Why Managed SOC Services Are Essential for U.S. SMEs to Defend Healthcare Data Against Rising Cyber Threats

Health |

2026-07-07 06:20:30

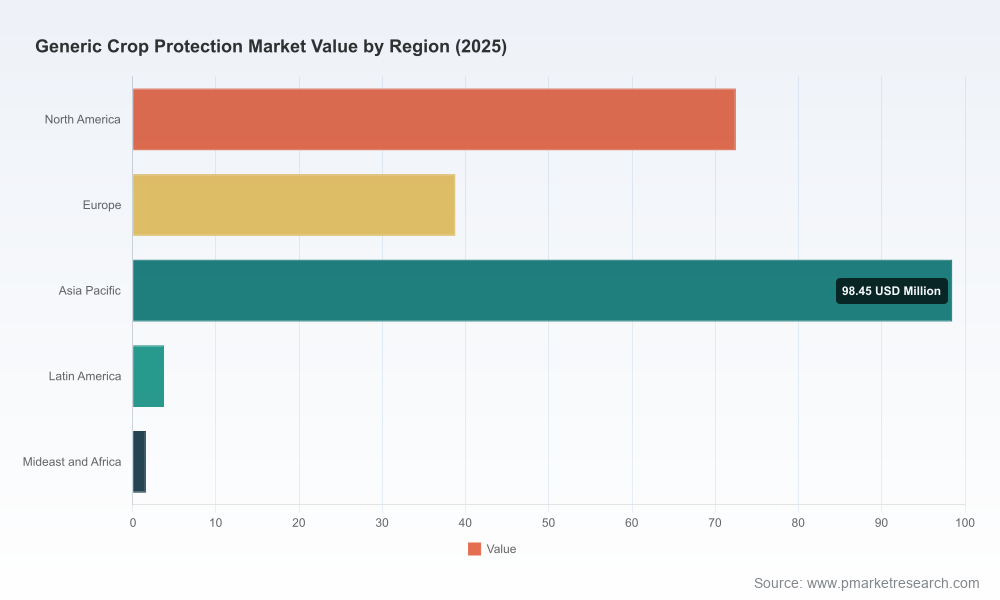

As agricultural supply chains move from crisis response to strategic re‑balancing, the generic crop protection market is entering a phase where scale, formulation sophistication, and channel access will determine winners and losers. Our PW Consulting Generic Crop Protection Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes the market’s recent trajectory and projects a steady expansion at a compound annual growth rate (CAGR) of approximately 4.45% across the forecast window. The market reached roughly USD 215 million in 2025 and is projected to continue growing toward the high‑hundreds of millions by 2032 under current assumptions.

Generic Crop Protection Market

This introduction outlines the study’s strategic value for 2026 planning: it translates macro momentum into discrete strategic options, highlights the critical competitive and regulatory inflection points, and prescribes pragmatic decision paths for commercial, supply‑chain, and M&A leaders. True to the “trailer” principle, we demonstrate analytical depth and strategic line‑of‑sight while withholding detailed segment tables and modeled outputs — these are available in the full report.

Generic Crop Protection Market

A resilient baseline: After recovering from pandemic‑era disruptions, the generic crop protection market has shown consistent year‑on‑year expansion. The combination of capacity shifts, renewed registration activity and steady crop protection demand underpins the projected CAGR through 2032.

Generic Crop Protection Market

Structural growth drivers: Three structural forces are driving the market — transitions in active ingredient supply and manufacturing, increased adoption of advanced formulations (to reduce drift and improve efficacy), and intensified digitalization of farmer advisory and product selection.

Volatility vectors: Near‑term volatility will come from regulatory approvals and litigation outcomes, price competition from low‑cost producers, and consolidation moves by larger ag‑chem players repositioning toward innovation. These vectors create differentiated opportunity windows for value capture in 2026 versus later years.

The market exhibits moderate concentration among the top players (top‑3 firms account for a majority share; top‑5 concentration rises further), which informs negotiation dynamics across distribution, raw materials, and contract manufacturing. Major participants focus on three distinct capability clusters: scale manufacturing, differentiated formulations, and channel integration via digital tools.

UPL Limited (Mumbai): UPL is leveraging a two‑track playbook — expanding formulation breadth while deploying digital farmer support tools to strengthen product stickiness. The company’s recent launch of an integrated digital advisory platform signals a move toward service‑led differentiation that goes beyond commodity price competition.

ADAMA Agricultural Solutions (Ra’anana): ADAMA’s recent product entries into dual‑action herbicide formulations demonstrate how technical differentiation (efficacy across crop cycles) can open high‑value hectares even within a generics market. Their approach shows the commercial premium for formulation R&D, faster registration pathways, and broad application messaging.

Albaugh LLC (Ankeny): Albaugh’s microencapsulated insecticides — purpose‑built to reduce drift — exemplify how formulation science can lower application costs and meet increasingly stringent environmental expectations. Expect these capabilities to be used both defensively and as acquisition‑grade IP.

AMVAC, Rotam, Sipcam and peers: These firms emphasize flexible manufacturing, white‑label partnerships, and regional go‑to‑market agility. Their value proposition focuses on shortened time‑to‑shelf and competitive pricing while selectively investing in niche formulation advantages.

Emerging Asian suppliers and regional partnerships: Strategic distribution partnerships are expanding footprint in underpenetrated geographies. These tie‑ups are intensifying competition on price and availability, particularly in markets where registration pathways have been liberalized.

Registration momentum: The period 2023–2025 saw a surge in generic registrations and new formulations globally. This has expanded product choice and compressed margins in commoditized pockets; conversely it creates arbitrage for players who can combine regulatory speed with differentiated application value.

Major incumbents repositioning: Several large incumbents have announced strategic exits or refocusing from generic active ingredient manufacturing toward innovation. These moves change the supply equation — reducing competition in some AIs while accelerating consolidation elsewhere.

Antitrust and distribution litigation: Pending litigation and regulatory scrutiny targeting loyalty or exclusivity programs in distribution channels could reconfigure access for generic suppliers. A favorable judicial outcome for plaintiffs could unlock distribution opportunities; conversely, settlements preserving ties may maintain higher barrier structures.

Formulation and environmental compliance: Pushes to reduce drift and non‑target exposure — plus buyer demand for lower environmental footprint — elevate investment returns on advanced formulations and application technologies.

Against the macro backdrop, executives must choose a coherent strategic posture. Our research highlights three viable archetypes, each with concrete operational implications:

Scale & cost leadership — invest in manufacturing scale, sourcing optimization, and lean distribution to defend margin against low‑price entrants. Critical capabilities: long‑term feedstock contracts, multi‑site quality control, and aggressive channel economics.

Differentiation through formulation and services — prioritize R&D in micro‑encapsulation, drift‑reduction, and combination formulations; couple with advisory/digital tools to capture adoption premiums. Critical capabilities: formulation IP, rapid registration playbook, and commercial integration with precision‑ag platforms.

Targeted partnership & asset play — pursue bolt‑on M&A or distribution partnerships to enter selective geographies or technologies quickly. Critical capabilities: M&A integration playbook, local regulatory expertise, and flexible supply contracts.

Most pragmatic strategies for 2026 will be hybrid: protect core cost positions while piloting differentiated formulations and digital services that can be scaled if adoption economics prove compelling. The choice of emphasis should be informed by quantified NPV trade‑offs — the full report contains scenario models that map these trade‑offs under alternative regulatory and price scenarios.

The full Generic Crop Protection Market study is structured to support boardroom decisions and commercial execution across 2026 planning cycles. Key practical deliverables include:

Market forecasting model (2026–2032) with scenario toggles for price, registration velocity, and raw material shocks — enabling rapid sensitivity testing for strategic options.

Regulatory tracker and risk matrix capturing registration approvals, notable de‑registrations, and litigation timelines that materially affect market access.

Commercial playbooks tailored to each strategic archetype: go‑to‑market steps, pricing frameworks, distributor negotiation scripts, and KPI dashboards for first 18 months.

Supply‑chain resilience toolkit including alternative sourcing maps, contract manufacturing scorecards, and inventory optimization levers.

Company profiles and competitor intelligence for the major generic players, including capability maps, recent product launches, and near‑term strategic options — curated to aid both organic and inorganic decision making.

Investment and M&A heuristics: target selection filters, valuation benchmarks, and integration checklists calibrated to the market’s concentration dynamics.

Embed the forecast and scenarios in your annual operating plan to stress‑test revenue targets under different regulatory and competitive outcomes.

Use the formulation and digital adoption case studies to prioritize product development funding and pilot geographies where adoption barriers are lowest.

Leverage the supply‑chain toolkit to create contingency plans for raw material dislocations or capacity exits by major players.

Apply our M&A heuristics to shortlist targets that accelerate either formulation capabilities or access to high‑growth channels, with clear integration milestones.

2026 will be a decisive year in the generic crop protection market. The combination of steady market growth, reformulation opportunities, realignments by large incumbents, and pending legal/regulatory outcomes creates multiple gating factors for value capture. Organizations that systematically align investment choices with a clear playbook — whether for scale, differentiation, or strategic partnering — will convert market uncertainty into competitive advantage.

PW Consulting’s full Generic Crop Protection Market report supplies the granular data, scenario models, and operational templates necessary to convert these strategic options into executable plans. For access to the detailed segmentation tables, regional and application models, and downloadable financial scenarios, please visit the report landing page.

For detailed analysis of this topic, please visit the official page:Generic Crop Protection Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com