Is Godrej Plots Jaipur Worth Investing In? Complete Analysis

Other |

2026-07-07 07:47:58

As healthcare providers and device makers enter 2026, the hemostat powder market sits at an inflection point. PW Consulting’s latest market study (base year 2025; historical window 2020–2025; forecast 2026–2032) synthesizes macro dynamics, competitive positioning, and operational levers that will determine winners over the next investment cycle. The global market is mature but expanding—our model shows sustained growth at a compound annual growth rate (CAGR) of approximately 4.8% through the forecast period, with total industry revenues moving from the mid‑hundreds of USD Million in 2025 toward a substantially larger market by 2032.

Hemostat Powder Market

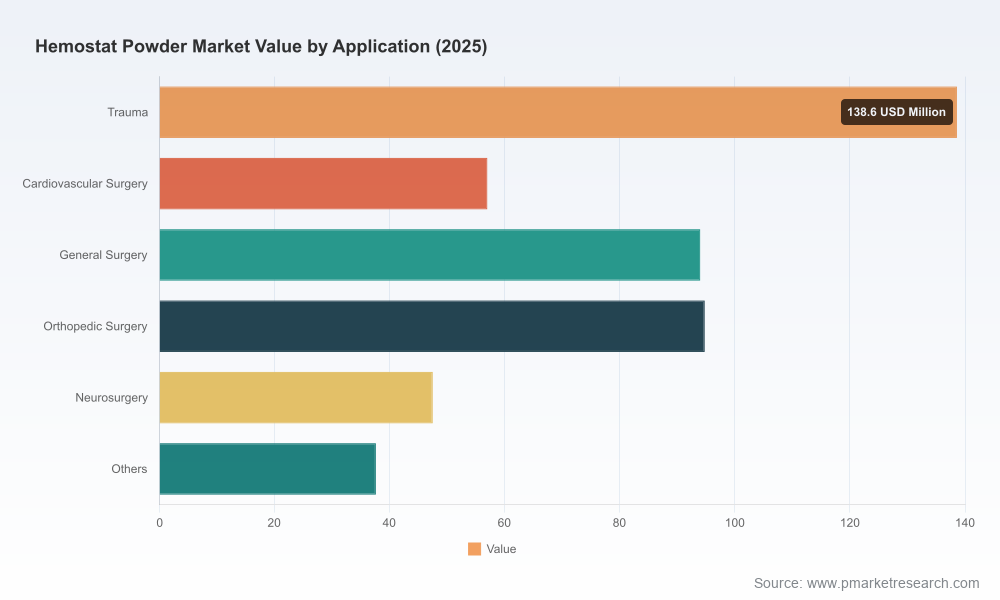

Base year (2025) market valuation and trajectory: The industry is meaningfully larger than five years ago, reflecting steady adoption across endoscopic, surgical, and trauma care settings. Our topline modeling captures historical volume and pricing trends and projects steady expansion under a central case (CAGR ~4.8%).

Hemostat Powder Market

Market structure: The sector remains fragmented — three‑ and five‑firm concentration ratios are modest, indicating an open competitive field and continued opportunity for differentiated entrants and technology consolidators (CR3 and CR5 are both well below levels seen in more consolidated medtech subsegments).

Hemostat Powder Market

Clinical expansion: The most significant demand tailwind is procedural diversification. Hemostat powders have transitioned from niche rescue therapies to routine adjuncts across endoscopy and a growing set of minimally invasive and open surgical procedures. Adoption is being accelerated by real‑world evidence demonstrating reduced procedure time, decreased transfusion rates, and downstream cost offsets for payors.

Innovation in delivery systems: Active and non‑contact spray systems, ready‑to‑use powders, and formulations tailored to specific bleeding profiles are expanding the clinical envelope. These product innovations are also creating distinct commercialization pathways — some favor hospital procurement channels, others leverage GI endoscopy distributors.

Cost pressure and input volatility: Raw material costs for gelatin and oxidized cellulose have risen materially in recent years, and sterilization/regulatory compliance expenses have also climbed. Together these increase COGS and compress gross margins unless offset by pricing or operational efficiency gains.

Regulatory and reimbursement tailwinds: While regulatory certification costs have increased, reimbursement trends are generally favorable. Payers increasingly recognize the cost‑saving potential of endoscopic hemostatic powder therapy, improving the economic case for adoption in ambulatory and inpatient settings.

The market is populated by established medtech firms, specialized hemostasis players, and a growing list of niche innovators. Competitive advantage is shaped by product differentiation, distribution reach, clinical evidence, and sterile manufacturing capability. Core players whose strategies and recent moves are shaping the landscape include:

Cook Medical (Winston‑Salem, NC, USA) — Known for an active delivery platform (Hemospray®) focused on endoscopic control of non‑variceal GI bleeding. The emphasis on device+powder integration gives Cook a strong position in endoscopy suites and allied clinical training channels.

Baxter International Inc. (Deerfield, IL, USA) — Markets PERCLOT®, a passive, polysaccharide‑based powder for adjunctive surgical hemostasis. Baxter’s scale and hospital relationships enable rapid uptake of new SKUs targeted at minimally invasive procedures.

Medtronic plc (Ireland) — Distributes a noncontact sprayed hemostatic system (Nexpowder™) for upper GI bleeding. Medtronic combines procedural device breadth with established procurement pathways in hospitals worldwide.

EndoClotPlus Inc. (Santa Clara, CA, USA) — Developer of a starch‑derived polysaccharide powder optimized for oozing bleeding in endoscopic settings. Niche clinical focus and partnerships, including distribution tie‑ups, are central to its growth trajectory.

Ethicon (Johnson & Johnson) (Somerville, NJ, USA) — Produces SURGICEL® Powder and has pursued acquisitions to bolster bioresorbable powder capabilities. Ethicon’s broad surgical portfolio and M&A activity position it as a consolidation architect in the category.

Ferrosan Medical Devices (Copenhagen, Denmark) — Markets gelatin‑based products such as SURGIFOAM™, leveraging legacy surgical relationships in select geographies.

Ushare Medical Inc. (USA) — Supplies polysaccharide powders with regulatory clearances and EO sterilization, relevant for cost‑sensitive or niche hospital segments.

Distribution and clinical adoption: Major endoscope OEMs have extended distribution agreements and clinical evaluations to accelerate adoption in the U.S. market, increasing visibility of polysaccharide systems in gastroenterology suites.

New product introductions: Leading market participants have launched collagen‑ and other novel formulation powders targeted to minimally invasive procedures — these moves are shifting clinical pathways and procurement conversations toward single‑use, ready‑to‑apply products.

M&A and capability build: Acquisition activity focused on bioresorbable formulations indicates an expectation that product lineage and IP will matter more over the mid term. Buyers are targeting R&D‑light scale‑up and regulatory know‑how.

This release is built as an active playbook for corporate strategy and commercial execution. Highlights include:

Granular market sizing and forecast models (by product class, application, and region) with scenario variants to stress‑test assumption sets.

Go‑to‑market frameworks: segmentation of hospital procurement archetypes, recommended distributor models for endoscopy vs. OR channels, and pricing elasticity tests under different reimbursement regimes.

Regulatory roadmaps and certification cost schedules, including timelines and expected upfront expenditures for sterilization/ISO compliance that materially affect unit economics.

Supply‑chain playbook addressing raw material sourcing strategies, hedging options, and contract manufacturing partner selection criteria to mitigate recent input cost inflation.

Competitive benchmarks, capability maps, and M&A screens identifying likely acquisition targets and buyer archetypes, supported by valuation sensitivity analysis.

Clinical evidence templates and economic value dossiers that commercial teams can adapt to accelerate formulary inclusion and payer conversations.

Prioritize differentiated delivery: Investments in active delivery systems, non‑contact spraying, or unique kit formats generate higher marginal returns than incremental formulation tweaks alone. If your R&D roadmap lacks a delivery innovation, consider partnership or licensing strategies.

Act on supply‑chain resilience now: Given the observed increases in raw material and certification costs, secure multi‑year supply contracts with price floors/ceilings, qualify secondary suppliers, and evaluate backward integration for high‑risk inputs.

Segment commercialization by clinical pathway: Develop tailored value propositions for endoscopy, trauma, and surgical oncology. Channel strategy should distinguish between hospital procurement (larger contracts, GPO negotiation) and outpatient/endoscopy settings (faster adoption, targeted clinical champions).

Leverage health‑economic evidence: Build dossiers that quantify procedure time savings and transfusion avoidance. Payer recognition of cost offsets is an acceleration lever for broader reimbursement—and for favorable contracting terms.

Prepare for consolidation opportunities: Low to moderate market concentration implies attractive bolt‑on targets for scale players. M&A should focus on filling capability gaps (e.g., bioresorbables, sterilized manufacturing capacity, or regionally strong distribution networks).

Price and margin discipline: Use segmented pricing that reflects clinical value and procurement sensitivity. Protect margins by negotiating sterilization and ISO recertification timelines that minimize expensive product recalls or rework.

This market sits between a period of clinical normalization post‑pandemic and a phase of technological maturation. With a predictable mid‑single digit CAGR, the principal battleground in 2026 will be differentiation rather than market creation. Companies that couple product innovation with supply‑chain rigor, health‑economic evidence, and targeted commercial models will capture disproportionate share. Conversely, undifferentiated suppliers face margin erosion as input costs and regulatory fees rise.

PW Consulting’s full Hemostat Powder Market report contains the underlying models, the detailed regional and application splits, and executable playbooks referenced above. For teams making capital allocation, commercial, or M&A decisions in 2026, the full dataset and scenario analyses will materially shorten decision cycles and reduce execution risk. Contact PW Consulting or visit our publications page to access the complete study and proprietary datasets.

For detailed analysis of this topic, please visit the official page:Hemostat Powder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com