Integrated Microwave Assembly Market Report: Trends, Drivers, and Strategic Analysis

Art |

2026-06-19 10:41:59

As PW Consulting’s lead industry analyst, I present a focused, decision-oriented preview of our Atomized Ferrosilicon Market research. This brief synthesizes the macro trajectory, competitive dynamics, regulatory shocks and the practical levers that senior executives must consider when setting strategy for 2026. The purpose is to signal the depth and applicability of the full study while preserving the proprietary granular segment outputs that materially affect commercial decisions — those live tables, plant-level cost curves and customer-by-customer demand models are available in the full report.

Atomized Ferrosilicon Market

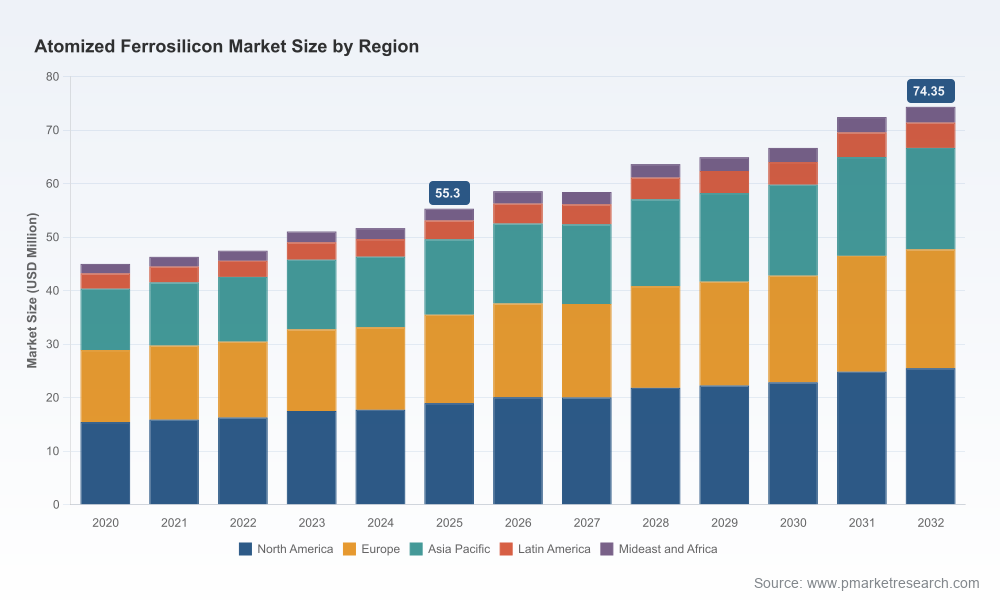

The atomized ferrosilicon market has shown steady recovery and structural growth over the past half decade. Using 2025 as our base year, the market reached approximately USD 55.3 Million (revenue unit: Million USD) after expanding from roughly USD 45.0 Million in 2020. Our forecast models — built on production, downstream steel & foundry demand, energy and trade policy scenarios — point to a compound annual growth rate of 4.3% through the 2026–2032 horizon.

Atomized Ferrosilicon Market

Projected output shows a continued upward trend, with an initial increase into 2026 and a pathway that reaches the mid-2030s level by 2032. Year-to-year movements in our series reflect micro-cycles driven by downstream steel output, episodic trade restrictions and localized capacity additions; expect some short-term noise but persistent mid-term expansion supported by alloy demand in specialty steel, casting and dense-media applications.

Atomized Ferrosilicon Market

Portfolio prioritization: Moderate, stable CAGR combined with pockets of premium demand makes 2026 a year for selective investment rather than ubiquitous scale-up. Companies should shift from volume-chasing to margin-chasing: target atomized grades and product forms that command quality premiums and long-term off-take durability.

Supply security & sourcing: Recent trade measures and tariffs have reshaped shortest-path sourcing. Buyers and producers will need dual playbooks — a baseline of contracted supply with longer tenors and a contingency layer for spot and regional supply. Procurement teams that implement layered contracting (firm volumes + call options + short-term buying authority) will materially reduce margin volatility in 2026.

CapEx discipline: Given the market’s steady but not explosive growth, greenfield projects require stronger hurdle rates. Brownfield debottlenecking, product-differentiation investments (e.g., atomization technology upgrades to improve spherical yield) and electrification of thermal processes offer higher IRR and lower execution risk in 2026.

Regulatory readiness: International trade actions and safeguard measures are no longer tail risks. They are active drivers of regional pricing and route-to-market strategies. Firms should embed trade-policy scenarios into all 2026 commercial plans and maintain dedicated regulatory monitoring tied to commercial contracting cycles.

The competitive landscape displays a mix of global groups, regional champions and specialty players. Market concentration is meaningful: the top three firms control a dominant share of installed capacity, and the top five capture an even larger proportion — a structural reality that creates both barriers and opportunities.

Ferroglobe PLC (UK) — A leader in high-purity grades with atomized powder lines optimized for deoxidizer and inoculant applications. Strengths: brand recognition in steel markets, established off-take relationships, and technical grades that reduce downstream variability.

Elkem ASA (Norway) — A strategic differentiator on low-carbon production. Elkem’s emphasis on renewable-powered reduction and metallurgy positions it to capture sustainability-seeking buyers and premium pricing in Europe.

DMS Powders (South Africa) — Specialist supplier focused on dense media separation with spherical atomized products. Its niche orientation gives it pricing insulation in industrial minerals and mining-related channels.

Large Chinese producers (e.g., Erdos Group, Sinosteel affiliates) — Scale players that influence global price floors and short-term availability. Their strategic posture will determine the pace at which low-cost output rebalances into export markets when trade barriers relax.

Regional and specialty firms (Om Holdings, Eramet, Washington Mills, Jayesh Group, Anyang Huatuo, Kovohuty, Fesil, IMEXSAR, M & M Alloys) — These companies are important competitive fabric: some combine local captive steel demand with export-led ambitions; others succeed through differentiated powder morphology or service models. Their smaller size belies significance in local procurement pools and niche segments.

Strategically, incumbent groups with premium-grade capabilities or low-carbon credentials will see differentiated demand growth in 2026. Smaller specialists that control unique particle geometries or application know-how can be attractive M&A targets for both upstream producers seeking product breadth and downstream consumers seeking security of supply.

Tariffs and safeguard measures implemented across major markets have already reallocated trade flows and temporarily tightened regional availability. These interventions create arbitrage and force nearer-term re-contracting patterns for import-dependent buyers.

Anti-dumping determinations against certain origins further complicate supply planning and raise the value of diversified sourcing strategies. Buyers must prepare for administrative lead times and price pass-through mechanics that will influence negotiations throughout 2026.

Parallel to trade actions, capacity investments in producer countries continue — new plants and expansions shift long-term supply curves and mean that firms must balance near-term supply security against future price normalization when new capacity ramps.

Conduct a supplier criticality heatmap: segment suppliers by technical fit, lead time, trade exposure and carbon profile. Use the heatmap to set contracting priorities and to define strategic vs. tactical spend.

Negotiate outcome-based contracts with key downstream customers: trade volume certainty for premium pricing on value-added atomized grades tied to metal yield, rework reduction or energy savings.

Accelerate selective CAPEX on atomization process efficiencies and particle control: even marginal improvements in spherical yield or size distribution can unlock higher margin channels (precision casting, specialty steel).

Adopt a dual-sourcing strategy with embedded flexibility: a core long-term supplier with defined escalation mechanics plus a verified secondary supplier pool able to provide emergency supply within contractually specified response times.

Embed regulatory scenario triggers into procurement and pricing playbooks: create pre-approved contract templates and rapid re-pricing clauses aligned to tariff or safeguard events.

Evaluate M&A and partnership targets not merely on capacity but on proprietary atomization technology, low-carbon production pathways and application-specific know-how. These assets confer durable commercial advantage beyond scale alone.

Granular demand and supply models by product form, application and region with scenario toggles for trade interventions and energy price shocks.

Comprehensive competitive dossiers: plant-level footprints, product portfolios, recent capital projects and strategic intent assessments for the major and mid-tier players highlighted above.

Price and margin sensitivity matrices that translate raw material and energy moves into cash-flow impacts — intended for CFOs and procurement heads to stress-test budgets.

M&A target screens and integration playbooks: value-creation roadmaps for bolt-on acquisitions, from due-diligence checklists to post-merger synergy templates.

Regulatory impact maps and trade-policy playbooks that link likely administrative outcomes to commercial actions under multiple time horizons.

Operational toolkits for procurement and supply continuity: layered contracting templates, inventory optimization algorithms and emergency supplier activation sequences.

Treat this piece as a strategic primer that frames key choices for 2026: secure supply with economics, invest selectively in product and process differentiation, and make policy risk a first-class input into commercial decisions. The full PW Consulting study provides the downloadable models and segment-level forecasts you need to quantify trade-offs and run board-level scenarios. We intentionally withhold the granular segment tables and price-by-origin schedules here to preserve the integrity of that actionable dataset.

2026 will be a year where tactical agility and strategic selectivity pay off. Companies that align contracting structures, technical capability investments and regulatory monitoring will protect margins and capture disproportionate share gains as markets normalize. If your 2026 plans include capacity moves, major long-term contracts, or M&A activity, use the full report’s plant-level economics and scenario models as the evidentiary backbone of your decision memo.

Access the full Atomized Ferrosilicon Market study to obtain the detailed segment outputs, plant-level cost curves, vendor scorecards and interactive scenario tools referenced in this preview. PW Consulting can also deliver a tailored executive workshop to convert these insights into an operational 90–180 day plan that aligns procurement, commercial and technical stakeholders.

For detailed analysis of this topic, please visit the official page:Atomized Ferrosilicon Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com