2026 Strategic Brief: Water Pump, Vacuum Pump and Turbocharger Market — PW Consulting Industry Insight

Executive summary

As companies finalize budgets and strategic priorities for 2026, capital allocation and product-roadmap decisions in the fluid- and air-handling space must be grounded in forward-looking market intelligence. PW Consulting’s new study, with a base year of 2025 and a historical series covering 2020–2025, projects the global Water Pump, Vacuum Pump and Turbocharger market through a 2026–2032 forecast window. The forecast embeds an aggregate compound annual growth rate (CAGR) of 6.98% across the period, delivering a clear directional signal: a mid-single-digit growth trajectory coupled with pockets of accelerated demand driven by electrification, emissions control programs and industrial vacuum requirements in high-tech manufacturing.

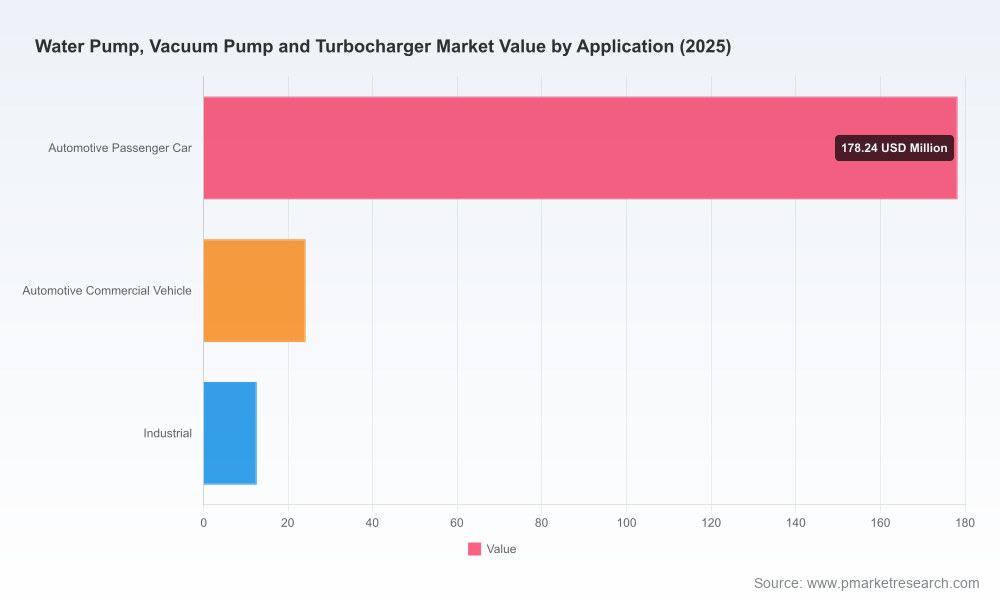

Water Pump, Vacuum Pump and Turbocharger Market

This brief highlights why the 2026 planning cycle should treat this study as a decision-grade input: it synthesizes market-scale dynamics, commercially actionable scenario analysis and supplier-by-supplier positioning—while deliberately reserving granular segment-level tables to drive engagement with the full report.

Water Pump, Vacuum Pump and Turbocharger Market

Why this matters for 2026 corporate decisions

- Capital allocation and capacity planning: The projected multi-year expansion requires firms to reassess factory footprints, ramp profiles and spare-parts inventories. Timing matters: lead times for specialized machining and turbocharger validation stretch across quarters, so investment decisions made in 2026 will influence product availability into 2028–2029.

- R&D and product roadmaps: Electrified water pumps and advanced turbocharging architectures (variable turbine geometry, electric assist, integrated thermal management) are moving from concept to series programs. OEM and Tier‑1 R&D portfolios need re-prioritization to capture fast-growing content per vehicle.

- Regulatory and service risk management: New HFC control measures and evolving reporting obligations that came into effect in 2025 alter servicing practices for refrigeration- and vacuum-related equipment. Compliance and reclamation capabilities are now operational imperatives, not future considerations.

- Portfolio and M&A strategy: The market concentration metrics show a fragmented competitive landscape—measured by low single‑digit CR3 and CR5 percentages—creating near-term opportunities for bolt-on acquisitions and capability consolidation focused on system integration rather than commoditized components.

Market dynamics shaping 2026–2032

The market’s mid‑to‑late‑cycle growth will be shaped by three intersecting forces:

Water Pump, Vacuum Pump and Turbocharger Market

- Electrification and thermal management: Electric water pumps are transitioning from optional to standard content in many architectures—covering engine cooling, battery/inverter thermal management and HVAC loop control. This raises the technical bar on electrical control systems, thermofluid optimization and supplier software stacks.

- Turbocharger evolution: Turbocharger demand is being driven by downsized turbocharged powertrains and hybridization. Variable turbine geometry and electrically assisted turbochargers are moving into production programs for both gasoline and diesel applications, increasing design complexity and validation burden.

- Vacuum demand from advanced manufacturing: High- and ultra-high vacuum equipment for semiconductor fabs, analytical instruments and R&D facilities is tightening the market for high-performance turbo and dry pumps. Clean, oil-free solutions and uptime guarantees are differentiators.

Overlaying these trends are regulatory inflection points: restrictions on higher‑GWP HFCs that began to take effect in 2025 and associated reporting obligations require equipment makers and service providers to reassess refrigerant handling, reclamation processes and documentation workflows—directly affecting aftermarket and service business models.

Competitive landscape — who matters and why

The competitive map features a mix of global diversified industrials, specialized pump manufacturers, and precision vacuum houses. PW Consulting’s analysis evaluates strategy, product positioning, manufacturing footprint, and program wins to help executives understand where to partner, compete or consolidate.

- BorgWarner (Irvine, CA): Aggressive turbocharger program wins for compact and light commercial vehicle platforms, including VGT and high-performance turbo programs, position them as a technology leader in powertrain forced‑induction solutions. Their work on thermal management (electric water pumps) complements turbo programs and creates systems-level opportunities for OEMs.

- Gorman-Rupp (Mansfield, OH): A stalwart in self‑priming and municipal wastewater pumps, Gorman‑Rupp’s strength is in rugged, serviceable units and aftermarket networks—an important factor for municipal and industrial users focused on lifecycle cost and uptime.

- Flowserve (Irving, TX): With a heavy presence in API and process pumps, Flowserve remains a go‑to for oil & gas, power and chemical sectors where industrial-grade centrifugal and process pumps dominate specifications.

- Gates Corporation (Denver, CO): Strong in automotive aftermarket and OE water pumps (including electric variants), Gates combines components and systems-level cooling expertise—an attractive partner for OEMs seeking integrated cooling subsystems.

- Aisin Seiki (Aichi, Japan): A leading OE supplier with mass-production capability for traditional and electric water pumps; their die‑cast and electric offerings are core to powertrain thermal strategies.

- Robert Bosch GmbH (Gerlingen, Germany): Bosch’s portfolio of electric water pumps, thermal management and turbocharger components makes them a cross-domain supplier to major OEMs, particularly in Europe.

- Edwards Vacuum (Crawley, UK), Pfeiffer Vacuum (Asslar, Germany), Atlas Copco (Nacka, Sweden): These firms dominate the high‑performance vacuum segment—serving semiconductors, analytical, and industrial processes—with differing focuses on turbo technology, dry screw solutions and service models.

PW Consulting’s competitor matrices identify not only product overlaps but also differentiated capabilities: software-enabled controls, validation capacity for electrically assisted turbochargers, aftermarket reach, and compliance-ready servicing for refrigerant‑related regulations. The study flags suppliers likely to be target acquisition candidates and those vulnerable to displacement due to capability gaps.

Recent developments shaping near-term opportunity

- Major turbocharger awards and program starts by established suppliers are accelerating production commitments into 2027–2028. These program wins underscore the need for Tier‑1s and OEMs to lock supply and validation calendars now.

- Capacity expansions in vacuum pump assembly and the introduction of more efficient dry vacuum designs point to intensifying competition in contamination‑sensitive end markets such as semiconductor and pharmaceutical manufacturing.

- Regulatory measures on HFCs that started in 2025 have already begun to change servicing and disposal practices—creating aftermarket compliance services and reclamation economics that incumbents and new entrants can monetize.

What the full PW Consulting report delivers (actionable modules)

The study is organized for operational use by strategy, product, procurement and M&A teams. Key deliverables:

- Proprietary market sizing and forecast model (2020–2032) with scenario toggles for slower/higher adoption paths and sensitivity to macro shocks.

- Supply‑chain and capacity maps, including critical supplier bottlenecks, lead‑time diagnostics and regional manufacturing exposure assessments.

- Competitor scorecards and playbooks for 20+ suppliers, with capability matrices, margin proxy analysis and M&A candidate shortlists.

- Regulatory impact toolkit detailing compliance pathways, cost-to-serve implications, and aftermarket service playbooks tied to recent HFC policy changes.

- Product roadmap templates and validation timelines for electrified water pumps, variable-geometry turbochargers and high-vacuum systems.

- Go‑to‑market and pricing levers for automotive OEMs, industrial buyers and service networks, including win/loss analytics and channel strategy guidance.

Strategic recommendations for 2026 planning

- Lock program qualification schedules: For companies targeting OEM turbocharger programs, establish cross-functional validation milestones that align with suppliers’ 2027–2028 series starts. Delays in test rigs, NVH sign‑off or emissions mapping will cascade into multi‑year revenue impacts.

- Prioritize electrified cooling IP: Invest in control‑software, thermal modeling and compact electric‑motor integration. Early pilots with battery and inverter cooling systems yield outsized learning benefits for broader HVAC and powertrain use cases.

- Harden aftermarket compliance offerings: Build or acquire refrigerant reclamation and compliant servicing capabilities to capture new service margins created by HFC restrictions and reporting obligations.

- Targeted M&A and partnerships: Use the fragmented concentration landscape to pursue bolt‑ons that add validation capacity, software control stacks or specialized vacuum competencies, rather than expensive horizontal roll‑ups.

- Scenario stress-testing: Run downside scenarios that assume supply-chain shocks or a slower automotive rebound—validate breakpoints in capacity utilization and working capital.

How to use the report in practice

PW Consulting’s deliverables are designed to be plug‑and‑play for board decks, investment memos and procurement playbooks. Use the model to run “what‑if” cases for electrification adoption, turbocharger mix shifts, and vacuum equipment demand from semiconductor fabs. Leverage supplier heatmaps for sourcing decisions and the regulatory toolkit to quantify compliance costs by product family.

Closing note — the value proposition

The Water Pump, Vacuum Pump and Turbocharger market is maturing into a systems‑level battleground where thermal management, emissions control and high‑vacuum performance intersect. Our study quantifies the addressable opportunity across 2026–2032 and converts market intelligence into executable initiatives for procurement, product and M&A teams. To preserve competitive advantage and avoid commoditization risk, executives should combine the study’s macro forecast and scenario engine with company‑specific diligence—available in the full report.

For executives preparing 2026 budgets, the PW Consulting study is not a static market snapshot but a decision-support platform: one that links growth projections, supplier behavior, regulatory change and technology trajectories to concrete action items. Accessing the full report is the fastest path to convert this directional insight into quantified, prioritized moves for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Water Pump, Vacuum Pump and Turbocharger Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com