Laser Hair Removal in Dubai: Flawless Skin Techniques

Health |

2026-06-24 06:59:09

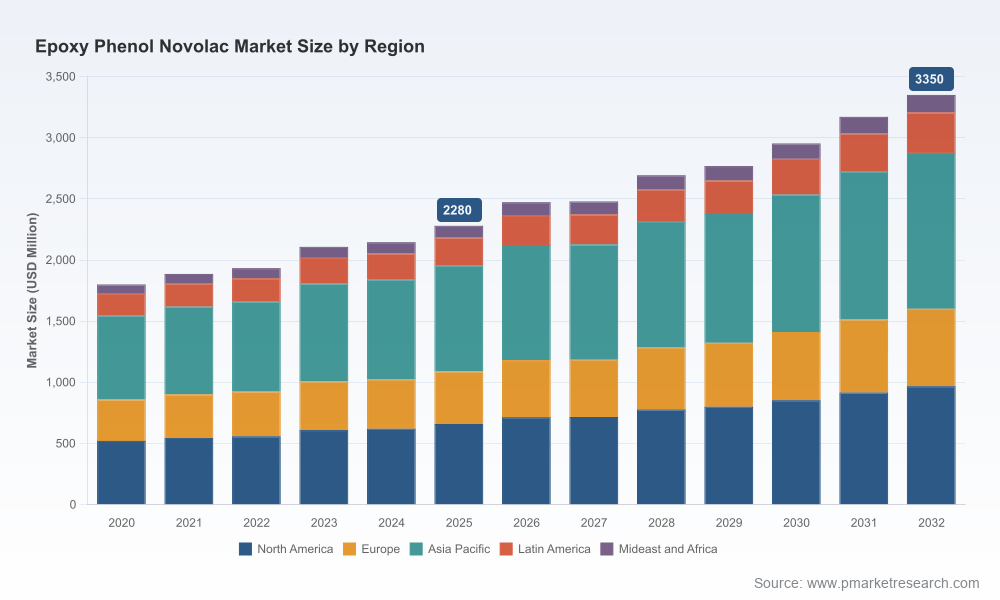

As PW Consulting’s lead industry analyst, I present a forward-looking synopsis of the Epoxy Phenol Novolac market designed specifically to inform executive choices in 2026. Our independent base-year benchmarking (2025) places the global market at approximately USD 2,280 million and the modelled outlook grows to an estimated USD 3,350 million by 2032, representing a compound annual growth rate (CAGR) of ~5.8% over the forecast horizon. These headline figures reflect structural demand from adhesives, coatings, composites and a suite of niche high-performance applications, tempered by feedstock volatility, regulatory shifts and evolving trade patterns.

Epoxy Phenol Novolac Market

Timing: 2026 is a pivot year. Companies that re-align sourcing, pricing and product strategies now will be better positioned to capture the mid-cycle recovery and premium demand projected through 2032.

Epoxy Phenol Novolac Market

Risk crystallization: Raw material and regulatory risks that were latent in 2024–2025 have become actionable business risks—affecting margins, contractual terms and capital allocation. Our research translates these risks into actionable scenarios for near-term decisions.

Epoxy Phenol Novolac Market

Capital efficiency: With moderate but steady market expansion at ~5.8% CAGR, capital deployed into capacity, R&D or M&A must be precisely targeted to high-return niches. The report provides the decision-grade prioritization matrix executives need.

PW Consulting’s full study goes beyond high-level estimates to deliver operationally relevant outputs that directly support corporate planning and commercial execution. Highlights include:

Market sizing and validated demand drivers (historic 2020–2025 and forecast 2026–2032) using a blended bottom-up/top-down methodology and >40 primary interviews across producers, formulators and end-users.

Feedstock cost-sensitivity models that quantify margin impacts across plausible price bands for phenol, formaldehyde and methanol derivatives, including break-even scenarios for liquid vs. solid product formats.

Regulatory impact frameworks mapping emissions and chemical compliance trajectories (regional and multilateral), with decision trees for formulation substitution, claim verification and supply continuity.

Commercial playbooks: go-to-market playbooks for producers (premiumization, contract re-design, flexible tolling) and for downstream buyers (hedging, dual-sourcing, specification negotiation).

M&A and capex roadmaps: prioritized target archetypes, valuation multiples observed in recent related transactions, integration risk checklists and an execution timeline to maximize post-deal synergies.

Technology and product roadmaps covering resins, modifiers and curing chemistries—identifying where incremental R&D spend delivers disproportionate performance uplift and price realization.

Three dynamics deserve special attention by 2026 planners:

Feedstock volatility: Phenol and formaldehyde price swings—exacerbated by geopolitics and methanol supply disruptions—have already squeezed resin manufacturers’ margins. Our models show that even moderate, sustained spikes materially alter producer operating leverage and incentivize dual-feedstock strategies and tolling arrangements.

Regulatory acceleration: Tighter emissions and low-formaldehyde mandates are changing formulation windows across major markets. Manufacturers who pre-emptively reformulate or secure validated compliant claims will gain privileged access to tier-one OEM specifications and long-term supply agreements.

Trade and substitution effects: Trade policy shifts, including tariffs affecting epoxy imports, have stimulated substitution and re-shoring dynamics. For some end-use segments, phenolic-based novolacs are emerging as preferred alternatives where supply security and regulatory compliance outweigh unit price competition.

The market balances established incumbents with regional specialists. The competitive environment is characterized by product breadth (liquid vs. solid grades), technical service capabilities and control of critical feedstock or processing know-how. Key strategic behaviors we observe among market leaders include premium product lines for high-temperature applications, targeted capacity investments in strategic regions, and selective price actions to manage inventory and margin.

DIC Corporation (Tokyo) — DIC’s portfolio includes both liquid and solid novolac grades optimized for high heat and chemical resistance. Their recent commercial move to revise epoxy resin pricing underscores a broader industry recalibration to input-cost pressure; suppliers that aggressively manage pricing levers are shaping short-term margin distribution and contractual renegotiations.

Olin Corporation (Stamford, CT) — Olin’s D.E.N. series, with multifunctional resins engineered for demanding coatings and composites, exemplifies the premiumization path. Olin’s strength is brand recognition in performance segments and established technical partnerships with formulators.

Kukdo Chemical (Seoul) — Kukdo competes on high-insulation and heat-resistant grades for protective coatings. Regional specialty players are leveraging proximity and application know-how to win specification-driven business, especially where logistical resilience is a decision criterion.

Nan Ya Plastics (Taipei) — Nan Ya brings integrated polymer capabilities and a route-to-market advantage in Asia-Pacific performance applications. Their focus on application engineering positions them well where system-level performance trumps commodity pricing.

Emerald Performance Materials (Cincinnati) — Emerald’s resorcinol-modified phenol novolac products target maximum chemical resistance and cross-link density. Such differentiated chemistries create defensible premium positions with specialty formulators and industrial OEMs.

Price adjustments by major suppliers in early 2026 indicate that cost pass-through mechanisms are being exercised more frequently. Buyers need updated sourcing clauses and indexation mechanics; sellers must refine customer segmentation to avoid disproportionate churn.

Geopolitical events in 2025 drove formaldehyde and methanol supply disruptions in certain regions, causing sharp short-term cost spikes. Manufacturers with flexible feedstock pathways and contractual tolling options have shown superior margin resilience.

Regulatory tightening—particularly on emissions—has accelerated the adoption of low/formaldehyde formulations. This creates a two-track market: compliant premium products and legacy formulations facing progressive displacement.

Based on our analysis, companies should pursue a coordinated set of moves in 2026 to balance growth and resilience:

Operational resilience: Implement feedstock hedging combined with regional dual-sourcing. Establish tolling agreements to flex capacity without committing large incremental capex.

Product and pricing segmentation: Differentiate between system-critical, high-value applications and large-volume commodity segments. Price-to-value rather than cost-plus in premium niches; apply contractual protection (minimum purchase obligations, indexation) for commodity accounts.

Regulatory-first innovation: Accelerate R&D for low-emission and low-formaldehyde resin options. Secure third-party verification where possible to pre-empt compliance-driven requalification cycles for customers.

M&A and partnerships: Target technology bolt-ons and regional players that offer application engineering capabilities or local market access. Prioritize targets with validated customer contracts to reduce integration risk.

Commercial excellence: Strengthen technical sales and specification support teams; invest in digital tools for demand sensing and contract analytics to better capture margin opportunities and reduce rebate leakage.

The full PW Consulting study translates the high-level market trajectory into executable plans: audited demand curves, supplier scorecards, detailed capex-impact simulations, scenario-based margin maps, and a prioritized set of near-term initiatives that CEOs, commercial heads and CFOs can activate within 90–180 days. Importantly, the report preserves proprietary segment-level analytics and granular region/application breakdowns to ensure strategic exclusivity for subscribers.

Portfolio prioritization: Use the CAGR-backed outlook and segment scenarios to re-weight investment portfolios—allocating R&D and capex to insulated growth pockets while pruning low-return lines.

Contract and pricing renegotiations: Present quantified feedstock exposure and benchmark positioning as the basis for updated contract terms in 2026 renewals.

M&A timing: Leverage the market’s steady mid-single-digit CAGR to pursue acquisitions at disciplined valuations, using our scenario stress-tests to set integration and payback targets.

Regulatory compliance strategy: Treat compliant formulations as a revenue-protection mechanism; prioritize certification and documentation efforts to avoid displacement risk.

The Epoxy Phenol Novolac market offers measured growth and durable applications-driven demand, but its near-term trajectory is governed by a set of manageable yet material risks—feedstock price cycles, regulatory realignments and trade-policy shifts. In 2026, the companies that combine disciplined commercial segmentation, proactive regulatory adaptation and nimble supply-chain strategies will transform these risks into competitive advantage. PW Consulting’s full study provides the granular, decision-ready intelligence required to make those calls with confidence.

For access to the comprehensive dataset, proprietary segment analysis and the tactical playbooks referenced in this preview, please consult the full report. PW Consulting clients receive tailored briefings and scenario workshops to align these insights with their 2026 operating plans.

For detailed analysis of this topic, please visit the official page:Epoxy Phenol Novolac Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com