Motorcycle Market 2026 Strategic Outlook — Actionable Intelligence for Executive Decisions

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present an executive primer on our latest Motorcycle Market study. This article synthesizes the study’s strategic implications for 2026 corporate decision-making: why near-term moves matter, where structural opportunities and risks lie, and which capabilities will separate winners from laggards. The commentary is deliberately diagnostic and directional — it demonstrates the analytical depth of the full study while withholding granular segment-level tables so clients consult the report for the complete dataset and interactive models.

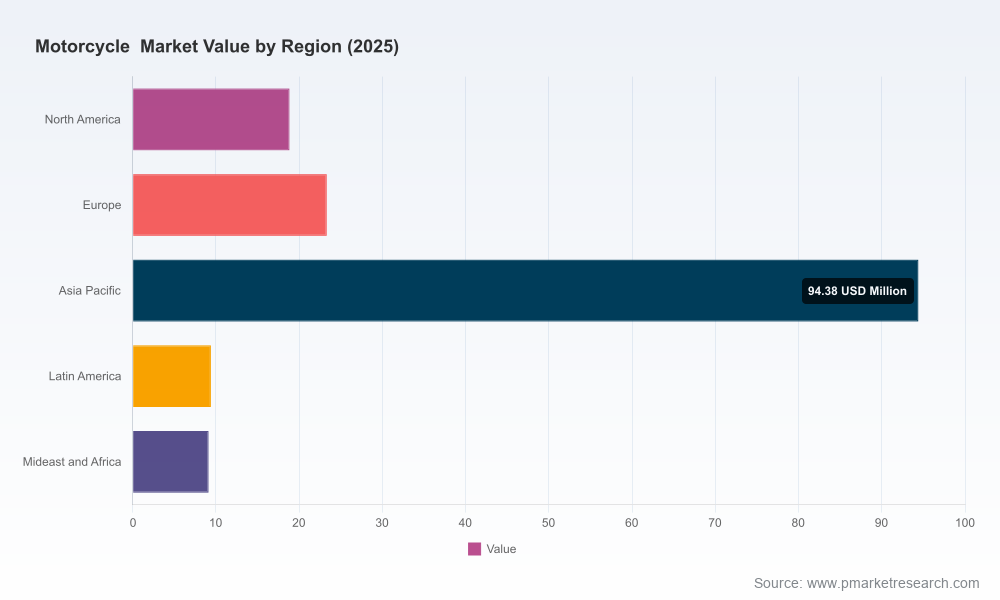

Motorcycle Market

Market snapshot: trajectory, volatility and the near-term baseline

Our study uses 2025 as the base year and maps historical performance across 2020–2025 with a forward-looking forecast window of 2026–2032. The headline forecast is a steady but moderate recovery: an aggregated market path that translates to a 3.2% compound annual growth rate over the forecast horizon. After the uneven post-pandemic recovery and a brief softness observed in the mid-cycle, the market re-established positive momentum into 2025 and is expected to expand through 2032, reaching a higher long-run scale than the near-term troughs.

Motorcycle Market

Two summary takeaways from the topline numbers that should inform 2026 planning: first, growth is positive but not explosive — capital allocation must prioritize returns and optionality; second, cyclical noise and regulatory interventions create discrete windows where cost and footprint optimization can materially affect competitiveness.

Motorcycle Market

Why this study matters for 2026 decisions

- Portfolio prioritization under constrained growth: With modest overall expansion, incremental volume gains are earned, not given. Companies must choose between broad model proliferation and concentrated investments in high-return SKUs and services.

- Supply-chain and tariff sensitivity: Recent trade-policy shifts create a new margin lever. Firms that act quickly to re-source or renegotiate contracts can convert policy changes into measurable margin uplift within fiscal year cycles.

- Product architecture and modularization: The proliferation of new model variants increases complexity and per-unit costs. Platform standardization and electronics-sharing are now sources of margin differential.

- Premiumization vs. mass-market plays: Premium models and lifestyle products remain resilient; mass commuting volumes will be concentrated in price- and fuel-efficiency-sensitive cohorts. Each path implies different channel and service strategies.

- Service, software and recurring revenue: As hardware growth moderates, monetizable aftersales, connected services and subscription offers become critical to sustaining enterprise-level margin expansion.

Competitive dynamics — interpreting OEM moves in 2026

The industry’s leading OEMs have signaled strategy through product launches, platform investments and targeted line-up refreshes. Below are high-level strategic readings of the principal players tracked in the study. These summaries focus on directional implications rather than exhaustive competitor matrices (those are available in the full report).

- Honda (Japan): Large-scale product introductions and continued investment in combustion and hybridized architectures — including expanded clutch technologies and an electric variant within marquee families — indicate a dual-path strategy: defend volume leadership while selectively piloting electrification. Expect continued leverage of scale in global procurement and an emphasis on high-volume core models.

- Yamaha (Japan): A broad on-road and off-road refresh shows Yamaha’s intent to defend diverse market niches. The company’s simultaneous push across sport, mid-capacity and small-displacement portfolios suggests they will compete on breadth and channel coverage rather than premium-only differentiation.

- Harley‑Davidson (United States): New premium families, high-displacement engines and limited editions reflect a premium-first strategy that leans on brand equity and lifestyle conversion. This approach favors higher per-unit margins and a focus on experiential retail and subscription services.

- BMW Motorrad (Germany): Incremental model updates and enhanced care programs point to a service-led premium strategy: expand lifetime customer value through care packages and targeted model evolution rather than high-volume SKU expansion.

- Kawasaki (Japan): New mid-range and retro/adventure entries indicate a focus on segments that deliver favorable margin profiles while keeping development costs controlled through platform reuse.

- Ducati (Italy): Continued emphasis on high-performance powertrains and niche off-road variants signals sustained pursuit of the high-margin, brand-driven customer segment and motorsport-derived halo effects.

- Triumph (UK): A large slate of new models — including strong heritage and lifestyle plays — underlines a growth-through-differentiation strategy: broaden appeal while preserving brand DNA.

- Suzuki (Japan): Targeted mid-capacity updates and electronics upgrades reflect a pragmatic engineering-led route to competitiveness, focusing on price/performance and incremental technology adoption.

What ties these moves together is the rising importance of software, electronics and modular production. OEMs that can reduce SKU complexity via common electrics stacks and shared platforms will extract outsized margin improvements. Suppliers able to deliver integrated mechatronics, ride-by-wire systems and scalable software stacks will increasingly command premium pricing.

Regulation and trade: the April 2026 turning point

A material policy development during the reporting period was the restructuring of Section 232 trade measures in April 2026. Notably, certain motorcycle manufacturing inputs were placed on an exemption list and in some cases finished units gained relief from duties. The practical implications for OEMs and suppliers are immediate:

- Manufacturers with U.S. assembly capacity gain a near-term competitiveness advantage through lower input costs and simplified sourcing optimization.

- Companies that locked multi-year procurement contracts without tariff pass-through clauses face renegotiation windows; firms that act fast can secure improved COGS profiles.

- Longer-term, the policy changes reduce one barrier to reshoring for select production steps, but they also increase policy dependency risk — continued monitoring and scenario planning remain essential.

What the report contains — practical deliverables for 2026 execution

Our full Motorcycle Market study was designed as an operational tool for strategy and corporate development teams. Highlights include:

- Proprietary topline model and seven forward scenarios calibrated to macro, supply and demand drivers (base year 2025; forecast period 2026–2032; headline CAGR 3.2%).

- Competitive playbooks for the eight OEMs summarized above, including SKU-level tracking, launch calendars and product ROI benchmarks.

- Supply-chain heatmaps and an inputs-tariff impact model that quantifies alternative sourcing, logistics and duty outcomes under different policy scenarios.

- Aftermarket and services valuation frameworks, plus KPIs for subscription and connected-services pilots.

- M&A and JV screening templates and an investment prioritization matrix tailored to manufacturing scale, brand positioning and technology needs.

- Implementation roadmaps (90/180/360 day checklists) and a risk register tied to regulatory and commodity-price sensitivities.

- Interactive appendices and dashboards for drill-downs; note that full segment tables, regional splits and application-level breakouts are detailed only in the complete report to protect competitive confidentiality.

90/180/360-day strategic checklist for executives

- 90 days: Run tariff-sensitivity audits on major supplier contracts; prioritize SKU rationalization candidates and begin supplier negotiations tied to new duty realities.

- 180 days: Launch a modular-platform pilot (mechanical + electronics commonality) and start a controlled customer trial for a connected service/subscription offering.

- 360 days: Execute capacity rebalancing for manufacturing footprints if scenario modeling supports near-shoring, and mobilize M&A diligence on 2–3 targets flagged by our screening framework.

Final perspective: how to use this intelligence in 2026

Decision-makers should treat the market’s moderate growth and the recent policy changes as an invitation to be deliberate: target investments that produce durable margin expansion (platform commonality, software, services), use the tariff window to improve cost competitiveness, and align product portfolios with clearly defined customer segments. The full PW Consulting Motorcycle Market study provides the granular segmentation, scenario outputs and executable playbooks you need to operationalize those priorities.

If your leadership team is preparing capital allocation, manufacturing footprint, or M&A decisions for 2026, this study is designed to convert market signals into prioritized actions. For access to the full dataset, segmented forecasts, and interactive tools referenced here, please consult the PW Consulting market report. Our team stands ready to support tailored workshops and rapid implementation sprints to translate insights into measurable value.

For detailed analysis of this topic, please visit the official page:Motorcycle Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com