Neurological Biomarkers Market — Strategic Outlook for 2026 Decision‑Making

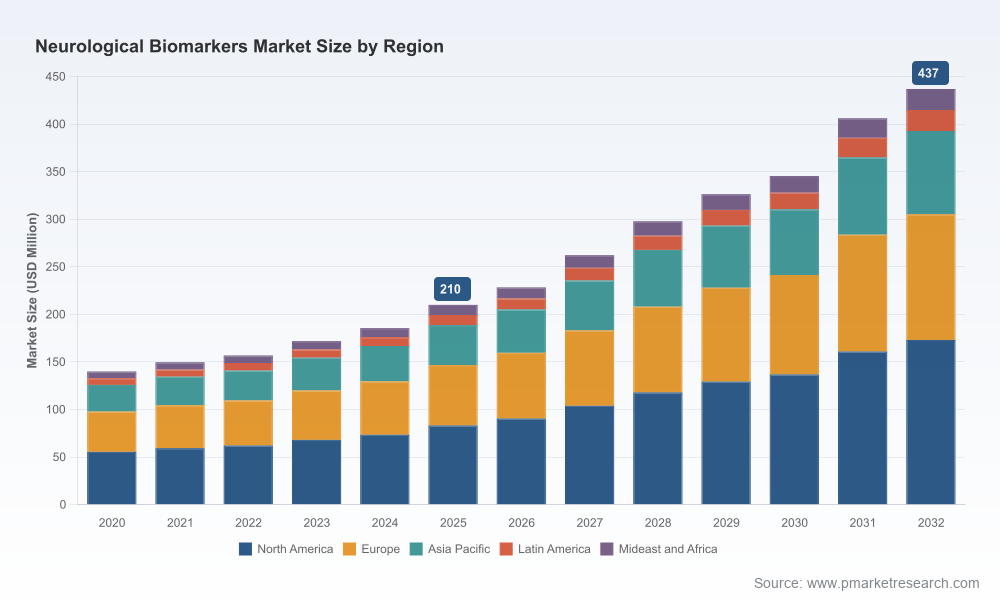

As neurological disease diagnostics and monitoring transition from niche research tools to mainstream clinical practice, executive teams face a critical strategic inflection in 2026. PW Consulting’s Neurological Biomarkers Market study (base year 2025; forecast 2026–2032) synthesizes macro growth, regulatory momentum, platform and reagent economics, and competitive behavior into an actionable blueprint for commercial and corporate strategy. The market has expanded rapidly — from roughly USD 140 million in 2020 to about USD 210 million in 2025 — and our forecast sees this trajectory continuing to approximately USD 437 million by 2032 at a compound annual growth rate (CAGR) of 11.2%. For leaders evaluating product launches, M&A, reimbursement strategy, or capacity investments, the timing and precision of decisions in 2026 will materially affect market position through the next cycle.

Neurological Biomarkers Market

Why this research matters for 2026

- Actionable timing intelligence: The market’s double‑digit CAGR conceals discrete windows when regulatory clearances, payer coverage decisions, and platform scaling converge — our study identifies those windows so you can align clinical validation and commercialization timelines.

- Regulatory and reimbursement playbook: The difference between a product that reaches routine clinical use and one that stalls is increasingly non‑technical — it is evidence design and payer engagement. The report maps IVDR and FDA dynamics and offers a prioritized set of evidence endpoints.

- Risk‑calibrated investment guidance: Our scenario modelling quantifies downside exposure from validation failures, supply‑chain constraints for immunoassay reagents, and delayed reimbursement, enabling risk‑adjusted capital allocation.

- Competitive positioning matrix: Rather than raw feature lists, we provide position maps that show where strategic partnerships, licensing, or bolt‑on acquisitions are higher return than organic development.

Market trajectory and inflection points

Historical growth (2020–2025) shows steady adoption as assay sensitivity and clinical utility matured: the market roughly grew from USD 140M to USD 210M in five years. Technology drivers include ultra‑sensitive immunoassays, high‑resolution mass spectrometry, and multiplexed proteomic panels — enabling blood‑based detection of neuronal injury and disease‑specific signatures previously accessible only via cerebrospinal fluid or advanced imaging. Regulatory milestones in 2024–2026 — including multiple 510(k)/CE‑IVD clearances and national certifications for blood‑based amyloid/p‑tau and NfL assays — have accelerated clinical integration, while early payer coverage decisions for select assays are beginning to translate clinical adoption into volume.

Neurological Biomarkers Market

Yet the path is non‑linear. The same regulatory frameworks that authenticate clinical utility also raise the bar for validation. European IVDR requirements and the FDA Biomarker Qualification Program impose extensive analytical and clinical validation burdens; delays or gaps in these programs create timing risk for commercialization. Additionally, raw reagent and biologics development costs remain elevated and are a recurrent constraint on rapid assay roll‑out.

Neurological Biomarkers Market

Competitive structure — what the landscape looks like in 2026

The neurological biomarkers market is moderately concentrated: the top three firms hold a majority share and the top five increase concentration further. This configuration produces a dual dynamic: established platform vendors control scale and distribution, while specialist diagnostics companies and mass‑spec innovators capture incremental clinical niches through focused R&D and strategic lab partnerships.

- Platform incumbents (large diagnostics and instrument providers) continue to leverage installed base economics. These firms emphasize validated assays for NfL, p‑tau isoforms, GFAP, and amyloid metrics and use regulatory clearances to drive uptake among hospital labs and reference networks.

- Ultra‑sensitive innovators (single‑molecule detection and specialized mass spectrometry providers) remain critical for assay sensitivity and early detection use cases. Their technology leadership creates premium niches, but scale and reimbursement remain gating factors to broader adoption.

- Clinical test specialists (commercial labs and focused diagnostics companies) convert technological advances into commercial tests with direct provider outreach, often leading in clinical workflows for acute care or memory clinics.

Recent notable developments underscore these dynamics: multiple approvals and clearances in 2025–2026 for blood‑based p‑tau and NfL assays have shifted the competitive calculus from “can we measure?” to “how quickly and at what cost can we deploy?” For market participants this means reallocating investments from discovery to scalable manufacturing, regulatory affairs, and payer evidence generation.

Strategic implications by stakeholder

- Diagnostics manufacturers: Prioritize platform interoperability and modular assay design. Focus on headroom where analytical performance differentiates clinical utility, but pair that with a reimbursement dossier prepared for payers at launch.

- Pharmaceutical companies: Leverage validated blood biomarkers to derisk trials, enrich cohorts, and create post‑approval monitoring programs. Engage early with platform vendors to secure kit supply and standardized assay runs.

- Clinical laboratories and reference networks: Invest in workflow automation and high‑throughput validation. Offer consultative services around assay interpretation to capture downstream value beyond the raw test.

- Payers and HTA bodies: Use real‑world evidence frameworks to evaluate long‑term cost offsets from earlier diagnosis and better disease management; selectively cover assays with clear clinical utility and guideline inclusion.

- Investors and private equity: Screen assets for regulatory maturity and payer engagement rather than headline sensitivity claims. Consider platform adjacency and distribution partnerships as primary value multipliers.

Key operational risks and mitigation strategies

- Validation burdens: IVDR and biomarker qualification timelines create launch uncertainty. Mitigation: stage evidence generation and use adaptive designs that allow incremental regulatory submissions.

- Reagent supply and COGS pressure: High immunoassay reagent costs can compress margins. Mitigation: diversify suppliers, invest in reagent optimization, and explore contract manufacturing partnerships.

- Payer fragmentation: Uneven coverage will produce uneven geographic uptake. Mitigation: prioritize early payer pilots and build value dossiers demonstrating clinical and economic impact.

- Competitive crowding: Rapid approval of similar assays risks commoditization. Mitigation: protect clinical differentiation via proprietary algorithms, longitudinal performance data, and integrated reporting services.

What PW Consulting’s report delivers — the practical toolkit

Designed for leaders who must act in 2026, the study blends quantitative forecasting with practical playbooks. Key deliverables include:

- Top‑line market model (base year 2025; forecast 2026–2032) with sensitivity and scenario runs that translate macro CAGR into revenue and investment milestones at company level.

- Regulatory pathway mapping across FDA and EU IVDR regimes, with recommended evidence packages and staged submission timelines tailored to assay type and indication.

- Payer engagement and reimbursement playbook outlining the evidence hierarchy, HTA milestones, and template economic models for negotiation with public and commercial payers.

- Technology and platform benchmarking that ranks vendors by analytical performance, throughput, cost per test, and scalability — linked to recommended commercialization routes (licensing, co‑development, or go‑it‑alone).

- M&A and partnership prioritization matrix that highlights targets likely to accelerate market entry or expand addressable use cases, and a short‑list of diligence KPIs for rapid screening.

- Clinical adoption guides and lab deployment checklists that convert validation data into operational readiness for hospital and reference labs.

To preserve commercial value and encourage direct engagement, the report deliberately omits granular public dissemination of region‑by‑region, type‑by‑type, and application‑by‑application split tables in this executive overview. Those segment breakouts, growth drivers by cohort, and proprietary pricing models are available in full on the report portal.

Immediate decisions for 90‑day and 12‑month horizons

- 90‑day actions: Complete an evidence gap analysis against the recommended regulatory dossier; initiate payer advisory boards; secure supply agreements for critical reagents.

- 6–12 month focus: Execute staged regulatory submissions; close strategic distribution or lab partnerships; pilot reimbursement claims with early adopters.

- KPIs to track: analytical validation milestones, payer coverage decisions, lab network integrations, cost of goods improvements, and ordering velocity from pilot sites.

Final perspective — why speed and discipline matter in 2026

The neurological biomarkers market is no longer purely a scientific frontier; it is a growing economic opportunity with defined rules of engagement. The market’s expansion from the low‑hundreds of millions in 2025 toward a substantially larger opportunity by 2032 at an 11.2% CAGR creates both runway and competition. For companies that synchronize regulatory execution, payer evidence, and scalable manufacturing, the rewards will be sustainable. For those that delay, the window for meaningful differentiation will narrow as platform incumbents and well‑capitalized specialists consolidate distribution and clinical recommender status.

PW Consulting’s Neurological Biomarkers Market study is engineered to convert this macro outlook into executable choices in 2026. For access to the full segment tables, competitive scorecards, and the proprietary model that underpins our forecasts, visit our report page or contact PW Consulting’s strategy team to schedule a targeted briefing and scenario workshop.

For detailed analysis of this topic, please visit the official page:Neurological Biomarkers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com