Where Is the Rheumatic Fever Market Heading with Improved Disease Management Strategies?

Networking |

2026-07-02 06:55:35

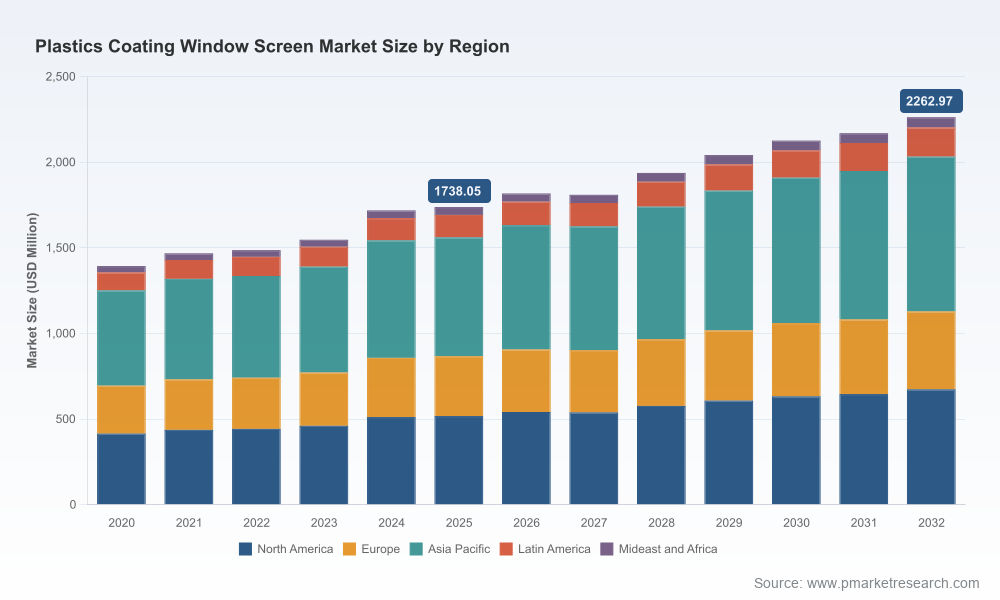

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I present a focused briefing that frames our full Plastics Coating Window Screen Market study as an operational roadmap for 2026 leadership choices. Built on a 2025 base and extended through 2032, the research situates decision-makers to act with confidence: the global market reached approximately USD 1,738 million in 2025 and is projected to grow at a mid-single-digit compound annual rate (CAGR) of 3.8% to roughly USD 2,263 million by 2032. This briefing demonstrates how that headline trajectory intersects with supply shocks, regulatory shifts and competitive manoeuvres — enough granularity to inform strategic priorities, while reserving the detailed segment-level tables and proprietary models for clients who access the full report.

Plastics Coating Window Screen Market

Actionable market timing: 2026 is a pivot year. The sector is no longer only driven by replacement cycles and low-cost surface treatments — innovation in coatings, weave technology and retractable systems now materially influence total addressable demand. Our study synthesizes demand drivers and timing so procurement, product and M&A teams can prioritize investments without waiting for lagging indicators.

Plastics Coating Window Screen Market

Cost-to-quality trade-offs under raw-material volatility: PVC resin and vinyl coating resin price movements in early 2026 materially shifted supplier cost models. The report quantifies exposure across manufacturing footprints and proposes hedging and sourcing strategies tailored to different business models (integrated manufacturers, OEM component suppliers and aftermarket specialists).

Plastics Coating Window Screen Market

Regulatory redesign of product spec: New REACH-compliant phthalate-free PVC formulations for the EU and tightened low-VOC requirements across North America are no longer hypothetical. The study maps compliance pathways, incremental cost estimates, and product re-spec timelines so product teams can prioritize reformulation vs. market withdrawal decisions.

Competitive positioning and concentration effects: With the market showing meaningful concentration at the top (CR3 and CR5 measures indicate a notably consolidated top tier), the study helps mid-market players identify white space and low-risk niches for profitable growth.

Our full report blends quantitative forecasting with tactical playbooks designed for executives, commercial leaders and engineers. The deliverables include:

Proprietary market-sizing and scenario models (base, upside and downside) that convert macro forecasts into product-level and channel-level demand curves — enabling rapid “what-if” evaluation of price, raw-material and regulatory shocks.

Segment maps (by region, coating type and application) with supplier cost-to-serve matrices and margin waterfall analyses. Note: this briefing intentionally does not publish segment share tables — they are detailed in the client report.

Supply-chain stress tests and sourcing playbooks, including shortlists of alternative resin suppliers, conversion contractors, and nearshore manufacturing partners to mitigate petrochemical volatility.

Regulatory compliance trackers: a jurisdiction-by-jurisdiction matrix of chemical, VOC and materials standards, with recommended timelines and CAPEX/OPEX implications for compliance and certification.

Commercial playbooks (pricing levers, channel expansion, retrofit programs) and product development roadmaps that align R&D, marketing and installation economics for measurable ROI within an 18–36 month horizon.

Interactive Excel models and sensitivity dashboards that translate high-level CAGR and market size into manufacturer- and SKU-level revenue scenarios.

The market is served by a mix of integrated window manufacturers, specialized mesh producers, and innovative systems suppliers. Key strategic archetypes and their implications:

Integrated OEM leaders (examples in the report): control over frame and screen systems enables product bundling, premium positioning and higher installed-value capture. These firms leverage brand, distribution and installation networks to push higher-margin, engineering-led offerings.

Mesh specialists and material innovators (examples in the report): firms focused on advanced coated meshes and tight-weave designs are where material differentiation occurs. Recent product launches have emphasized larger viewing spans and pet- or insect-resistant weaves — an important source of unit price resilience.

Systems and retractable solution providers: companies producing motorized or track-based retractables unlock retrofit demand and attract higher ASPs. Their growth underscores the need for OEMs to consider systems partnerships rather than single-component sourcing.

Low-cost global suppliers and regional specialists: these players dominate price-sensitive channels and aftermarket reefs. Their role in the value chain accelerates commoditization unless incumbent firms invest in product differentiation and certification-based premiuming.

Recent industry moves illustrate these dynamics: product expansions to wider-span viewing meshes, automated manufacturing investments to scale production, and a wave of certifications and reformulations to meet low-VOC and phthalate-free requirements. The full report documents these developments and provides a heatmap of capability gaps among leading competitors.

Two interlocking forces have reshaped short-term economics: commodity volatility and regulatory tightening. Early 2026 saw notable increases in PVC resin prices and in vinyl coating resin costs tied to crude and petrochemical constraints. For manufacturers this translates to margin compression or immediate price pass-through decisions; for product teams it raises questions about polymer substitution and reformulation budgets.

Regulatory drivers are equally impactful. The adoption of phthalate-free PVC formulations in the EU and stricter VOC ceilings for coatings in North America create dual pressures: elevated material costs and shortened certification lead-times. The study quantifies the compliance delta and sequences mitigation steps — for example, targeted reformulations for largest-volume SKUs, prioritized certification for export markets, and strategic reservoir stocking of compliant resins to smooth 2026 supply disruptions.

Base case: the market follows the reported CAGR of 3.8%, driven by steady replacement cycles, modest new-build uplift in select regions, and incremental premiumisation of mesh and systems.

Upside case: accelerated retrofit programs, faster adoption of premium retractable systems, and stabilization of resin prices lift growth materially above the base. This favours firms that can scale automated manufacturing and who have secured compliant formulations early.

Downside case: prolonged petrochemical shortages or fragmented regulatory barriers leading to product delistings. This scenario amplifies the need for flexible manufacturing, dual-sourcing and nimble pricing strategies.

Decision-makers should map current initiatives against these scenarios to identify three immediate moves: preserve margin with short-term hedges and inventory; accelerate certification and reformulation programs; and target product/channel interventions that protect installed-value.

CEO/CFO: Use the scenario models to stress-test cash flow and M&A screening matrices. Prioritize bolt-on targets that add either compliant-formulation capability or systems integration to accelerate aftermarket capture.

Head of Product/Engineering: Implement a two-track R&D schedule — compliant reformulations for regulated markets and premium material innovations for value capture. Leverage our cost-to-serve and margin waterfall templates to prioritize SKUs for reformulation.

Procurement/Supply Chain: Deploy the supplier risk heatmaps and hedging playbooks to redesign contracts and stocking policies. Evaluate automated manufacturing partners to offset labor and variability risks.

Commercial & Channel Heads: Adjust channel incentives to favor higher-margin systems and certified product lines. Use the retrofit playbooks to create targeted campaigns in markets with elevated retrofit economics.

The PW Consulting Plastics Coating Window Screen Market study is built to convert macro forecasts (USD 1,738 million in 2025; 3.8% CAGR through 2032) into executable plans for 2026. It balances immediate operational fixes — procurement hedges, certification timelines — with medium-term portfolio plays — systems partnerships, automated scaling and material innovation. For leaders who must decide where to allocate scarce R&D and capital in 2026, the study provides the evidence base, scenario tools and playbooks to prioritize actions that protect margins, accelerate compliant growth and capture higher installed-value.

For access to the full dataset, segment models, company scorecards and downloadable dashboards that underpin these recommendations, consult the complete report and interactive materials on our client portal.

For detailed analysis of this topic, please visit the official page:Plastics Coating Window Screen Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com