Flue & Chimney Pipes Market — Strategic Imperatives for 2026 Decision‑Makers

As PW Consulting’s lead industry analyst, I present a focused introduction to our Flue & Chimney Pipes Market study — a tactical briefing designed to convert macro market dynamics into boardroom-ready actions for 2026. This market is no longer niche engineering; it sits at the intersection of decarbonisation policy, building safety regulation, and modular construction economics. Our analysis synthesises historical performance, forward projections, regulatory headwinds, material supply risk and competitive intent so executives can prioritise capital, M&A, and go‑to‑market moves with conviction.

Flue & Chimney Pipes Market

Why this market matters in 2026

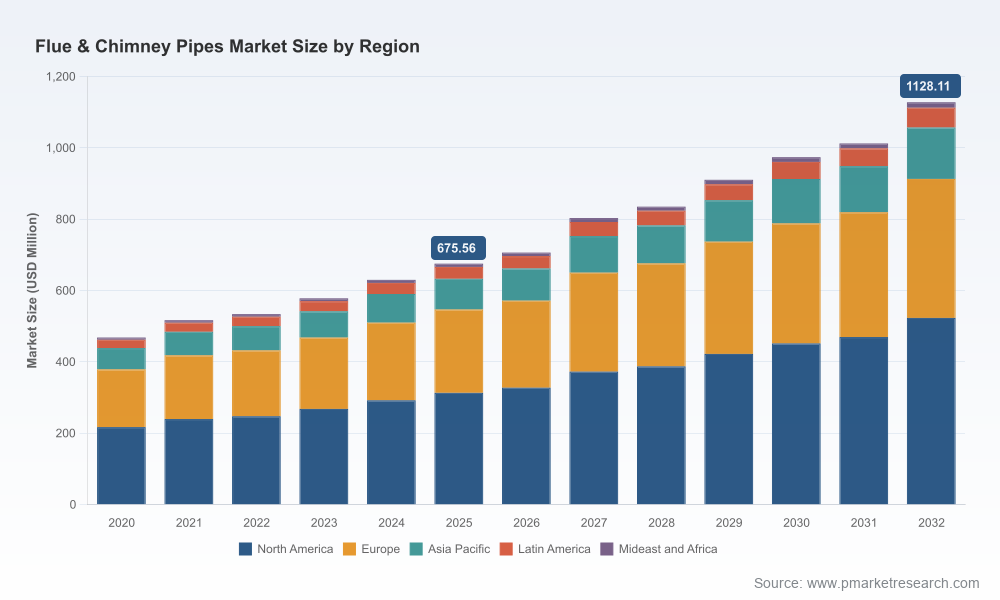

- The flue & chimney pipes market has demonstrated steady recovery and expansion through the first half of the decade, growing from mid‑hundreds of millions in annual revenue in 2020 to a stronger base in 2025 (USD 675.56 Million). This momentum sets the stage for accelerated growth across the forecast horizon.

- From 2026 through 2032 the market is projected to expand at a compound annual growth rate (CAGR) of 7.6%, reaching north of USD 1.1 billion by 2032. That growth is concentrated where regulation, retrofit demand and product innovation intersect — creating distinct value pools for targeted players.

- Market concentration remains moderate: the top three players account for under one‑third of the market and the top five just over one‑third. This structure favours both consolidation plays and differentiated niche strategies.

What the PW Consulting report delivers (practical contents)

Our study is intentionally action‑oriented. It combines desk research with supplier interviews and primary installer consultations to provide:

Flue & Chimney Pipes Market

- Validated market sizing and a transparent methodology for reproducing scenario runs under alternative energy and regulatory paths.

- Supply‑chain heat maps identifying single‑source exposures (notably high‑grade stainless steel) and tier‑1 supplier risk profiles.

- Regulatory compliance matrices — mapped to key markets — that translate standards (e.g., EN/BS series and CE requirements) into direct product design and testing implications.

- Go‑to‑market playbooks for OEMs, distributors and pure‑play installers: channel economics, margin waterfalls, service‑extension opportunities and digital enablement use cases.

- Pricing and margin sensitivity models tied to primary input costs and labour availability — useful for short‑term hedging and longer‑term contract strategy.

- A shortlist of M&A targets and partnership archetypes, with screening criteria aligned to strategic objectives (capacity, certification, channel access, IP).

- Operational blueprints for modular prefabrication, lean fabrication lines and quality assurance protocols that reduce installation risk and warranty exposure.

Regulatory and material dynamics — the levers that will move the market

- Standards and conformity: Metal chimneys and flue liners are governed by established European and national standards (BS EN series and CE marking obligations in key jurisdictions). Compliance is non‑negotiable; investments in certified testing, traceability and installer training pay off as market access enablers.

- Raw material pressure: Premium products increasingly rely on stainless steel 316L (and equivalent grades). The broader stainless market — valued in the multi‑billion dollar range globally — drives both cost and availability. Hedging strategies, diversified sourcing and material‑efficient design are immediate priorities.

- Installer competency: Safety and performance checkpoints mean certified installers (HETAS or equivalent) control conversion rates in retrofit markets. Labour shortages and certification bottlenecks shape where growth converts to revenue.

- Decarbonisation ripple: Building electrification and hybrid heating strategies are reshaping appliance mixes. Where combustion persists (solid fuels, biomass, gas in transitional scenarios), demand for reliable, compliant flue systems remains high — but product specs are evolving to handle lower‑temperature flue gases and corrosion vectors.

Competitive landscape — strategic positions and implications

The sector features a mix of specialised European manufacturers, large North American suppliers with UL credentials, and regional components specialists. Below I outline competitive archetypes and the strategic conclusions we draw from our company intelligence.

Flue & Chimney Pipes Market

- European premium specialists (e.g., Schiedel, Poujoulat, Meniflex): Deep expertise in stainless and ceramic systems, strong engineering heritage and EU certification credibility. Their strength: product innovation and brand trust in residential and commercial applications. Strategic implication: continue investing in material science and modular systems; pursue selective aftermarket services to capture higher lifetime value.

- UK regional manufacturers and systems players (e.g., SFL Flues & Chimneys, Rhino Flues, Brewer Metalcraft): Close installer networks, broad accessory portfolios and event‑driven marketing (notably regional exhibitions and installer forums). Strategic implication: leverage local presence to offer bundled installation packages and certification training to protect margin from commoditisation.

- North American systems and listings specialists (e.g., DuraVent, Rockford Chimney Supply): UL‑listed systems, emphasis on insulated double‑wall solutions and flexible liner supply. Strategic implication: use standards compliance and labelling as differentiation in export markets and in segments where warranty and insurance interactions matter.

- Mechanical ventilation and extraction specialists (e.g., Exodraft): Cross‑sell opportunities arise when combining draft control, fans and flue systems into integrated solutions for commercial and industrial customers. Strategic implication: pursue systems sales and OEM integration agreements with appliance manufacturers.

Notable recent activity: SFL Flues & Chimneys is publicly set to exhibit at The Trade Stove & Fireplace Professional Show (May 2026). Such events continue to be valuable conduits for installer recruitment, specification debates, and local market intelligence.

Strategic plays that will differentiate winners in 2026

Our analysis identifies three winning pathways depending on your starting position and capital appetite.

- Operational excellence and scale (for incumbents): Invest in modular prefabrication lines, lean assembly and traceability systems to reduce installation time and warranty claims. Use concentrated market share (CR3/CR5 context) to negotiate upstream material contracts and pursue bolt‑on acquisitions to fill capacity or geographic gaps.

- Product and materials innovation (for premium niche players): Differentiate on corrosion‑resistant alloys, low‑temperature tolerant seals and integrated sensors for draft and blockage detection. Patentable coatings and testing protocols create defensible margins.

- Channel and service extension (for distributors/retailers): Bundle certified installation, maintenance subscriptions and remote diagnostics. Train and certify installer networks to create demand capture advantages in retrofit volumes.

Risk matrix — what to monitor in quarterly reviews

- Raw material price shocks (stainless grades) and lead‑time volatility.

- Regulatory amendments to building codes or labelling regimes that impose additional testing/traceability costs.

- Installer capacity constraints and the pace of certification uptake among local trades.

- Competitive pricing pressure if low‑cost imports or alternate materials encroach on mainstream applications.

Execution checklist for 2026 planning cycles

- Run sensitivity scenarios across three inputs: steel pricing, installer availability, and retrofit conversion rates. Embed results into capital allocation decisions.

- Secure at least 12–18 months of critical stainless supply via contracts or strategic stockpiles for premium product lines.

- Accelerate certification pipelines (EN/BS testing, UL where relevant) for any product aimed at new geographies.

- Deploy a channel upgrade program: certified installer tiers, digital lead routing and performance‑linked incentives.

- Target 1–2 strategic acquisitions or JVs that provide either manufacturing scale or access to a certified distribution network within 12 months.

How PW Consulting can accelerate your 2026 decisions

The full PW Consulting Flue & Chimney Pipes Market report contains the granular datasets, regional and application splits, price‑band analysis, and supplier scorecards you need to operationalise these recommendations. In keeping with our “trailer” principle, this introduction highlights the core strategic takeaways while reserving detailed segment tables, company share models and M&A candidate dossiers for the full report — the precise tools your deal teams and commercial leaders will use to execute.

For executives preparing budgets, supply contracts or acquisition screens in 2026, the report provides ready‑to‑use models and an implementation roadmap that turn a 7.6% CAGR projection and a growing revenue base into actionable investment and market‑entry decisions.

Next steps

- Request the full dataset and scenario models to run your internal stress tests.

- Book a strategy workshop with PW Consulting to map a tailored 12‑month roadmap — from procurement hedging to channel roll‑out and M&A screening.

- Engage our competitive monitoring package to receive monthly alerts on certification changes, material cost shifts and peer activity (including trade show and product launch intelligence).

PW Consulting’s in‑depth study gives you the market context, the risk controls and the competitive playbook needed to convert 2026’s uncertainty into decisive advantage. For the proprietary regional and application breakdowns, case studies and company scorecards referenced above, please consult the full report.

For detailed analysis of this topic, please visit the official page:Flue & Chimney Pipes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com