. For clients and decision-makers seeking executable models, scorecards, and the complete set of subsegment analytics required to finalise 2026 budgets and product roadmaps, please visit PW Consulting’s Intelligent Stethoscope Market report page to request the full dataset and advisory engagement options.

For detailed analysis of this topic, please visit the official page:Intelligent Stethoscope (Smart Stethoscopes) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com