Les Meilleures Plages pour un Casino en Ligne de Qualité

Other |

2026-06-19 12:18:26

As corporations and investors prepare capital allocation and sourcing strategies for 2026, the cyclohexene market offers a nuanced pathway: modest but consistent growth, pockets of specialty demand, and a supply base that is concentrated enough to influence margins yet fragmented enough to permit tactical sourcing wins. Our PW Consulting market study (base year 2025, historical analysis 2020–2025, forecast 2026–2032) synthesizes quantitative trend lines with actionable playbooks — intentionally presented here as a capability demonstration and strategic teaser. The complete intelligence — including granular segmentation, supplier scorecards, and scenario-modeled financial impacts — is reserved for the full report and client portals.

Cyclohexene (CAS 110-83-8) Market

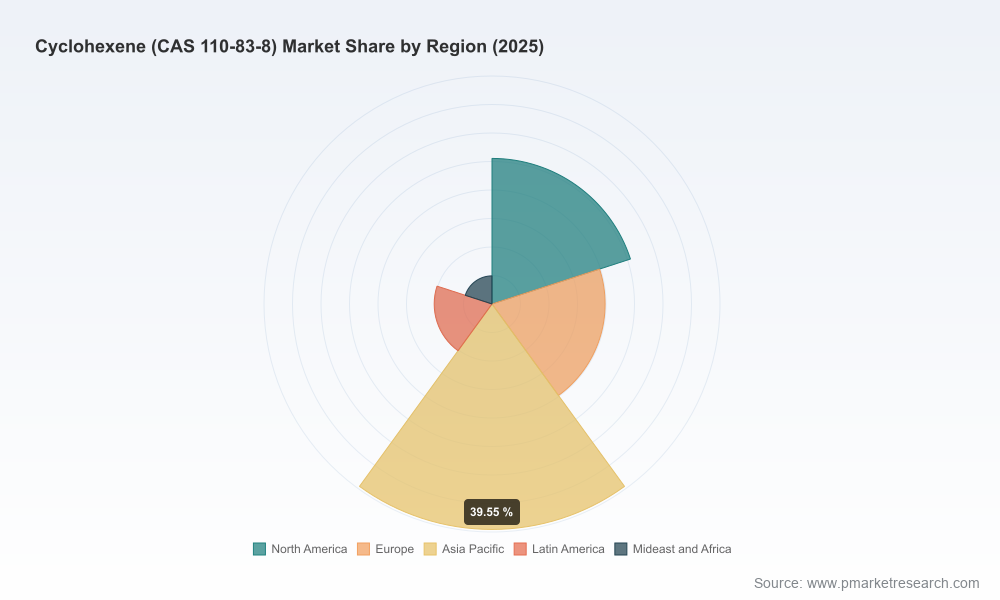

Market trajectory: The global cyclohexene market, measured in USD Million, experienced a recovery and steady expansion through the 2020–2025 historical window, rising from the low-300s to reach a base-year value in 2025. Our forecast shows continued growth under a mid-single-digit compound environment, with a compound annual growth rate (CAGR) of 2.51% across 2026–2032, reaching the mid-400s (USD Million) by 2032.

Cyclohexene (CAS 110-83-8) Market

Demand composition: Demand drivers are anchored in intermediates for fine chemicals, specialty solvents, and laboratory-grade products. Overlays such as pharmaceutical API synthesis cycles, agrochemical formulation pipelines, and specialty resin production create differentiated pockets of value for high-purity versus technical-grade supply.

Cyclohexene (CAS 110-83-8) Market

Supply structure and concentration: Market concentration metrics indicate a moderately fragmented industry — the top three suppliers do not dominate the market, and the top five collectively command a modest share. That configuration creates both risk (sensitivity to outages at several regional hubs) and opportunity (ability for buyers to negotiate and for new entrants to gain footholds via differentiated value propositions).

The historical dataset (2020–2025) captures pandemic-era disruption, a rebound with recovery in downstream industrial activity, and an acceleration into 2024–2025 driven by restocking and renewed capital spending in end-use sectors. In our baseline forecast, growth moderates but remains positive through 2032. For decision-makers in 2026, the implication is clear: investments timed to mid-cycle demand can deliver steady returns, but managers should avoid assuming rapid expansion that would justify large, inflexible new capacity without adaptive clauses or staged capital deployments.

High-purity cyclohexene: Premium applications (pharma, specialty agrochemicals) demand tighter impurity profiles and reliable certification. These buyers are willing to trade price for guaranteed supply and technical support. Contract structuring that blends spot purchase with long-term offtake and quality-based premiums is a recommended approach.

Technical-grade and industrial volumes: These segments are more price-sensitive and tied to cyclical downstream industries. Procurement strategies that leverage blended sourcing — regional producers for cost and specialty suppliers for contingency — reduce exposure to single-source disruptions.

Adjacency and value-added services: Suppliers that provide regulatory dossiers, impurity profiling, and small-batch formulation support capture higher margins and stickier customer relationships. For buyers, sourcing partners with technical service capabilities reduce time-to-market for new formulations.

The market features a mix of integrated petrochemical majors, regional specialty manufacturers, and global distributors. Understanding each archetype helps in designing procurement strategies, partnership frameworks, and M&A screens.

BASF SE (Ludwigshafen, Germany) — An integrated chemical major producing high-purity cyclohexene via benzene hydrogenation at its complex. Its strengths are global reach, stringent quality systems, and the ability to serve pharmaceutical and specialty chemical customers with consistent specification and regulatory support.

Chevron Phillips Chemical Company (Houston, Texas, United States) — A Gulf Coast-based producer that leverages benzene hydrogenation units for industrial and specialty uses. Its competitive advantage lies in feedstock integration and downstream logistics in North America.

ExxonMobil Chemical Company (Spring, Texas, United States) — A selective hydrogenation route provider focused on high-purity outputs for pharmaceutical and agrochemical synthesis. Scale, process control, and internal R&D capabilities are its core differentiators.

Metadynea Austria (Krems, Austria) — A regional specialist supplying selective-hydrogenation-derived cyclohexene for fine chemicals and pharmaceutical intermediates. Its positioning favors tailored, small-volume technical support and specialty formulations.

Parchem Fine & Specialty Chemicals (Queens, New York, United States) — A distributor and global supplier of cyclohexene as a specialty chemical, focused on supply chain responsiveness and customer-specific packaging and stabilization solutions.

Charkit Chemical Corporation (Stamford, Connecticut, United States) — A raw-material-focused supplier that serves industrial markets, emphasizing logistical flexibility and inventory-backed service levels.

Sigma-Aldrich (Merck) (St. Louis, Missouri, United States) — A laboratory-supply specialist that markets stabilized cyclohexene for research and small-scale synthesis, where traceability and certification are decisive procurement criteria.

The PW Consulting deliverable is not a descriptive brochure; it is an execution toolkit. Highlights include:

Granular demand models by application and region, scenario-modeled across three macroeconomic pathways, with price elasticity matrices and sensitivity analyses to feed procurement and financial models.

Supply-mapping with unit-level capacity, lead-time risk scores, and contingency routing for logistics interruptions — designed to support dual-sourcing decisions and inventory policy calibration.

Supplier scorecards that combine technical capability, regulatory readiness, ESG alignment, and commercial flexibility to rank prospective partners for long-term contracts or strategic alliances.

Contract and negotiation playbooks tailored to buyer archetypes (asset-heavy industrial buyers, R&D-driven specialty formulators, distributors), including sample commercial clauses for quality warranties, force majeure, and capacity ramp commitments.

Regulatory and compliance dossiers across major markets, plus a roadmap for registering high-purity grades — critical input for product development timelines in regulated end-uses.

Commercial scenarios and ROI models for greenfield capacity, brownfield expansions, and tolling arrangements, with break-even analyses keyed to our forecast price and demand bands.

The market’s modest growth masks concentrated operational risks: feedstock volatility, selective hydrogenation process constraints, and regional logistics bottlenecks. Our study offers prioritized mitigation levers that are immediately actionable for 2026 planning cycles:

Flex capacity and tolling options to manage capital intensity and match demand uncertainty.

Tiered contracting that blends fixed-volume commitments for critical high-purity grades with index-linked spot purchasing for industrial volumes.

Strategic inventory positioning at cross-dock nodes to offset regional supply interruptions and seasonal demand swings.

Supplier development programs to cultivate second-source options and co-invest in quality upgrades where technical barriers restrict supply competition.

Prioritize flexible contractual structures: Given our baseline CAGR of 2.51% and the forecast shape to 2032, firms should avoid large, fixed-expense capacity commitments without embedded flexibility or off-ramps.

Segment procurement by value-to-business: Differentiate strategies for high-purity, high-margin applications versus commodity industrial uses. Allocate working capital and insurance differently across these buckets.

Invest selectively in supplier partnerships that offer regulatory documentation and technical support — the premium for such services often outperforms the cost in reduced time-to-market for regulated products.

Embed ESG and feedstock resilience in supplier selection: sustainability metrics and feedstock diversification are increasingly priced by end-customers and regulators.

Use scenario planning to stress-test M&A and expansion options: our report provides modeled returns under upside, base, and downside demand scenarios to inform timing and structure of investments.

Share this strategic synopsis with procurement, commercial, and R&D leadership as a focal point for cross-functional workshops in Q1–Q2 2026. Use the high-level conclusions to set tactical mandates (e.g., supplier rationalization targets, technical partner engagements, inventory buffer thresholds) and then engage PW Consulting for the granular inputs required to operationalize those mandates.

This article intentionally demonstrates PW Consulting’s analytical depth and the practical levers our cyclohexene market study unlocks for 2026 corporate decision-making while withholding the core segmented matrices and supplier-specific economics that deliver competitive advantage. If your team needs the complete datasets, micro-segmentation, supplier scorecards, and executable transaction templates, the full report and our advisory services grant direct access to those assets — enabling you to convert market insight into measurable commercial outcomes.

Contact PW Consulting to schedule a briefing and to obtain the full cyclohexene market dossier, model files, and tailored scenario sessions for your organization’s 2026 strategy cycle.

For detailed analysis of this topic, please visit the official page:Cyclohexene (CAS 110-83-8) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com