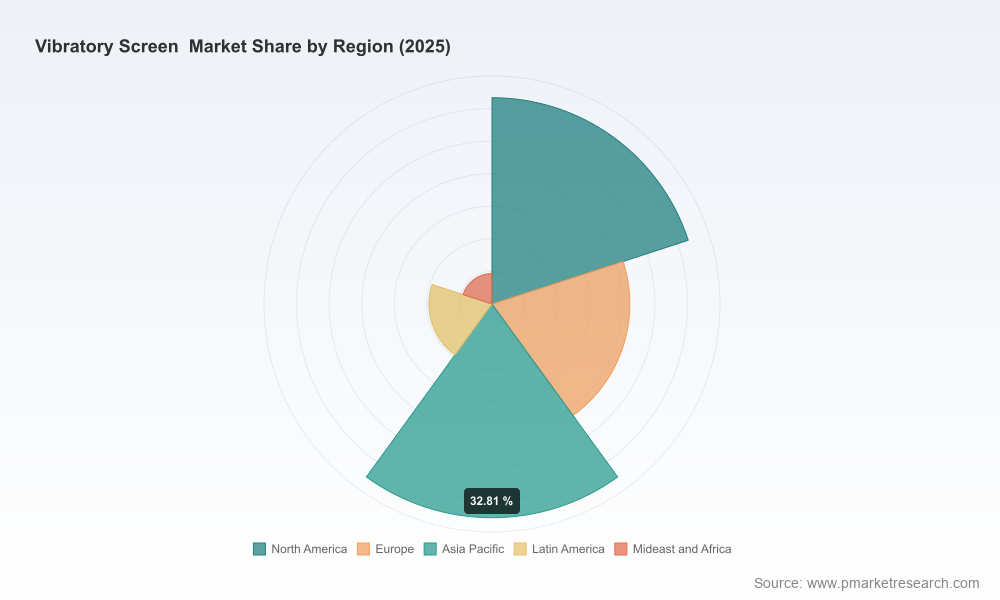

Vibratory Screen Market — 2026 Strategic Outlook and Executive Primer

As companies recalibrate capital allocation and product roadmaps for 2026, the vibratory screen market presents a nuanced growth story: steady expansion, pockets of technological disruption, and a competitive landscape that rewards operational excellence and aftermarket capture. This primer from PW Consulting synthesizes the headline intelligence from our full market study to equip senior executives and investment committees with the strategic questions and decision framework they need — while reserving the granular segmentation and proprietary tables for subscribers and clients.

Vibratory Screen Market

Market snapshot: growth trajectory and structural signal

Using 2025 as the base year, our model identifies sustained mid-single-digit expansion across the forecast window. The global market reached a meaningful milestone in 2025 and, under the central-case assumptions, is projected to grow at a 7.0% compound annual growth rate through 2032. By the end of the forecast horizon the market reaches a materially larger scale, reflecting continued demand from heavy industries, construction activity and recycling-driven retrofit cycles.

Vibratory Screen Market

Two macro structural signals matter most to strategists:

Vibratory Screen Market

- Fragmentation at the supplier level: market concentration remains modest, with the top-three and top-five supplier groups accounting for under a third of total revenue — a structural feature that sustains pricing variability and carve-out opportunities for focused players.

- Resilience and cyclicality: while the market shows signs of cyclical sensitivity to mining and construction activity, it has demonstrated resilience vis-à-vis recent regulatory and sustainability-driven investment cycles that are supporting replacement and higher-spec equipment purchases.

Why this matters for 2026 decision-making

For executives charting 12–36 month plans, three strategic imperatives emerge from our analysis:

- Prioritize aftermarket and service economics. Given the installed base dynamics and the technical specificity of screening media and wear parts, aftermarket revenue is a high-margin lever that can materially change return-on-investment math for equipment manufacturers and distributors.

- Differentiate via technology that addresses regulatory and operating cost pressures. Equipment that demonstrably reduces energy use, waste, or water consumption is winning specification battles in environmentally constrained projects and public tenders.

- Choose deployment pathways—organic vs M&A—based on targeted capability gaps rather than scale alone. With the market only modestly concentrated, bolt-on acquisitions that fill gaps in digital monitoring, specialized media, or regional service networks can accelerate share gains faster than broad-spectrum roll-ups.

Operationally actionable insights — what to do in the next 6–18 months

- CapEx and product roadmap: Reallocate a higher share of R&D to screening media longevity, modular retrofit kits (to convert older machines to higher-efficiency profiles), and to embedded sensors for predictive maintenance. Prioritize pilot projects that reduce total cost of ownership (TCO) rather than just unit price.

- Aftermarket and spares strategy: Map the installed base in priority end-markets, establish tiered service contracts, and create “parts-as-a-service” bundles. Evaluate deferred revenue models that convert equipment sales into recurring streams through consumables and uptime guarantees.

- Supply chain resilience: Hedge exposure to single-source mechanical components and control for lead-time variability by qualifying redundant suppliers for bearings, motors and elastomeric mounts. Build a critical-parts stocking strategy linked to customer uptime SLAs.

- Commercial and pricing playbook: Implement value-based pricing for retrofit and specialty screens; use outcome-based contracts for high-availability customers; and pilot dynamic pricing for spare parts informed by usage telemetry.

- Regulatory and sustainability programs: Obtain or validate environmental performance claims (energy, water, emissions) for key product lines to strengthen bids for infrastructure projects and to comply with tightening sector regulations introduced in 2025.

What the full report contains (practitioner-focused)

Our complete study is structured to be immediately operational for commercial, product and M&A teams. It includes:

- Transparent market sizing model (historical 2020–2025 and base-year 2025) with scenario-based forecasts to 2032, including sensitivity to commodity cycles and regulatory adoption curves.

- Commercial playbooks for OEMs, aftermarket specialists and distributors — detailing pricing benchmarks, negotiation levers, and channel economics.

- Competitive benchmarking and capability matrices that map suppliers against technical attributes (e.g., motion type, screening media, modularity), service footprint, and digital maturity.

- Technology and innovation tracker — IP landscape, emerging materials, and sensor ecosystems — with guidance on licensing, partnerships and in-house development thresholds.

- Deal-screening templates and valuation impact worksheets for bolt-on acquisitions or greenfield investments in service networks and production capacity.

- Regulatory impact matrix and a sustainability playbook that quantifies near-term compliance risks and identifies product enhancements that unlock tenders.

Competitive landscape — what to watch and where opportunities lie

The sector is populated by a mix of legacy engineering specialists, global mining-cap equipment suppliers, and nimble niche players focused on sanitary or high-efficiency screening. Key archetypes include:

- Technology-focused OEMs with patented motion profiles — companies that leverage proprietary kinematics and screening mechanisms to win sector-specific specifications in food, pharma and minerals.

- Mining and aggregates heavyweights — established suppliers that offer end-to-end processing solutions and compete on scale, multi-type screen platforms and dewatering capabilities.

- Regional specialists and system integrators — firms that excel at local service, customization and parts support, often enabling premium aftermarket margins.

Representative players highlighted in our study include established gyratory and circular motion specialists, heavy-duty mining equipment manufacturers, and regional engineering houses with strong pulp-and-paper or sanitary screening pedigrees. Recent industry activity — including significant product introductions and high-profile exhibitions during 2026 — underscores the emphasis on advanced screen media and thermal/abrasion-resistant solutions as differentiators. Executives should monitor both product commercialization and field trial outcomes closely, as these will determine specification shifts in major tenders.

Regulation, infrastructure and sustainability — the non-negotiables

Regulatory tightening enacted in 2025 has been a clear accelerant for higher-specification equipment purchases. Two practical consequences to embed in 2026 planning:

- Procurement teams increasingly demand documented reductions in waste generation and energy intensity from screening equipment as prerequisites for inclusion in public and large private tenders.

- Infrastructure projects and mine rehabilitation programs are prioritizing solutions that lower lifecycle environmental costs, creating a premium niche for certified low-waste, low-energy screens.

Companies that can demonstrate quantifiable environmental benefits and provide lifecycle service commitments will win share in the next procurement cycle.

Decision framework and KPIs for 2026 executives

Adopt a simple, four-point decision lens for capital allocation and commercial focus:

- Strategic fit: Does the initiative increase recurring revenue (service/parts/digital) or materially shorten time-to-specification for high-value tenders?

- Value capture: What margin and cash-flow uplift can be expected within 12–24 months — and what is the payback on R&D or M&A spends?

- Customer impact: Does the solution measurably reduce TCO for priority customer segments (e.g., mining, construction, recycling)?

- Execution risk: Are supplier, regulatory and aftermarket capabilities sufficient to scale the solution without unacceptable service disruptions?

Recommended KPIs to track real-time include installed-base utilization, parts attach rate, mean time-to-repair, retrofit conversion rate, and percentage of new orders specifying sustainability-enhanced configurations.

Where M&A and partnerships make sense

Given the modest top-end concentration, inorganic strategies should be selective:

- Bolt-ons that add regional service networks or specialty screening media capabilities can deliver rapid margin expansion.

- Minority investments or licensing deals with sensor/software vendors accelerate digital monitoring without the full cost of in-house development.

- Strategic partnerships with local integrators smooth entry into regulated infrastructure projects where local compliance and service are decisive.

Final note — the value of the full PW Consulting study

This executive primer surfaces the strategic themes and immediate actions we believe will define winners and laggards in 2026. For procurement teams, product leaders and investors seeking the empirical basis to underpin decisions — including granular regional and application splits, supplier share matrices, price trends and detailed scenario outputs — the full report provides the data, templates and decision tools to mobilize execution. Access to the complete dataset and proprietary segmentation is the next step for teams wanting to convert this strategic insight into prioritized programs and quantified investment cases.

For detailed analysis of this topic, please visit the official page:Vibratory Screen Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com