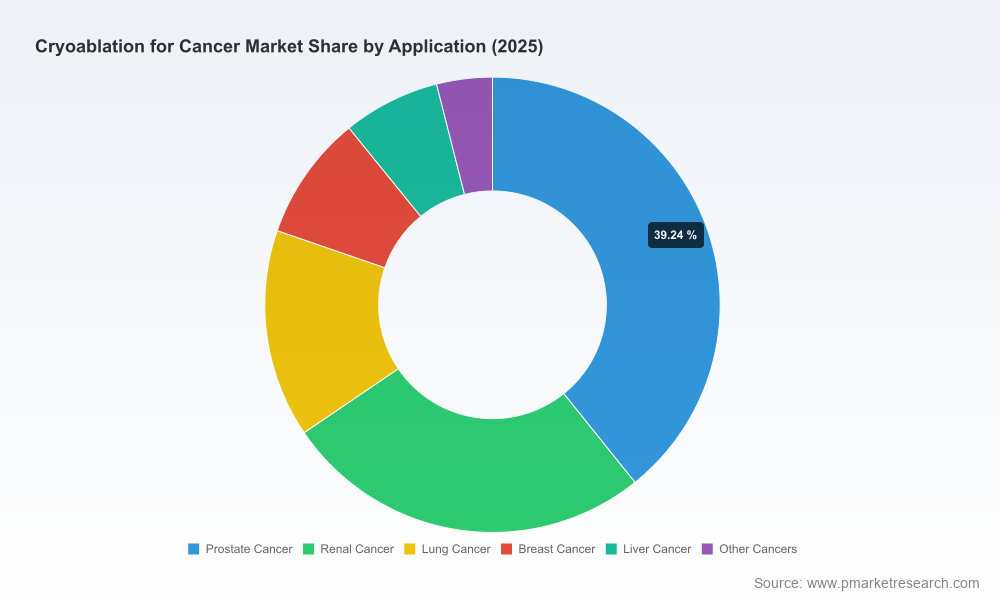

PW Consulting: Cryoablation for Cancer Market to Rise from USD 475.0 Million in 2025 to USD 902.41 Million by 2032 at a 9.42% CAGR, Led by Cryoprobes (USD 323.95M)

Other |

2026-07-02 18:04:09

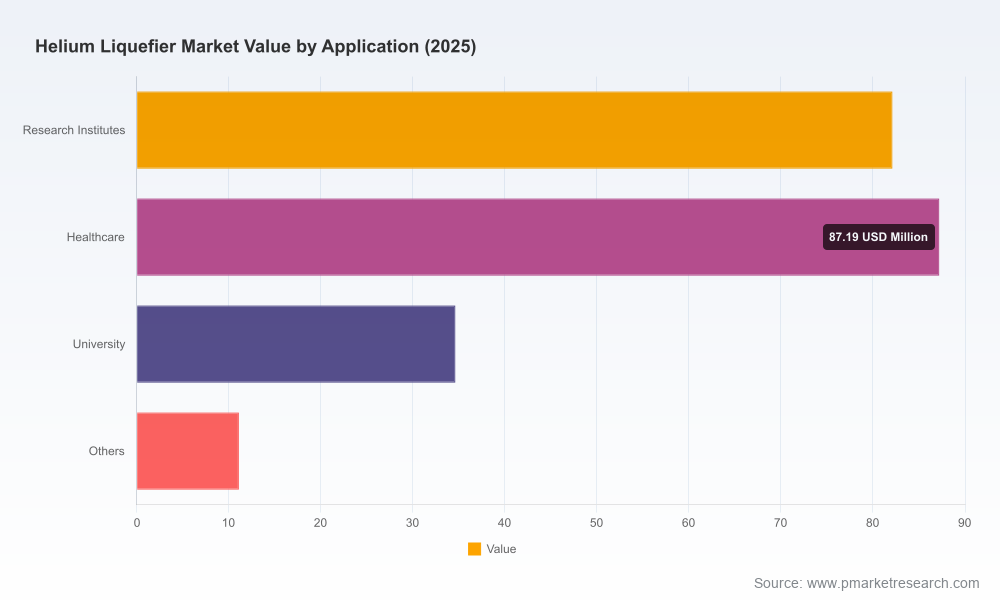

As of the 2025 base year, the global helium liquefier market has matured into a mid‑single‑hundred million USD industry with a clear, multi‑year uptrend. After expanding steadily through the 2020–2025 historical window, the market is projected to continue its expansion across the 2026–2032 forecast horizon at a compound annual growth rate of approximately 6.7%, reaching the high hundreds of millions by 2032. For boards, corporate development teams, and industrial procurement leaders, 2026 is not merely another planning cycle — it is the inflection point at which supply‑side instability, accelerating end‑use demand (from healthcare to quantum and aerospace), and technology choice converge to determine capital allocation and competitive positioning for the rest of the decade.

Helium Liquefier Market

Supply shocks are now a structural variable in procurement decisions. Recent policy and geopolitical events in 2026 — including new export controls and regional conflicts that temporarily curtailed major production hubs and disrupted chokepoints — demonstrate how quickly physical availability can change. These shocks are amplifying volatility in an otherwise steadily growing market and have immediate implications for how companies size buffer inventories, structure contracts, and evaluate on‑site liquefaction.

Helium Liquefier Market

Demand drivers are diversifying. Beyond traditional laboratory and medical uses, the commercial roadmap for liquefaction equipment now explicitly embraces aerospace testing, semiconductor manufacturing, and emerging quantum computing installations. These end uses bring different utilization profiles, location constraints, and service expectations that change the calculus for capex vs. opex, modular vs. custom systems, and lifecycle service offerings.

Helium Liquefier Market

Market structure and supplier economics create leverage points. The upper tier of suppliers maintains a measurable share of market supply and technological capability, but fragmentation below this tier leaves opportunities for specialization, modular product plays, and service‑led differentiation — particularly for customers seeking integrated helium recovery, reliquefaction, and long‑term service contracts.

Transparent, audit‑ready market sizing and a demand model built from 2020–2025 historical data and a 2026–2032 scenario framework (base, stress, and upside).

Technology taxonomy and selection framework: piston‑expander vs. turbine‑expander vs. vacuum cold box architectures, with decision matrices keyed to throughput, uptime, energy intensity, and serviceability.

Supplier benchmarking and sourcing playbook: capability maps, purchase‑to‑service lifecycle TCO templates, RFP language, and due‑diligence checklists for warranty and spare parts ecosystems.

CapEx/Opex modeling tools with sensitivity analyses for utilization, helium price shocks, and downtime risks — built to plug into capital approval processes.

Operational case studies (NMR/research facilities, aerospace test centers, and distributed medical gas networks) showing deployment pathways, common pitfalls, and remediation strategies.

Regulatory and geopolitical scenario simulations, with mitigation options mapped to procurement lead times and contractual clauses.

M&A and partnership heatmaps highlighting niches attractive to private equity and strategic buyers (service ecosystems, modular OEMs, recovery technology vendors).

The market is served by a set of well‑established engineering majors alongside specialized OEMs focused on recovery and compact reliquefiers. Tactical sourcing in 2026 is therefore a choice between the scale, integration and turnkey expertise of global engineering houses and the agility and product focus of specialized suppliers.

Air Liquide Advanced Technologies (Paris, France) — Offers the HELIAL family of standard liquefiers and custom systems for laboratories, scientific instrumentation and aerospace test stands. Their strength lies in modular product ranges and deep experience in lab‑scale integration and after‑sales networks. (See corporate offering: https://advancedtech.airliquide.com/markets-solutions/deep-tech/science/helium-liquefaction)

Linde Engineering (Pullach, Germany) — A full‑spectrum player delivering both piston‑expander and turbine‑expander designs plus large‑scale recovery and liquefaction plants. Recent contract wins indicate their continued role as a prime contractor for complex, high‑availability installations. (https://www.linde-engineering.com/products-and-services/process-plants/natural-gas-processing/helium-recovery-and-liquefaction-plants)

Chart Industries (Ball Ground, Georgia, USA) — Known for cryogenic vacuum cold box systems that produce high‑purity liquid helium at industrial scale. Their portfolio suits capital‑intensive, high‑throughput applications requiring 100% liquid production and integrated cold‑chain solutions. (https://www.chartindustries.com/Products/Helium-Liquefiers)

Cryomech (Syracuse, NY, USA) — Specializes in recovery and reliquefier systems, including compact units for single‑instrument NMR and quantum computing racks. They are often the preferred choice for installations where footprint and continuous recovery are primary constraints. (Product overview: https://bluefors.com/products/liquid-helium-management-products/helium-reliquefiers/)

Notable near‑term developments to factor into procurement timelines: Linde’s sole‑source contract award for a NASA liquefier program (Jan 2025) and modular, 24‑hour continuous systems released by specialty OEMs in 2025. These moves underscore the bifurcation of the market into large turnkey projects and modular, service‑centric deployments.

Validate your supply risk budget now. Reassess inventory strategies (minimum days on hand), and price hedging where available. Factor in additional lead times for equipment and spare parts driven by export controls and shipping disruptions.

Prioritize modularity for near‑term deployments. Where possible, choose modular liquefiers that reduce commissioning time and allow capacity scaling without large incremental capex.

Balance CapEx and service economics. A lower initial capex purchase can become more expensive if service networks are immature; require explicit service level agreements and spares availability clauses in procurement contracts.

Invest in on‑site recovery where process continuity matters. For high‑uptime applications (aerospace testing, quantum) reliquefiers and closed‑loop recovery reduce exposure to market tightness and transport disruption.

Embed regulatory and geopolitical triggers into contract governance. Include force majeure definitions, contingency sourcing steps, and supplier audit rights to navigate export controls and sanctions risk.

Use supplier stratification in RFPs. Structure bids to allow multiple award strategies: a primary systems provider for turnkey delivery plus a secondary specialist for redundancy on critical subsystems.

Screen for lifecycle sustainability. Energy consumption and leakage rates materially affect TCO in multi‑year contracts — include measured lifecycle performance targets in procurement evaluations.

A university research cluster replaced periodic bulk deliveries with a compact reliquefier and a tiered service contract; operational continuity improved and scheduling risk shifted away from third‑party logistics.

An aerospace test center pursued a hybrid model: modular liquefaction units for daily testing demands and a standby vacuum cold box for surge events — enabling predictable test schedules during regional supply disruptions.

Full case studies, including deployment timelines, capex/opex tradeoffs, and contract language templates, are available in the complete PW Consulting report.

Board briefings — provide scenario summaries for capital approval and risk exposure quantification.

Procurement and legal — translate supplier benchmarking into RFPs and robust contracts that anticipate export controls and chokepoint disruptions.

Operations and engineering — adopt the technology selection framework and TCO models for vendor evaluation and pilot sizing.

Corporate development — use the M&A heatmaps and competitive benchmarking to identify acquisition or partnership targets that accelerate service ecosystems or modular product offerings.

The helium liquefier market is expanding steadily, but 2026 introduces new volatility that will determine winners and losers in procurement cycles and product positioning. Executives who combine a disciplined supply‑risk framework, modular technology adoption, and supplier governance now will capture asymmetric benefits as demand profiles evolve. Our report provides the analytical foundation — market sizing, scenario models, supplier playbooks and transaction‑ready tools — to convert uncertainty into executable strategy.

For the full dataset (including regional and application‑level forecasting, detailed segment economics, downloadable financial models, and the complete supplier scorecards), access the PW Consulting Helium Liquefier Market report and associated annexes.

For detailed analysis of this topic, please visit the official page:Helium Liquefier Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com