Liquid Crystal Polymers (LCPs) Market — Strategic Brief for 2026 Decision-Makers

Executive snapshot

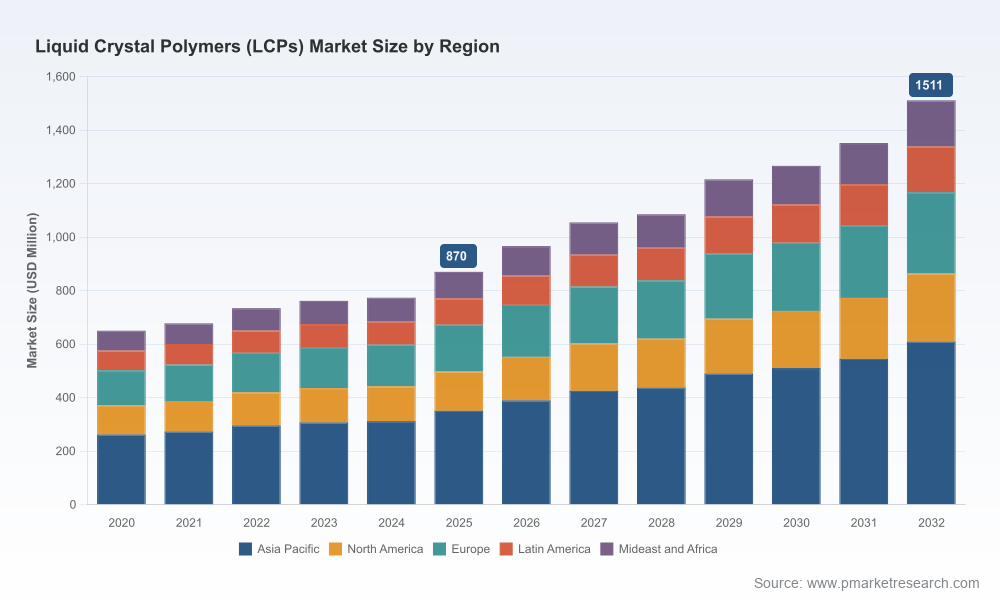

The Liquid Crystal Polymers (LCPs) market is transitioning from a component-driven niche into a broadly adopted engineering polymer class that underpins next‑generation RF, high‑speed interconnects, precision medical devices, and selected automotive applications. PW Consulting’s latest study uses a 2025 base year and a 2026–2032 forecast window to quantify this transition: the global market is projected to grow at a compound annual growth rate (CAGR) of approximately 8.31% through the forecast period. After a steady expansion from our historical window (2020–2025), our top‑line scenario shows continued acceleration as 5G/mmWave deployments, advanced semiconductor packaging, and design‑for‑miniaturization trends converge on LCPs’ combination of dielectric stability, high‑temperature performance and processing advantages.

Liquid Crystal Polymers (LCPs) Market

Why this study matters for 2026 corporate strategy

- Timing of supply and qualification decisions. Manufacturers and Tier‑1 buyers must align supplier certification, qualification cycles and inventory strategies with product roadmaps—decisions that made in 2026 will determine access to qualified low‑loss LCP grades for 2027–2029 product launches.

- Material substitution and cost-to-performance trade-offs. LCPs now compete directly with PA, PEEK and other high‑performance polymers on total system cost and cycle time; procurement and R&D teams need quantified comparisons, not qualitative claims.

- Sustainability and regulatory positioning. The emergence of biomass‑derived monomers and evolving IPC standards means sustainability credentials will increasingly influence supplier selection and customer acceptance in regulated segments.

Market trajectory and headline metrics

PW Consulting’s consolidated market model tracks the LCP industry from an established base in 2025 through material adoption curves across the 2026–2032 forecasting horizon. The model incorporates a historical series and forward scenarios that account for product lifecycle timing, supplier capacity additions, and demand multipliers from ICT, automotive and medical applications. The top‑line view shows the market expanding materially from the 2025 base, following the stated CAGR and culminating in a materially larger market by the end of the forecast period.

Liquid Crystal Polymers (LCPs) Market

Concentration metrics underline a moderately consolidated supplier landscape: the three‑firm concentration (CR3) is in the mid‑40s percentile, while the five‑firm concentration (CR5) sits in the mid‑60s percentile. That structure implies a healthy balance—leading vendors retain price and technology influence, while second‑tier suppliers can still capture niche and localized demand through specialization or capacity investments.

Liquid Crystal Polymers (LCPs) Market

Structural dynamics shaping 2026 decisions

- Technology drivers. LCPs’ dielectric stability and low loss tangent across broad frequency and temperature ranges are central to mmWave antenna‑in‑package and high‑frequency connector designs. IPC‑level dielectric specifications are increasingly influencing material selection for RF and high‑speed modules.

- Processing and design advantages. Thin‑wall injection molding and high‑flow LCP grades enable smaller, more integrated assemblies with shorter cycle times compared to many high‑temperature alternatives—an important lever for high‑volume electronics and medical micro‑components.

- Supply chain and material sourcing. Recent moves to commercialize biomass‑derived monomers and localized capacity licenses are altering the supplier map. Buyers must weigh sustainability credentials against qualification risk and time‑to‑market.

- Regulatory and qualification regimes. Standards and customer certification cycles—particularly for RF dielectrics and medical implants—are gating factors. Buyers need to plan for multi‑stage validations that can exceed typical procurement lead times.

Competitive landscape — who matters and why

Four supplier archetypes dominate strategic conversations today: global integrated chemical producers with differentiated specialty LCP portfolios; Asia‑based specialty polymer houses with tight ties to electronics assemblers; regional compounders expanding capacity; and emerging entrants pursuing niche bio‑based or ultra‑high‑flow formulations.

- Celanese Corporation (Irving, Texas) — Strong position with Vectra® and Zenite® LCP grades, including medical‑grade variants. Their technical data sheets highlight dimensional stability after high‑temperature reflow and targeted performance in connectors and antenna components. Celanese is positioned as a go‑to supplier for customers demanding tight tolerances and established global support networks.

- Polyplastics Co., Ltd. (Tokyo) — Known for LAPEROS® grades optimized for high‑flow molding and precision electronics. Recent portfolio extensions emphasize improved flowability and heat resistance, making Polyplastics attractive to smartphone and miniaturized connector suppliers who prioritize manufacturability.

- Sumitomo Chemical Co., Ltd. (Tokyo) — Offers SUMIKASUPER™ LCP grades aimed at ICT and mobility solutions. Notably, Sumitomo announced a biomass‑based monomer program moving toward customer certification and commercial supply, positioning them early on sustainability claims for LCPs in regulated supply chains.

- Toray Industries, Inc. (Tokyo) — Supplies SIVERAS™ LCP resins with an emphasis on low‑warpage, high‑flow applications in electronics. Toray’s strength is integration across polymer technologies and close partnerships with manufacturing OEMs in East Asia.

Beyond these leaders, regional players are expanding capacity and securing safety certifications to serve localized demand—moves that materially affect lead‑times and price elasticity in specific geographies.

Recent industry moves to watch

- Sumitomo’s announced mass‑production route using a biomass‑sourced monomer, with customer certification targeted within the 2026–2027 timeframe, signals an inflection in how sustainability credentials will be operationalized for critical electronic components.

- Polyplastics’ product line expansion toward higher‑flow and higher‑temperature grades targets the next wave of smartphone and precision connector designs that prioritize rapid mold fill without sacrificing dielectric performance.

- Regional capacity licensing and facility certifications—illustrated by recent domestic production permits—are reducing logistics friction in certain markets and tightening competitive dynamics for high‑frequency and 5G‑grade LCPs.

What the PW Consulting report contains — practical, executable components

Our full study is designed as a decision support system for procurement, R&D, strategy and corporate development teams contemplating actions in 2026. Key deliverables include:

- Top‑down and bottom‑up market sizing with transparent modeling assumptions and sensitivity cases (including upside/downside adoption curves driven by 5G rollout and semiconductor packaging cycles).

- Segmentation by region and application with demand drivers, price trends and margin impact—presented in a way that supports scenario planning and negotiations with suppliers.

- Supplier scorecards and capability matrices that evaluate technology roadmaps, capacity timing, qualification behavior and sustainability credentials.

- Go‑to‑market playbooks for material users: qualification checklists, sample acceptance workflows, and a risk‑weighted supplier selection framework tailored to LCP specificities (e.g., dielectric performance, dimensional stability after reflow, thin‑wall processability).

- Technical annexes summarizing critical benchmarks—such as dielectric constant and loss tangent expectations for RF film applications and dimensional stability tolerances after high‑temperature reflow—to expedite engineering trade studies.

- Regulatory and standards mapping, highlighting IPC and other relevant specifications that commonly govern supplier acceptance for RF and high‑frequency assemblies.

Actionable playbook for 2026

- Immediate (next 3 months): Map product roadmaps against certification timelines. Prioritize suppliers with available certified grades for your target applications, and open dual‑track qualification with at least one incumbent and one challenger to manage supply risk.

- Mid‑term (3–12 months): Invest in co‑development trials for high‑flow or bio‑based grades that align with product sustainability targets. Require supplier disclosure of qualification milestones and long‑lead raw material sourcing plans.

- Strategic (12–36 months): Consider capacity partnerships or offtake arrangements where scale economics and front‑loaded qualification cycles are a barrier. Use modeling outputs to stress‑test cost curves under different adoption and price scenarios.

Risks, uncertainties and scenario levers

Key risks include delays in certification of bio‑based monomers, localized capacity constraints in critical regions, and shifts in IPC or customer specifications that increase engineering overhead for material change. Our sensitivity analyses show that demand shocks from either a slower 5G device replacement cycle or a delay in advanced packaging adoption materially change supplier leverage and price trajectories. PW Consulting’s full model allows clients to run custom scenarios against these levers.

How to use the full PW Consulting report

This brief demonstrates the report’s strategic value without disclosing the granular split‑outs that many clients use as competitive intelligence. The full report provides the detailed regional and application segmentation, supplier market shares and downloadable financial models required to make contracted procurement decisions and M&A assessments in 2026. If your team is preparing supplier negotiations, qualification plans or product redesign roadmaps, the model, scorecards and technical annexes will shorten decision cycles and reduce execution risk.

Conclusion

For corporate leaders making 2026 choices, the LCP market represents both an operational challenge and a strategic opportunity. The technology’s unique combination of dielectric performance and processability places it at the intersection of multiple growth vectors—communications, high‑speed connectivity, and precision medical components—while supplier dynamics and sustainability transitions are reshaping the practical choices available to buyers. PW Consulting’s study equips decision‑makers with the scenario tools, supplier intelligence and technical benchmarks needed to move from reactive procurement to proactive value capture. To access the full data, segmentation tables and the interactive forecast model, please refer to our report page.

For detailed analysis of this topic, please visit the official page:Liquid Crystal Polymers (LCPs) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com