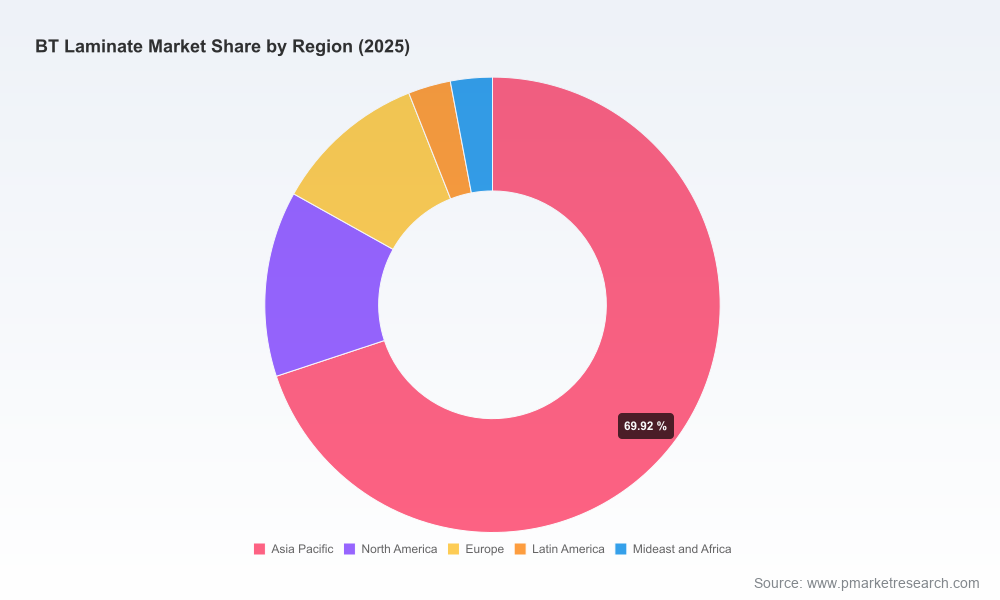

PW Consulting: BT Laminate Market to Reach USD 5,243.45 Million by 2032, Growing at a 7.25% CAGR

Other |

2026-07-02 05:04:13

As PW Consulting’s senior strategic advisory team, we present an executive preview of our comprehensive Isoprene Rubber (IR) market study — an intelligence package calibrated for boardrooms, strategy teams, and corporate development functions planning for 2026 and beyond. This preview synthesizes the macro trajectory, structural dynamics, competitor moves, and operational levers that matter most when allocating capital, designing sourcing strategies, or shaping product roadmaps in the IR value chain.

Isoprene Rubber (IR) Market

The global IR market is on a structurally positive path. Our analysis projects the market expanding at a compound annual growth rate (CAGR) of 6.98% from the 2025 base year through the forecast horizon, with total market value moving from approximately USD 215.0 Million in 2025 to roughly USD 344.8 Million by 2032. This trajectory is not uniform — it reflects the interplay of raw material cost cycles, standards-driven demand in medical segments, technology shifts toward bio-based variants, and targeted capacity investments by strategic players.

Isoprene Rubber (IR) Market

For decision-makers in 2026, these macro signals translate into actionable choices across four strategic dimensions:

Isoprene Rubber (IR) Market

Feedstock volatility — a leading margin driver. Isoprene monomer supply is predominantly derived from petroleum-based naphtha or natural gas liquids. Upstream price volatility — highlighted by notable increases in Q1 2026 — imposes short-to-medium-term cost pressure on polyisoprene producers. Firms that can secure advantaged feedstock, implement dynamic pricing mechanisms, or realize feedstock integration will enjoy a structural cost advantage.

Regulatory tailwinds in medical and healthcare. International standards (ISO 2303 and related updates through 2026) and regulatory guidance such as FDA recommendations favoring protein-free glove production have accelerated adoption of synthetic polyisoprene latex in medical applications. This has immediate implications for capacity planning and quality assurance investment for suppliers targeting the medical segment.

Sustainability and feedstock substitution. The commercial introduction of bio-based synthetic polyisoprene variants signals an inflection point: customers increasingly value life-cycle credentials and renewable feedstocks. Early movers that can credibly commercialize bio-based grades without sacrificing performance will capture premium placement in OEM and healthcare supply chains.

Concentration and competitive dynamics. The IR market remains relatively fragmented at the top: the three- and five-firm concentration ratios indicate significant market share dispersion. This fragmentation creates opportunities for M&A consolidation and for niche specialists to command premium pricing through differentiated capabilities.

The full PW Consulting IR research report is designed as a playbook for executives. It combines rigorous market-sizing with prescriptive tools to convert insight into action. Key deliverables include:

The IR supplier universe features a mix of global chemical majors, specialized elastomer producers, and vertically integrated tire makers. The market’s modest top-tier concentration creates fertile ground for strategic repositioning — particularly by players who combine technology differentiation with scale.

Kuraray Co., Ltd. — the recognized leader in liquid isoprene rubber (LIR) and high-value polyisoprene grades. Kuraray’s unique position in LIR provides it with differentiated applications in high-performance tires and medical devices. For buyers, Kuraray represents a premium supplier; for competitors, it is the benchmark for specialty-grade R&D.

Cariflex Pte. Ltd. — demonstrated aggressive capacity and scale expansion, including a major Jurong Island facility that materially increases global polyisoprene latex throughput. The scale-up should be monitored for downstream pricing implications and potential supply-demand rebalancing in medical latex markets.

Major chemical and polymer players (e.g., LyondellBasell, Shell, ExxonMobil, Sinopec) — these firms influence feedstock flows and can exert pricing pressure via integrated isoprene and elastomer production. Their strategic posture around feedstock integration and specialty grade investments will shape margins across the value chain.

Specialty elastomer producers (e.g., JSR Corporation, ZEON Corporation, Kraton) — focused on high-performance grades and innovation. ZEON’s launch of a bio-based synthetic polyisoprene variant is an early signal that R&D-driven differentiation can disrupt procurement priorities for OEMs with sustainability mandates.

Tire manufacturers and integrators (e.g., Goodyear and others) — recent divestitures and acquisitions within polymer chemicals businesses underscore strategic tradeoffs between vertical integration and capital allocation. The 2025 transactions involving Goodyear’s polymer chemicals business illustrate how portfolio reshaping can affect supply security and technology ownership.

Procurement & Sourcing: Implement dynamic feedstock tracking and multi-supplier tendering. Where possible, secure medium-term contracts with indexed pricing and optionality clauses that align supplier economics with raw material cycles.

Investment & Capacity: Defer or accelerate greenfield expansions based on scenario analysis that weighs feedstock price paths, medical-grade demand curves, and adoption rates for bio-based grades. Consider brownfield upgrades to capture yield improvements faster than greenfield timelines.

Product Strategy: Differentiate through certified bio-based and premium medical-grade offerings. Invest in test-and-certification pathways early to capitalize on regulatory tailwinds and secure OEM qualification windows.

M&A & Partnerships: Target bolt-on acquisitions that fill technological gaps (e.g., LIR capability, clean-room manufacturing for medical grades) or provide access to critical logistics corridors. JV structures may be preferable where feedstock access or regulatory approvals create entry frictions.

Risk & Resilience: Build inventory and working-capital buffers calibrated to upstream volatility, and stress-test scenarios that combine feedstock shocks with regional demand shifts. Strengthen supplier audits and dual-sourcing arrangements for critical intermediates.

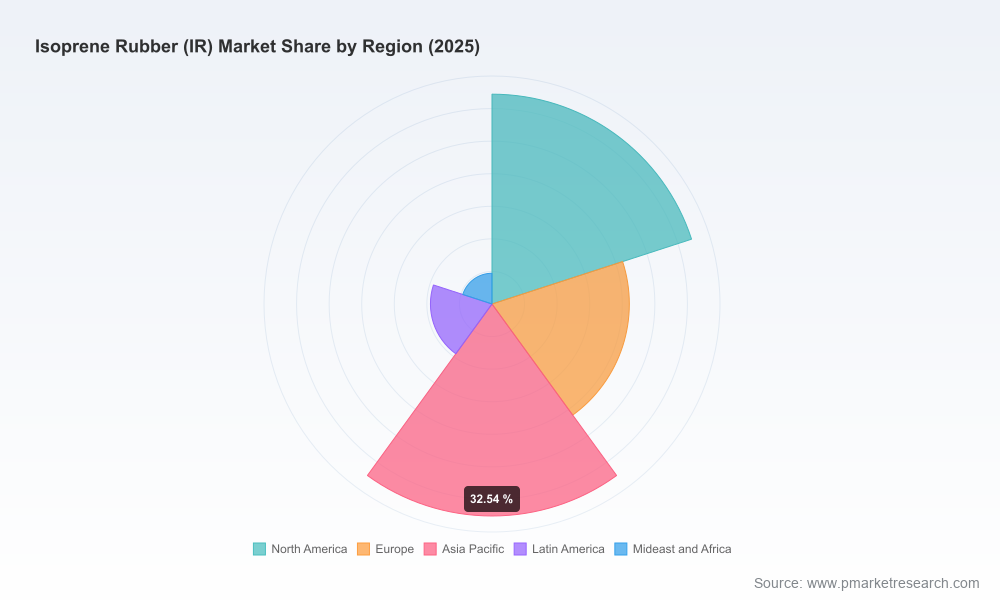

In keeping with the “trailer” principle of this preview, we are intentionally not disclosing granular segmentation tables (region-by-region or application-specific percentage shares and detailed revenue splits) within this briefing. Those detailed segmentations and the underlying datasets — which include granular regional demand drivers, application-by-application forecasts, supplier-level production volumes, and modelled pricing paths — are included in the full PW Consulting IR market report available via our platform.

This selective disclosure is purposeful: it ensures that stakeholders who require transaction-grade intelligence — procurement teams issuing RFPs, M&A teams performing target diligence, and strategy units modelling multi-scenario investments — receive full methodological transparency and the data extracts necessary to run bespoke analyses.

Custom scenario modeling: We translate the report’s baseline and alternative scenarios into company-specific financial impacts — aiding capital allocation and price passage decisions.

Supplier diligence: Deep dives on target suppliers, including technology audits, site-level risk assessment, and integration planning support for transactions.

Regulatory compliance roadmaps: Operational recommendations to meet evolving ISO and FDA requirements for medical-grade synthetic latex and elastomers.

Conclusion — As IR demand accelerates and the supply base evolves through capacity projects, product innovation, and selective consolidation, 2026 is a pivotal planning year. The market’s projected growth path to 2032 creates both opportunity and complexity. The PW Consulting IR study arms leaders with the scenarios, the financial levers, and the competitive maps needed to turn uncertainty into strategic advantage. For the complete dataset, granular segment views, and the full suite of actionable tools, visit the PW Consulting report landing page and request the full report and model pack.

For detailed analysis of this topic, please visit the official page:Isoprene Rubber (IR) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com