Biscuit Shortening Flakes Market Forecast Targeting rapid convenience food processing investments as the Asia-Pacific region claims a dominant 41% regional share

Food |

2026-06-16 12:50:26

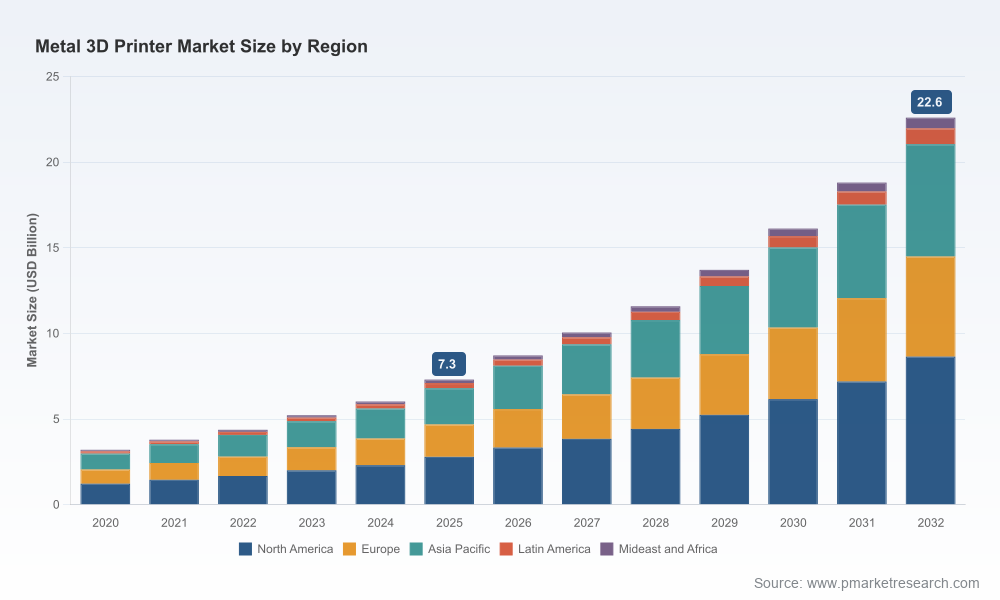

The metal additive manufacturing (AM) market is shifting from early adoption to industrial deployment. Our PW Consulting market model — covering historical performance (2020–2025) and a forward-looking forecast (2026–2032) — projects an annualized expansion at a 17.5% CAGR. Measured in USD billions, the market progressed from roughly 3.2 in 2020 to about 7.3 in 2025 and is forecast to reach approximately 8.7 in 2026, accelerating toward an estimated 22.6 by 2032. These topline dynamics reflect both rising unit shipments of production-class systems and growing service, material, and software revenues that cluster around end-use industrialization.

Metal 3D Printer Market

Timing of investment: With the market entering a steep growth phase in 2026, procurement windows for production-grade machines and binder-jet lines are tightening. Early movers secure capacity, certification pathways, and material supply relationships that become harder to assemble at scale later in the decade.

Metal 3D Printer Market

Certification and qualification pressure: Aerospace and defense qualification standards have matured rapidly. Buyers and OEMs must factor certification timelines and traceability into procurement and program schedules rather than treating them as post-deployment activities.

Metal 3D Printer Market

Supply chain and material volatility: Metal powder supply and pricing dynamics have become a non-trivial component of unit economics. Materials strategy—sourcing, standardization, and recycling—can swing total cost of ownership materially and should be integrated into capital decisions.

Consolidation and competitive concentration: Market concentration metrics indicate a meaningful share controlled by a few incumbents, with implications for interoperability, long-term service availability, and pricing dynamics. Strategic buyers must evaluate supplier roadmaps alongside financial and technical criteria.

This preview is intentionally high-level. The full PW Consulting Metal 3D Printer Market report is a hands-on toolkit for commercial, engineering and corporate development teams preparing 2026 plans. It includes:

Proprietary market model: Annualized market sizing and a rigorous forecast (2026–2032) with scenario layers (baseline, aggressive adoption, slowed growth) and sensitivity to key variables such as lead times, certification velocity, and capital availability.

Technology matrix and roadmaps: Comparative evaluation across LPBF, DED, binder jetting, bound-powder extrusion, and emerging hybrid approaches. For each class we quantify: throughput ranges, typical part sizes, expected lifecycle costs, and maturity timelines for qualification in regulated sectors.

Competitive vendor benchmarking: A structured scorecard covering performance, throughput, materials ecosystem, qualification support, service footprint, and upgradeability. This is augmented with CR3/CR5 market concentration analytics to inform negotiation and sourcing strategies.

Supply chain and materials playbook: Risk heatmaps for powder chemistry, supplier single points of failure, and recommended hedging/verticalization paths. Includes practical templates for material agreements, quality clauses, and recycling/value recovery models.

Use-case ROI models and deployment roadmaps: Pre-built calculators that map part volumes, scrap rates, cycle times, and post-processing costs to payback and unit economics for pilot vs production scenarios.

Regulatory and qualification playbooks: Step-by-step sequences for aerospace, defense, and medical approvals, including recommended validation protocols and data requirements to shorten qualification timelines.

M&A and partnership watchlist: Identifies strategic segments (materials, post-processing, software, service bureaus) where tuck-in acquisitions or JV structures can accelerate time-to-market.

The vendor field is heterogeneous: specialist laser-based incumbents continue to dominate certification-heavy niches, while newer entrants push production economics through binder-jet and innovative deposition methods. Key strategic profiles we highlight in the report include:

EOS GmbH — known for mature laser-based powder bed fusion platforms with multi-laser scaling and strong aluminum/copper support strategies. Their emphasis on high-reliability systems and materials depth positions them well for aerospace and regulated industrial programs.

3D Systems — offers DMLS platforms with integrated powder handling that appeal to manufacturers seeking closed-loop workflows and high uptime. Recent product updates underscore a push to broaden throughput options for productionized lines.

Renishaw — couples laser powder bed systems with in-line metrology and process control, which simplifies qualification pathways for customers that require tight traceability and part-level measurement integration.

Nikon SLM Solutions — a competitive player in high-throughput LPBF, with multi-laser architectures designed to increase build rates without sacrificing resolution. Their trajectory signals a technological arms race on lasers-per-build-chamber as a route to scale.

Desktop Metal — a frontrunner in binder jetting production systems, targeting end-use metal parts at scale through a systems approach that includes powder, print lines, and sintering throughput planning.

Markforged — pursues differentiated markets with bound powder extrusion for accessible metal printing and composite synergies, relevant for industrial maintenance and tooling applications.

FormAlloy — specializes in Directed Energy Deposition for large-format builds and in-situ repair, giving them an edge in heavy aerospace structures and field-service use cases.

Recent product refreshes and new entrants are important signals. During the past 12–18 months, a number of firms announced new high-speed printers and production-focused lines, indicating that vendor competition will increasingly be fought on throughput, total cost of ownership, and readiness to support qualification programs.

Based on our modelling and advisory work across buyer archetypes, companies should consider three pragmatic strategies depending on their risk appetite and business model:

Fast-scaler: Commit to production-capable binder-jet or multi-laser LPBF capacity now. Pros: first-to-scale economics, deeper supplier integration. Cons: higher upfront capital, material/qualification risk to manage.

Orchestrator: Build partnerships with qualified service bureaus and retain focused in-house capability for critical parts. Pros: lower capex and faster access to certified supply. Cons: less control over IP and potential throughput bottlenecks at partners.

Measured adopter: Continue robust pilot programs, invest in qualification dossiers and training, but defer large fleet purchases until second-generation systems demonstrate predictable TCO. Pros: lower near-term capital exposure. Cons: risk of longer lead times to scale if demand spikes.

Whichever route is chosen, procurement teams should evaluate suppliers on five core metrics: demonstrable qualification assets, end-to-end powder management, proven uptime in comparable production settings, service and spare parts reach, and clarity of upgrade/migration pathways.

We crafted this preview to surface the strategic levers that matter as organizations finalize their 2026 manufacturing and investment plans. The metal AM market’s strong macro trajectory — underpinned by double-digit CAGR and a transition from prototyping to end-use production — creates attractive opportunities but also elevates execution risk around qualification, materials and supplier concentration.

For procurement leaders, R&D heads, and corporate strategists, the full PW Consulting Metal 3D Printer Market report contains the detailed segmentation, vendor scorecards, downloadable datasets, scenario-based financial models, and actionable procurement templates needed to convert strategic intent into measurable outcomes. We intentionally withhold tranche-level regional and application splits in this preview to preserve the research integrity of our deliverable — the complete intelligence package is available through our report portal.

Engage with PW Consulting’s advisory team to map these findings into a tailored 2026 action plan: from equipment selection and partner sourcing to materials hedging and certification roadmaps.

For detailed analysis of this topic, please visit the official page:Metal 3D Printer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com