Outdoor Gear Market 2026: Strategic Imperatives from PW Consulting

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present a focused executive introduction to our latest Outdoor Gear Market study — a practical, decision-oriented guide designed for leadership teams planning for 2026 and beyond. This preview surfaces the structural forces, competitive battlegrounds, and near-term tactical moves you must consider. To protect the value of our proprietary segmentation and scenario outputs we intentionally withhold granular splits in this summary; the full report contains the data tables, heat maps, and models that will convert insight into executable plans.

Outdoor Gear Market

Big-picture market context

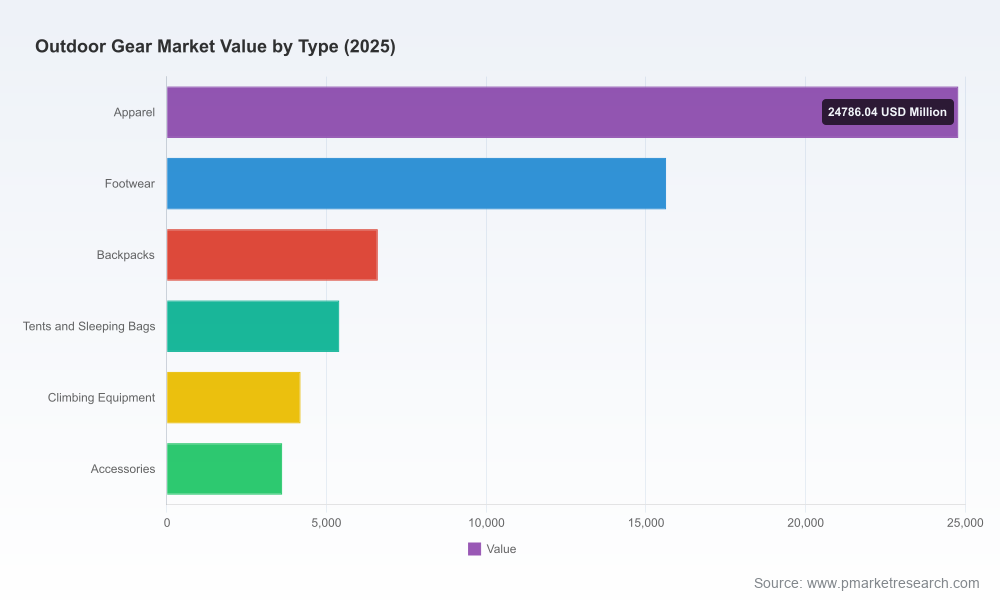

Using 2025 as the base year and a historical window from 2020–2025, the global outdoor gear market has expanded materially: total industry revenue rose from approximately USD 44,635 Million in 2020 to roughly USD 60,225 Million in 2025. Looking forward across our 2026–2032 forecast horizon, we model a compound annual growth rate (CAGR) of 4.44%, with market size tracking toward roughly USD 81,521 Million by 2032 under our central scenario. These top-line dynamics frame both margin opportunities and execution risks for incumbent brands, retail platforms, and new entrants alike.

Outdoor Gear Market

Report scope: what the full study delivers

- Robust market-sizing and a transparent methodology (historical reconciliation, addressable market definitions, channel overlays).

- Scenario-led forecasts through 2032 with upside/downside sensitivity to macro drivers (consumer discretionary spend, travel & tourism recovery, raw material cost shocks, and regulatory shifts).

- Actionable go-to-market playbooks for premium, mass, and value segments — including assortment, pricing, and promotional levers mapped to channel economics.

- Supply-chain stress-testing and cost-to-serve models that quantify tariff and input-cost pass-through across supplier networks.

- Competitive heat maps, capability benchmarking, and a prioritized M&A/opportunity pipeline for strategic buyers and PE sponsors.

- Regulatory and product-safety intelligence — compliance action plans for PFAS bans, emissions rules, and evolving excise tax frameworks.

- Commercial pilots and circular-economy blueprints for resale, repair, and certification programs that capture lifetime value.

Dynamics shaping 2026 decisions

- Policy and trade volatility: Incremental tariffs introduced in 2025 have already raised landed costs for many outdoor products, squeezing gross margins especially for brands with concentrated import exposure. Expect margin pressure to persist unless supply chains are rebalanced or pricing power is strengthened.

- Regulatory substitution of materials: State-level PFAS restrictions (effective in high-value jurisdictions) are accelerating material innovation and supplier qualification cycles. Brands that moved early to validated recycled and bio-based inputs are now avoiding compliance bottlenecks and benefiting from claim-based premiumization.

- Product safety and reputation risk: High-visibility recalls in 2025 highlighted the financial and reputational downside of inadequate upstream quality control. Investment in testing, traceability, and post-sale remediation reduces tail risk and protects brand equity.

- New retail and circular models: Leading retailers are piloting resale and repair formats to extend product lifecycles and capture secondhand flows. Certification programs for used equipment are emerging as a credibility tool for the pre-owned market segment.

- Category convergence: Electrification (e-bikes), multi-sport crossovers, and lifestyle-driven apparel are shifting where value accumulates — from single-purpose hardware to services, membership models, and distinctive experiences.

Competitive landscape — strategic reads on the majors

The market’s concentration profile is meaningful but not prohibitive: the top three firms account for a material minority of sales, while the top five approach half of industry revenue — a structure that creates scale advantages but leaves room for differentiated challengers. This dynamic supports both category consolidation and targeted bolt-on M&A plays.

Outdoor Gear Market

- Columbia Sportswear Company: Deep distribution and broad product architecture make Columbia a resilient volume player. Their core strength is value-engineered, seasonally refreshed apparel and footwear. Strategic priority: tighten direct-to-consumer economics and accelerate low-carbon material roadmaps to protect margins and premiumization potential.

- YETI Holdings, Inc.: YETI’s premiumization of functional accessories shows how brand storytelling can elevate commoditized items. Exposure to tariffs and imported hardware costs is a current vulnerability — hedging through diversified sourcing or localized manufacturing will matter for margin protection.

- Fenix Outdoor International AG: A portfolio of heritage European brands emphasizes technical light-weighting and niche specialty appeal. Their route-to-market through selective retail networks supports margin but may need broader DTC acceleration in North America and Asia.

- V.F. Corporation / The North Face: The North Face remains the anchor performance brand in high-end mountain sports. VF’s playbook combines technological leadership with scale — but balancing wholesale partners and DTC growth is an ongoing execution challenge.

- Patagonia, REI, Rocky Brands, Duluth Holdings: These players illustrate different strategic archetypes — sustainability-first premium positioning (Patagonia), membership and community-driven retail (REI), durability-led footwear (Rocky), and workwear-crossover lifestyle (Duluth). Each has a distinct proposition that can be either a competitive moat or a scaling constraint depending on capital allocation and channel mix decisions.

Strategic implications for 2026 planning

Companies that treat 2026 as a year of strategic recalibration — not merely a continuation of pre-2025 playbooks — will preserve margin and create optionality. The report prioritizes the following near-term actions:

- Supply-chain resilience and tariff mitigation: Map supplier concentration, test alternative routing, and model price elasticity to determine optimal pass-through strategies by channel and product tier.

- Materials transition program: Fast-track PFAS substitutes and certified recycled fibers with dual tracks for product redesign and supplier qualification to shorten lead times.

- Circular commerce pilots: Launch certified resale, repair, and trade-in pilots aligned with brand positioning to recover margin from secondhand flows and increase lifetime customer value.

- Category portfolio optimization: Use SKU analytics to identify low-ROI SKUs (by channel) for rationalization and redirect capital to high-growth, high-margin micro-categories such as technical outerwear and performance accessories.

- Risk-averse product safety governance: Implement upstream testing checkpoints and digital traceability to reduce recall frequency and speed head-off remediation costs.

- M&A and partnership playbook: Prioritize bolt-ons that add supply-chain control, direct-to-consumer capability, or sustainability technology. Consider strategic minority investments in circular platforms and certification providers (e.g., used-equip certification).

How this study changes decision-making

Leaders need three things from market intelligence in 2026: defensible numbers, scenario-tested options, and executable next steps. Our study supplies all three. Rather than provide an exhaustive catalogue of segment percentages in this teaser, we offer the analytical levers that materially move P&L and strategic outcomes:

- Quantified tariff and input-cost scenarios linked to margin waterfalls and pricing strategies.

- Channel-level unit economics for brick-and-mortar, wholesale, DTC and resale so leaders can reallocate go-to-market spend quickly.

- Regulatory playbooks that translate PFAS, emissions, and excise tax changes into concrete product, sourcing and labeling requirements.

- Priority M&A target profiles and integration checklists to accelerate near-term consolidation without overpayment risk.

Final note — why the granular data matters

High-level trends are necessary to set strategy, but transaction-level and segment-level granularity is what drives investment memoranda, SKU-level assortment decisions, and supplier re-contracting. Our full report includes the proprietary segmentations, channel matrices, price elasticity matrices, and buyer-persona workstreams that enable you to translate the strategic pivots above into board-ready plans and 2026 operating targets.

To access the complete dataset, scenario models, and executable playbooks — including our prioritized list of M&A targets, heat maps by sub-category, and supplier risk scores — please consult the full PW Consulting Outdoor Gear Market report on our website.

For detailed analysis of this topic, please visit the official page:Outdoor Gear Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com