EMC Shielding and Test Equipment Market Size, Share, and Growth Opportunities

Other |

2026-06-03 12:08:11

PW Consulting’s latest market study on 5‑Aminolevulinic Acid Hydrochloride (5‑ALA HCl) synthesizes five years of historical performance and a seven‑year forecast into an actionable briefing tailored for executive teams, corporate strategy groups, corporate development, and investors preparing for 2026. Anchored to a 2025 base year and a modeled forecast through 2032, the study quantifies the market trajectory (CAGR: 7.32%) and maps the structural drivers that will determine commercial winners and losers across pharmaceutical, clinical, agricultural and specialty end‑uses.

5-Aminolevulinic Acid Hydrochloride Market

Data‑grounded timing. The market expanded from about USD 40.3 Million in 2020 to USD 57.4 Million in 2025, and our forecast trajectory anticipates continued expansion to roughly USD 94.6 Million by 2032. These levels and growth rates are material for capex scheduling, supply commitments, and pricing strategies as companies reset production and commercial plans for the mid‑decade.

5-Aminolevulinic Acid Hydrochloride Market

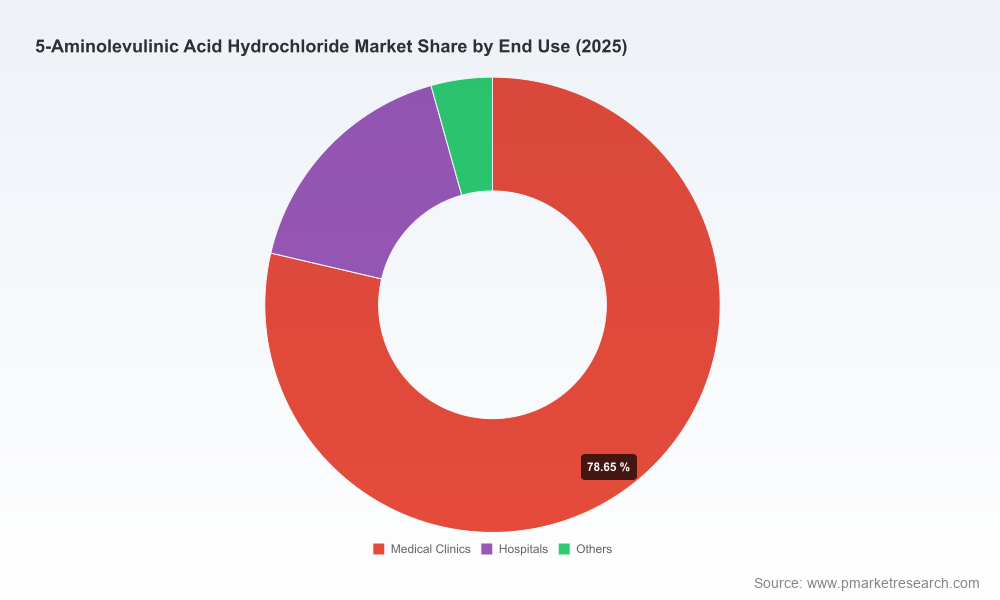

Cross‑sector inflection points. 5‑ALA HCl sits at the intersection of clinical photodynamic therapy (PDT), neurosurgical fluorescence guidance, dermato‑cosmetic opportunities, and agricultural biostimulants. The breadth of demand profiles creates both hedging and specialization opportunities — and requires a distinct go‑to‑market posture for each channel.

5-Aminolevulinic Acid Hydrochloride Market

Regulatory and reimbursement rhythms. Recent and legacy regulatory milestones (including an established EMA authorization pathway for certain neurosurgical uses) and localized reimbursement mechanisms (e.g., special access channels) materially influence product adoption curves; integrating these rhythms into commercial planning is a core deliverable of the report.

Market model and scenario engine: deterministic and sensitivity scenarios calibrated to historical 2020–2025 data and extending across a 2026–2032 forecast window. The model is built in modular form to let strategy teams test pricing shocks, capacity constraints, and regulatory outcomes.

Supply‑side mapping: global supplier matrix with capability profiling (clinical vs. research vs. agricultural grades), regulatory dossiers (including flagged USDMF filings), manufacturing footprints, and recent capacity moves. The mapping highlights single‑point risks, long‑lead vendors, and potential contract manufacturing partners.

Demand segmentation playbooks: commercial roadmaps for each major end‑use (clinical PDT, neurosurgical fluorescence guidance, compounding, and crop biostimulants), including recommended product specifications, pricing architecture, channel priorities, and physician/agronomist engagement strategies.

Regulatory tracker and reimbursement playbook: timelines and decision points for submitting marketing dossiers, leveraging special access or compassionate‑use mechanisms, and aligning clinical development assets to reimbursement windows in key jurisdictions.

M&A and partnership shortlists: target prioritization framework combining technological fit, regulatory position, capacity footprint, and customer access — built to accelerate due diligence in 2026.

Operational checklists: supplier audit templates, quality assurance gating criteria for pharmaceutical vs. agricultural grades, and SKU rationalization frameworks to optimize working capital and reduce obsolescence.

Growth concentrated, but opportunity broad. Despite robust aggregate growth (7.32% CAGR projected 2026–2032), the market shows a mixed concentration profile: the top three firms account for about one quarter of market share and the top five for roughly thirty percent. This fragmentation signals accessible opportunities for new entrants that can differentiate on regulatory filings, consistent high‑purity production, or integrated clinical partnerships.

Purity and regulatory status are primary differentiators. Firms positioning for pharmaceutical and clinical channels must prioritize high‑purity manufacturing controls and global dossier readiness (e.g., USDMF/DMF listings). The report outlines the technical gating factors and QC parameters buyers will insist on in tender and bilateral contracting processes.

Supply cadence and capacity rhythm create tactical windows. Recent corporate moves — including announced capacity expansions and product launches by major chemical and pharmaceutical firms — indicate a step‑change in available supply. Meanwhile, certain manufacturers exhibit multiyear production rhythms that can create intermittent supply tightness, which in turn enables opportunistic pricing or long‑term offtake negotiations. The full study models several timing scenarios to guide contract length and safety stock decisions.

Raw material economics compress commercial risk. Glycine is a low‑cost primary feedstock in established synthetic routes. That input‑level affordability does not eliminate margin pressure — regulatory compliance, quality testing and specialized downstream processing drive cost differences across grades. The report includes a cost‑build that differentiates commoditized biochemical production from regulated pharmaceutical API pathways.

New applications and adjacent markets are material upside. Recent announcements — spanning agricultural biostimulants to cosmetic formulations — point to emerging demand vectors outside traditional clinical use. These adjacencies can meaningfully augment topline for suppliers willing to develop tailored formulations, distribution networks and regulatory strategies.

Established API players with regulatory pedigree hold a privileged position for clinical supply. Several European, Japanese and Chinese manufacturers currently supply pharmaceutical‑grade 5‑ALA HCl and some have active dossier filings in major markets. These firms remain the primary commercial partners for drug developers and hospitals needing reliable GMP supply.

Specialist product companies control clinical brand economics. Companies that market finished products containing 5‑ALA HCl for PDT and neurosurgery capture downstream value via product differentiation, physician education and reimbursement relationships. Their strategic play focuses on clinical evidence generation, label expansion, and geographic rollout rather than raw material cost leadership.

Compounding and research suppliers compete on speed and batch flexibility. Firms that cater to compounding pharmacies and research labs prioritize small‑batch agility and quick turnaround; they are attractive partners for early‑stage clinical programs but are limited by scaling and regulatory acceptance in pivotal trials.

Agricultural and cosmetic entrants require distinct go‑to‑market muscles. Chemical and crop‑science companies entering with bio‑stimulant or cosmetic formulations rely on channel relationships, formulation expertise and regulatory frameworks pertinent to their markets — a different playbook than pharmaceutical API supply.

Product launches that expand grade availability reduce merchant risk for buyers planning to scale clinical programs; firms should re‑assess supplier RFP timelines in light of these introductions.

Strategic partnerships between chemical majors and specialty formulators point to co‑development models that accelerate entry into cosmetic and agricultural channels — a potential template for firms seeking to diversify revenue.

Capacity expansions in Japan and elsewhere alter regional supply balances and may compress lead times; procurement teams should renegotiate supply‑security terms to convert timing improvements into cost or service advantages.

Regulatory and tender dynamics (including tariff considerations in certain public procurement systems) add transactional complexity for cross‑border procurement; aligning trade, regulatory and legal teams early reduces bid rejection risk.

API producers: Prioritize dossier filings in targeted jurisdictions, invest in GMP‑grade capacity, and offer tiered commercial agreements (clinical supply vs. bulk research). Use the report’s pricing and cost build to set sustainable long‑term contracts and avoid destructive spot pricing.

Pharma/medical device firms: Lock in multi‑year supply agreements with quality KPIs and step‑in rights for additional volumes. Align clinical development timelines with supplier capacity profiles and built‑in contingency sourcing.

Agribusiness and cosmetics players: Consider co‑development partnerships and pilot programs with established chemical manufacturers to accelerate regulatory acceptance and market trials while sharing R&D risk.

Private equity and strategics: Target consolidation plays around GMP‑capable assets and specialty product companies that own branded clinical channels. The fragmentation of supply creates acquisition arbitrage opportunities supported by the market’s projected growth.

Procurement and supply chain: Incorporate production cadence signals, tariff exposure and regulatory dossier completeness into supplier scorecards. The report provides an audit checklist and contract clause templates to safeguard supply continuity.

Scenario testing: Run your commercial and manufacturing plans through our modeled scenarios to quantify revenue, margin and working capital sensitivity to pricing, capacity and regulatory outcomes.

Diligence acceleration: Use the supplier matrix and regulatory tracker to shorten target screening and DD timelines, reducing time to term sheets in 2026 M&A processes.

Commercial alignment: Apply the demand segmentation playbooks to define GTM pilots that align clinical evidence staging with sales channel rollouts.

Our study couples a rigorous, transparent market model (historical 2020–2025 and forecast 2026–2032) with practical execution tools: supplier templates, regulatory roadmaps and M&A prioritization frameworks. We reveal the structural levers that matter to 2026 decision cycles — while reserving the granular subsegment allocations and underlying datasets for the full report to preserve the strategic exclusivity clients need when bidding, negotiating or acquiring.

To convert the macro trend (7.32% CAGR) and the documented growth pathway into defensible commercial advantage, the full study provides the ready‑to‑deploy models, supplier dossiers and contract language your teams need. Access to the complete dataset and our scenario workbook is available via the PW Consulting report portal.

For detailed analysis of this topic, please visit the official page:5-Aminolevulinic Acid Hydrochloride Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com