NAC (Acetylcysteine) Market: Strategic Roadmap for 2026 Decision-Makers

Executive preview

As PW Consulting’s lead industry analyst, I present a focused preview of our NAC (N‑acetylcysteine) Market study designed to inform executive decisions in 2026. This briefing demonstrates the analytical depth and actionable framing available in the full report while deliberately withholding detailed segment-level datapoints so senior teams must consult the full publication for transaction‑grade intelligence.

NAC (Acetylcisteine) Market

Why NAC matters to corporate strategy in 2026

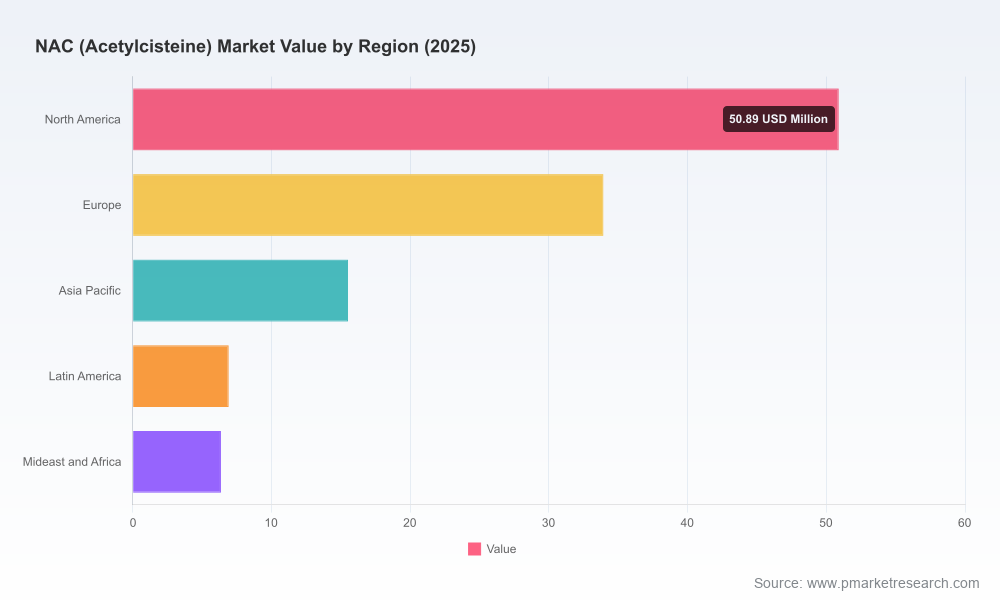

NAC has evolved from a niche mucolytic to a multi-use API underpinning hospital parenteral therapies, respiratory products, and nutrition/supplement lines. The market trajectory over the last half‑decade shows robust expansion: the global market roughly doubled from the low tens of USD‑million in 2020 to a six‑figure‑scale in USD‑million by 2025, and it is forecast to continue at a strong compound annual growth rate (CAGR) of about 13.5% across the 2026–2032 horizon. That pace creates strategic imperatives for manufacturers, CMO/CDMOs, life‑science distributors, and branded product owners alike—ranging from capacity planning and sourcing policy to regulatory positioning and portfolio prioritisation.

NAC (Acetylcisteine) Market

High‑level market trajectory and what it means

- Structural growth. Demand is being driven by a combination of hospital use (parenteral and IV formulations), sustained interest in respiratory indications, and a parallel consumer/supplement channel. The growth profile is not uniform across channels, but overall expansion creates optionality for scale players and targeted opportunity windows for specialised entrants.

- Mid‑term upside. The market’s forecast path to 2032 implies accelerating absolute demand that will favor licensed suppliers with validated quality systems and documented regulatory filings (DMF/CEP/EDQM equivalents).

- Concentration and competitive dynamics. Market concentration is moderate: the three largest suppliers control less than half of global revenue, and the five largest approach roughly six tenths of the market. This structure creates both defensible positions for incumbents and feasible entry vectors for challengers who can address quality, cost, or supply reliability differentials.

What the full report delivers (practical, transaction-ready modules)

- Bottom‑up market model (base year 2025, historical series 2020–2025, forecast 2026–2032) with scenario outputs for base, downside, and upside cases.

- Granular demand drivers mapped to clinical, OTC/supplement, and nutrition channels—each tied to epidemiology, prescribing trends, and reimbursement shifts.

- Supply‑side mapping: validated API producers, contract manufacturers, CMOs for IV and oral dosage forms, and a supplier‑assessment framework aligned to DMF/CEP/USP/EP/JP compliance.

- Price and margin benchmarking across the value chain, including purchased input sensitivity and finished‑good price elasticity.

- Regulatory and commercial playbooks: licensing pathways, export compliance, and recommended dossier strategies for market entry and label expansions.

- Detailed company profiles and capability matrices for the leading players, recent M&A and capacity moves, and a readiness checklist for strategic sourcing and M&A diligence.

- Procurement and risk tools: supplier scorecards, dual‑sourcing templates, forward hedging scenarios for critical raw inputs, and an implementation roadmap for supply continuity.

Competitive landscape—what incumbents are doing now

The competitive set mixes specialised API producers, multinational hospital‑focused players, and nutritional supplement suppliers. Several patterns stand out:

NAC (Acetylcisteine) Market

- Scale + regulatory depth wins hospital tenders. Companies supplying IV formulations and parenteral nutrition leverage established regulatory dossiers and hospital procurement relationships. They increasingly invest in capacity and sterile/aseptic capabilities to capture higher‑value segments.

- API specialists differentiate on documentation and origin tracing. Suppliers that maintain comprehensive DMF/CEP/USP/EP/JP filings and capable audit trails dominate quality‑sensitive flows to branded pharmaceutical manufacturers.

- Geographic supply layering is strategic. Players source raw inputs from diverse origins—fermentation and alternative feedstocks—to manage cost and regulatory risk. This is particularly visible in companies that disclose multi‑origin sourcing strategies to meet global demand.

Representative company positions

- Axplora (Germany): A vertically capable API producer focused on pharmaceutical‑grade NAC. Recent capacity expansions and investments in adjacent high‑growth biologics/GLP‑1 manufacturing at EU sites signal an ambition to move up the value chain and secure higher‑margin, regulated supply contracts.

- Zambon S.p.A. (Italy): Brings depth in IV and oral respiratory formulations with an emphasis on hospital portfolios. Recent regulatory approvals in major markets demonstrate successful clinical and regulatory execution for parenteral products.

- Nippon Rika (Japan) and Wuhan Grand Hoyo (China): API manufacturers with global supply footprints; they underscore the importance of multi‑pharmacopeia compliance and certifications in winning multinational business.

- Fresenius Kabi, Boehringer Ingelheim, Sigma‑Aldrich (Merck): These established healthcare and chemical suppliers act as anchor buyers/sellers in hospital, research, and pharma channels—providing distribution reach and regulatory credibility but also presenting price discipline for the market.

- Regional and specialty players (e.g., Pharma Nord, Manus Aktteva, Moehs): Tend to focus on supplements, clinical formulation support, or niche generics/paused markets, affording them flexibility in commercial strategy but limiting scale in tendered hospital channels.

Recent developments that shape 2026 choices

- Capacity and investment: Targeted expansions by established API producers in 2025 improved availability for regulated supply chains but also signal intensifying competition for higher‑value hospital business.

- Regulatory milestones: Regulatory approvals for IV formulations in large markets unlock hospital adoption curves and require manufacturers to maintain clinical and manufacturing evidence to scale.

- Policy and enforcement: Recent regulatory guidance on the classification of NAC in certain jurisdictions has material implications for how manufacturers and sellers classify, label, and export products—especially where supplement vs pharmaceutical definitions differ.

Industry dynamics and risk vectors

Five dynamics should guide 2026 decisions:

- Regulatory clarity vs. fragmentation. Where regulators have issued definitive guidance on NAC classification, market access becomes transactional; where ambiguity remains, commercial risk escalates—impacting distribution channels and export documentation.

- Sourcing and raw material variability. The market shows increasing use of diversified feedstocks (including fermentation and alternative biological sources). Procurement strategies must account for traceability, auditability, and potential supply shocks.

- Quality and documentation as gatekeepers. Pharmacopeial compliance (USP/EP/JP and equivalents) and DMF/CEP readiness are minimums for hospital and international markets; those without complete dossiers will be excluded from many tenders.

- Concentration creates targeted opportunities. With the top handful of suppliers capturing a material share of revenue, focused challengers can win through specialized services (fast regulatory filing, niche formulations, superior supply continuity) rather than broadscale price competition.

- Export and certificate complexity. Export certificates and CAP requirements are nontrivial in several markets; manufacturers must align export documentation capabilities with trade strategy to avoid shipment delays and lost sales.

Strategic playbook for 2026

Based on the market model and supplier insight, PW Consulting recommends a three‑pronged approach for market entrants and incumbents preparing for 2026:

- Secure quality credentials and dual‑sourcing: Prioritise DMF/CEP readiness and at least one alternate source for critical feedstocks. This reduces tender risk and supports premium pricing in hospital segments.

- Prioritise formulation and channel focus: Decide early whether to compete in parenteral/hospital, OTC/supplement, or nutrition channels. Each requires distinct regulatory, quality, and commercial investments; partial overlap exists but execution must be channel‑specific.

- Targeted partnerships over broad M&A: Consider strategic partnerships or minority investments with quality‑certified API producers to secure supply, share risk, and accelerate market entry without the overhead of greenfield facilities.

How PW Consulting supports your 2026 agenda

Our full NAC Market report is structured to convert insight into action: granular scenario models, supplier due diligence templates, regulatory filing playbooks, and procurement negotiation scripts. For teams evaluating capacity expansion, supplier contracts, or M&A in 2026, the report provides the empirical foundations and tactical tools needed to de‑risk decisions and accelerate time to value.

Disclosure and next steps

This article intentionally focuses on strategic context and high‑level metrics to illustrate the research’s value; detailed regional and application splits, exact price series, and transaction‑level figures are available exclusively in the full PW Consulting NAC Market report. If you are preparing a 2026 strategic plan—whether sourcing, licensing, or investing—contact PW Consulting to obtain the full dataset, scenario workpapers, and tailored advisory engagement options.

For detailed analysis of this topic, please visit the official page:NAC (Acetylcisteine) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com