Polyurethane Dispersion Market: Insights and Competitive Analysis

Other |

2026-05-04 05:27:26

PW Consulting presents a focused industry briefing designed to inform executive decisions in 2026 for companies operating in, or considering entry to, the Non‑Radioactive Nucleic Acid Labeling Products market. This preview synthesizes our macro market model, regulatory inflection points, competitive dynamics, and action‑oriented strategic options. It deliberately demonstrates analytical depth while withholding granular segmentation tables and proprietary channel‑level figures to encourage access to the full report for transaction‑grade intelligence.

Non-Radioactive Nucleic Acid Labeling Product Market

The non‑radioactive labeling segment has moved from a niche laboratory convenience to an operational standard across diagnostic development, genomics research, and molecular pathology workflows. Our market model — calibrated on historical performance (2020–2025) and rigorous bottom‑up input factors — shows the market expanding from a 2025 base to a materially larger footprint by the end of the forecast horizon. Specifically, the market is estimated at USD 241.5 Million (base year 2025) and is projected to reach approximately USD 412.1 Million by 2032, reflecting a compound annual growth rate (CAGR) of 8.2% over the forecast period (2026–2032). The near‑term acceleration is visible in our 2026 point estimate, which demonstrates continuity of demand as adjacent diagnostic and life‑science segments recover and invest in non‑radioactive probe technologies.

Non-Radioactive Nucleic Acid Labeling Product Market

Demand drivers: End‑user adoption is being pulled by three structural trends — regulatory preference for non‑radioactive workflows, cost and safety benefits in clinical labs, and expanded R&D activity in nucleic acid‑based diagnostics and therapeutics.

Non-Radioactive Nucleic Acid Labeling Product Market

Technology vectors: Fluorescent and covalent‑attachment chemistries continue to evolve, improving signal/noise and enabling multiplexing. Incremental gains in labeled nucleotide performance and kit usability are unlocking new applications beyond traditional hybridization and blotting.

Commercial dynamics: The market exhibits strong concentration among incumbent suppliers and specialized kit producers, creating both barriers to entry and fertile ground for strategic consolidation or focused differentiation.

Regulatory developments have materially altered the operating context. The U.S. Food and Drug Administration’s reclassification of in situ hybridization test systems in June 2025 removed prior constraints around non‑radioactive labeled probes and FISH techniques, effectively acknowledging the maturity and clinical acceptability of these technologies. That regulatory shift reduces one important source of uncertainty for clinical applications and accelerates procurement cycles for clinical labs and diagnostic OEMs. For strategy teams, the implication is clear: pathways to clinical adoption have shortened, and comparative performance—not just regulatory clearance—will drive vendor selection.

Proprietary market model (2020–2032): full historical calibration and scenario runs for base, upside and downside demand cases, with sensitivity levers you can toggle for pricing, reimbursement, and adoption velocity.

Go‑to‑market playbooks: validated channel mixes, promotional mechanics for reagent kits versus custom probe services, and distributor partner scorecards.

Technology benchmarking: comparative feature maps across labeling chemistries, protocol complexity index, time‑to‑result metrics, and reagent shelf‑stability matrix.

Regulatory and reimbursement impact matrix: consequence mapping for regulatory events (like the FDA reclassification), plus market access triggers in key jurisdictions.

Commercial due diligence toolkit: unit economics templates, M&A valuation checklists, and integration playbooks for bolt‑on acquisitions or strategic alliances.

Competitive intelligence appendices: supplier scorecards, product lineage timelines, patent landscape summaries, and named‑player SWOTs (executive‑level summaries included below).

The market is anchored by a compact set of established suppliers and specialist kit manufacturers. Firms to watch include legacy innovators, reagents specialists, and broad‑line life sciences companies that have extended into labeling technologies. Key incumbents profiled in our study include:

Enzo Biochem, Inc. (Farmingdale, NY) — long‑standing pioneer in non‑radioactive labeling and probe systems, with recognized product platforms for ISH and gene analysis (https://www.enzo.com).

New England Biolabs (Ipswich, MA) — a trusted supplier of labeling reagents and enzymatic kits, with strong adoption in molecular biology workflows (https://www.neb.com).

Vector Laboratories, Inc. (Newark, CA) — focused on covalent biotinylation and end‑tagging kits designed for ease of use and direct probe attachment (https://vectorlabs.com).

Jena Bioscience GmbH (Jena, Germany) — specialist in labeled nucleotide chemistries and high‑concentration probes for efficient enzymatic incorporation (https://www.jenabioscience.com).

Mirus Bio LLC (Madison, WI) — developer of one‑step fluorescent labeling kits focused on minimizing protocol steps (https://www.mirusbio.com).

Promega Corporation (Madison, WI) — offers a suite of non‑radioactive detection reagents used across hybridization and blotting workflows (https://www.promega.com).

Thermo Fisher Scientific Inc. (Waltham, MA) — a full‑line supplier with broad fluorescent, biotin, and hapten labeling kits and strong channel reach (https://www.thermofisher.com).

These players set commercial benchmarks across product quality, channel coverage, and technical support. Our full report contains comparative scorecards that quantify product maturity, supply reliability, pricing posture, and innovation velocity — information you will need for competitive positioning or acquisition diligence.

Rationalize R&D roadmaps around clinical enablement: With regulatory headwinds reduced, prioritize investments that address robustness, multiplex compatibility, and simplified workflows that clinical laboratories can adopt without retraining large cohorts of technicians.

Channel and pricing strategy: For kit manufacturers, hybrid sales models (direct OEM sales plus distributor networks) will accelerate reach. For platform suppliers, consider differentiated pricing that reflects protocol‑time savings and reduced safety overheads in clinical settings.

Partnerships over unilateral expansion: Strategic alliances with diagnostic OEMs and pathology service providers can create bundled offerings that embed labeled probes into validated end‑to‑end workflows — an effective way to capture higher margin service revenues.

M&A criteria: Target technical gaps (e.g., multiplex fluorescent chemistries or rapid covalent labeling IP), narrow geography playbooks, or manufacturing capacity constraints. Our acquisition checklist in the report scores targets across technology defensibility, customer stickiness, and regulatory readiness.

Operational resilience: Ensure supply‑chain redundancy for labeled nucleotide precursors and conjugation reagents; lead times and QC variability can materially affect launch timelines for diagnostic customers.

Executives typically approach this market with one of three strategic intents: grow a reagent or kit business, embed labeling into a larger diagnostic product, or acquire specialized capability to accelerate a pipeline. Our scenario runs translate those intents into a small set of KPI outcomes — revenue growth, margin expansion, payback period for R&D, and time‑to‑market under different adoption curves. For example, a company that accelerates clinical validation programs and secures two OEM partnerships within 18 months can materially outpace the base market CAGR; a business that competes solely on price without differentiation is likely to see slower growth due to the incumbents’ technical moats.

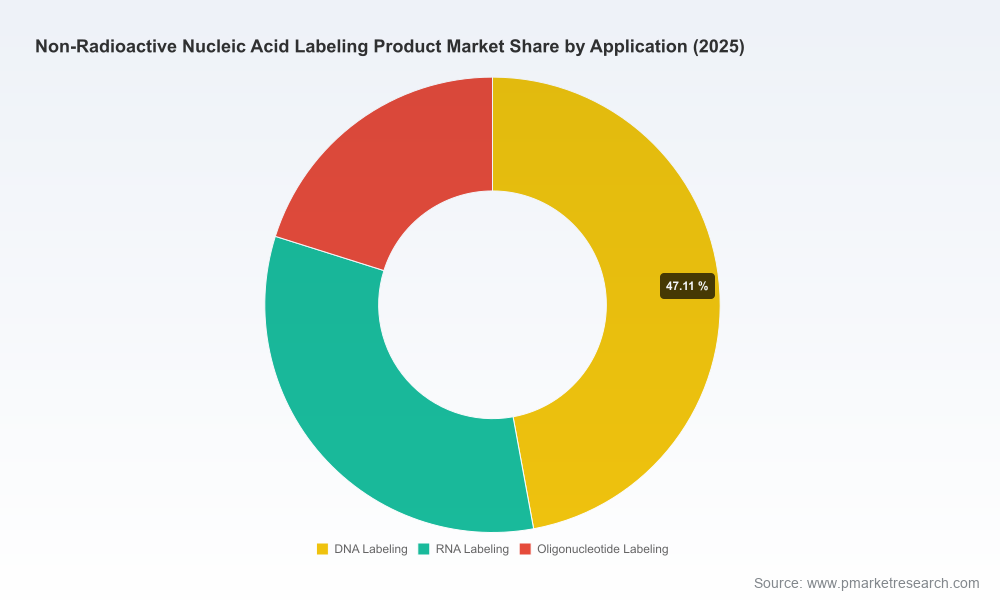

To preserve actionable differentiation, this preview intentionally omits granular regional splits, application‑level percentages, and the full competitor pricing matrices that underpin our valuations. The full PW Consulting report provides those breakdowns, downloadable market models, and client‑ready slide decks that allow you to run your own scenario permutations. If you are evaluating M&A targets, preparing a market entry plan, or aligning R&D budgets for 2026, that level of granularity is essential — and included in the complete study.

Short list: Use the briefing to validate high‑level strategic direction for Q1 2026 (R&D spend, partnership outreach, initial go‑to‑market budget).

Subscribe: Access the full report to obtain the model, competitor scorecards, and deal screening tools needed for transaction decisions.

Engage: PW Consulting can perform a tailored deep‑dive — combining our market model with your internal data to generate a bespoke commercial or M&A playbook aligned to your 2026 targets.

In an industry where regulatory shifts and incremental chemistry improvements rapidly change product viability, having a calibrated market model and practical playbooks is non‑negotiable. PW Consulting’s full Non‑Radioactive Nucleic Acid Labeling Product Market study provides the analytic rigor and executable guidance that senior management teams need to convert the 2026 opportunity into measurable growth. Contact us to access the complete report and the underlying data model.

For detailed analysis of this topic, please visit the official page:Non-Radioactive Nucleic Acid Labeling Product Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com