Moulding Equipment Market — Strategic Briefing for 2026 Decision-Makers

Executive snapshot

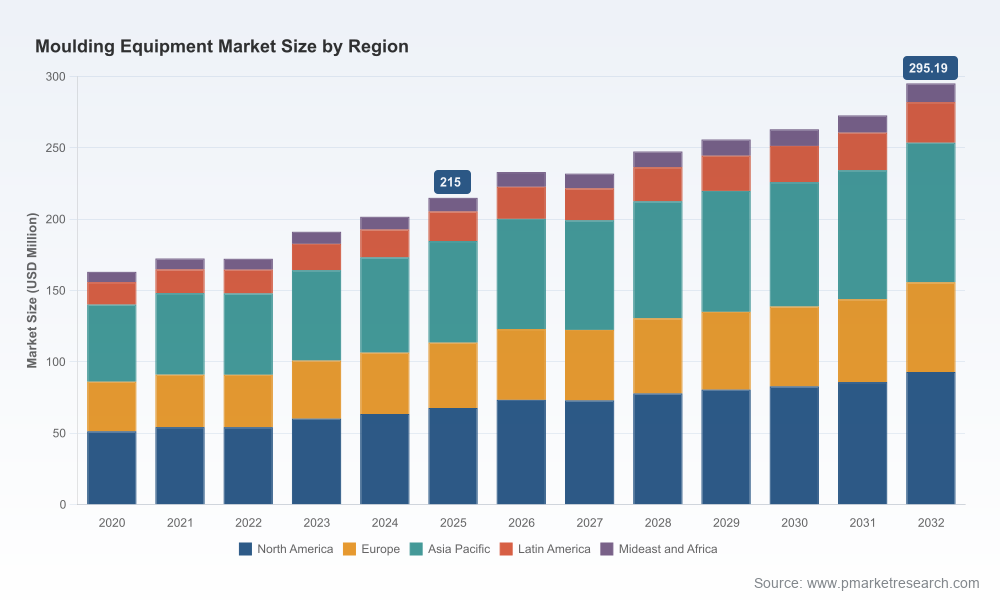

As PW Consulting’s lead industry analyst, I present a concise strategic orientation to the Moulding Equipment Market that links current realities to near‑term choices. Our proprietary modelling—anchored on a 2025 base year and a 2026–2032 forecast horizon—shows the market expanding from approximately USD 215.0 Million in 2025 to a projected USD 295.19 Million by 2032, at a compound annual growth rate (CAGR) of 4.8%. The trajectory is evidence of steady demand growth tempered by episodic operational and input‑price headwinds. Market concentration is meaningful: the three largest vendors account for a majority share of revenues, and the top five firms capture roughly two‑thirds of the market, shaping competitive dynamics, supplier leverage and consolidation risk.

Moulding Equipment Market

Why this briefing matters for 2026 decisions

- Transition timing: 2026 is a pivot year. Buyers, OEMs and investors must decide whether to accelerate migration to low‑energy, high‑automation platforms or to extend life of legacy assets under tight cost constraints.

- Investment discipline: capital allocation choices made in 2026 will influence cost structures and competitiveness through the 2030s—affecting unit economics more than short‑term demand fluctuations.

- Supply chain resilience: volatile polymer feedstock pricing and localized energy policies mean procurement strategies and inventory policies adopted in 2026 will materially affect manufacturing margin variability into 2028 and beyond.

Market trajectory and what the numbers reveal

The market grew from roughly USD 163.15 Million in 2020 to USD 215.0 Million in 2025, reflecting recovery and investment cycles following pandemic disruptions, broader industrial automation adoption, and incremental productivity gains in plastics and rubber processing. Our base‑case forecast anticipates continued expansion at a 4.8% CAGR over 2026–2032, with a non‑linear path: an initial uplift in 2026 driven by fleet refresh initiatives, a modest normalization in 2027 as retrofit projects complete, and sustained growth thereafter as automation and electrification projects scale.

Moulding Equipment Market

Interpreting these figures for 2026: purchasers and capital allocators should expect a market that is large enough to justify strategic investments but concentrated enough to require selective partnership strategies. The top vendors’ combined market power elevates the importance of supplier negotiation, service bundling and aftermarket strategies.

Moulding Equipment Market

Key market dynamics shaping 2026 strategy

- Energy and regulation: Rising energy costs—especially in Europe—and emissions and efficiency regulations are prompting a measurable shift toward high‑precision, low‑energy‑consumption platforms. All‑electric and advanced servo‑hydraulic systems are delivering rapid ROI in many use cases, and energy efficiency will increasingly be a primary procurement criterion.

- Raw material volatility: Polymer and resin prices remain correlated with crude oil and natural gas markets. This creates margin squeeze episodes and increases the value of flexible production architectures that can switch grades or products without lengthy retooling.

- Labor and automation: Increasing labor costs in precision manufacturing are accelerating adoption of integrated robotics and advanced process control. Firms that implement automation to improve repeatability and reduce per‑unit labour content gain a durable cost advantage.

- Concentration and consolidation: The market’s CR3/CR5 profile suggests a landscape where leading OEMs can set technical and commercial terms, but opportunities exist for niche players to win on specialization—e.g., rubber injection systems or vertical machines with integrated automation for specialized applications.

What the full report delivers — practical, decision‑ready tools

PW Consulting’s full Moulding Equipment Market report is built to move beyond descriptive analysis to actionable decision support. Highlights include:

- Investment playbooks: Capex vs. retrofit decision frameworks with payback windows under alternative energy‑price scenarios.

- Total cost of ownership (TCO) models: Configurable calculators that factor equipment acquisition, energy, maintenance, labour and tooling turnover to support vendor selection and lifecycle budgeting.

- Technology adoption roadmap: Milestone‑based guides for migrating from hydraulic to servo‑hydraulic and all‑electric platforms, including automation integration sequencing and expected productivity lift curves.

- Procurement and supplier playbook: Negotiation levers, service‑level structuring, spare‑parts pooling and warranty tradeoffs tailored to differing fleet strategies (centralized vs. distributed manufacturing).

- Scenario planning modules: Demand stress tests driven by polymer price shocks, regulatory tightening on energy use, and labor disruption—each connected to recommended mitigation options.

- Market entry and M&A screening tools: Shortlists and financial templates to evaluate partnerships, acquisitions and greenfield plays, calibrated to the market’s concentration dynamics.

Competitive landscape — profiles and strategic implications

The market is defined by a mix of global full‑line OEMs and regional specialists. Knowing who does what—and how they position their technical value proposition—matters for procurement and partnership strategy. Below are concise strategic reads on key competitors covered in the report.

- Arburg GmbH + Co. KG (Loßburg, Germany): Arburg’s ALLROUNDER TREND series emphasizes oil‑free, all‑electric drives, modularity and rapid set‑up. Strategic implication: strong option for manufacturers prioritizing energy efficiency and modular fleet strategies. Arburg’s intuitive interfaces lower training thresholds—valuable for multi‑site rollouts.

- Negri Bossi S.p.A. (San Maurizio Canavese, Italy): Focused on high‑efficiency servo‑driven machines and integrated robotics, with strengths in food, cosmetics and medical segments. Strategic implication: well‑suited to firms requiring high‑precision, hygiene‑compliant systems and end‑to‑end automation.

- DESMA Schuhmaschinen GmbH (Oberderdingen, Germany): Specialized in rubber injection systems and end‑to‑end solutions for North American markets. Strategic implication: attractive partner for rubber‑centric production lines and for buyers who value domestic servicing and localized engineering support.

- ENGEL Machinery Inc. (Schwertberg, Austria — North American ops): Known for economical two‑platen solutions that combine energy efficiency and short cycle times for large shot weights. Strategic implication: compelling where large‑part repeatability and floor space efficiency are priorities; recent trade show activity underscores continued product refinement.

- Haitian International Holdings Limited (Ningbo, China): Offers servo‑hydraulic and all‑electric platforms aimed at high‑volume production. Strategic implication: price/performance leader for scale manufacturing; buyers must balance acquisition cost advantages against service and spare‑parts footprint considerations.

- Yuhdak Machinery Co., Ltd. (Taiwan): Specialist in vertical injection solutions with automation and labour‑saving features targeted at rubber and thermoplastics applications. Strategic implication: niche play for precision vertical processes and highly automated cell designs.

Two recent market signals bear watching: ENGEL’s presentation of high‑efficiency two‑platen solutions at Plastindia 2026 and Negri Bossi’s unveiling of next‑generation servo‑driven machines with integrated robotics at PLAST 2026. Both moves validate the acceleration toward energy‑efficient, automation‑ready platforms and reinforce OEM competition along technology and system integration vectors.

Strategic priorities for leaders in 2026

- Manufacturers (OEMs and large buyers): Prioritize hybrid fleet strategies—retain proven hydraulic assets for low‑capex needs while selectively investing in all‑electric/servo systems where energy, precision and automation deliver clear ROI.

- Mid‑sized converters and contract manufacturers: Use 2026 to standardize interfaces for robotics and Industry 4.0 telemetry to reduce OEE losses and accelerate changeover times; negotiate bundled service contracts to stabilize aftermarket costs.

- Investors and private equity: Focus deal screening on service‑led business models, regional service networks and software‑enabled aftermarket revenue streams that can improve margins in a moderately concentrated market.

- Suppliers and component makers: Build modular, upgradeable subsystems (drives, controls) that allow end users to incrementally improve energy performance without full‑machine replacement.

Concluding view and next steps

2026 is a year of choices. The macro path—steady growth at a mid‑single‑digit CAGR—creates room to invest, but the competitive and input‑price realities demand selectivity. Energy efficiency, automation readiness and a nuanced procurement stance will separate winners from laggards. PW Consulting’s full report provides the operational tools, vendor scorecards and scenario models required to convert these insights into executable 12–36 month plans.

To access the complete segmentation, vendor benchmarking, and the decision‑support templates referenced here, consult the full Moulding Equipment Market report on our website. The core datasets and the model workbooks are gated to ensure strategic confidentiality—contact our team for an executive briefing and tailored scenario runs for your business case.

For detailed analysis of this topic, please visit the official page:Moulding Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com