Agricultural Biotechnology Market Size, Share, Innovation Trends and Forecast by 2032v

Other |

2026-05-11 13:07:07

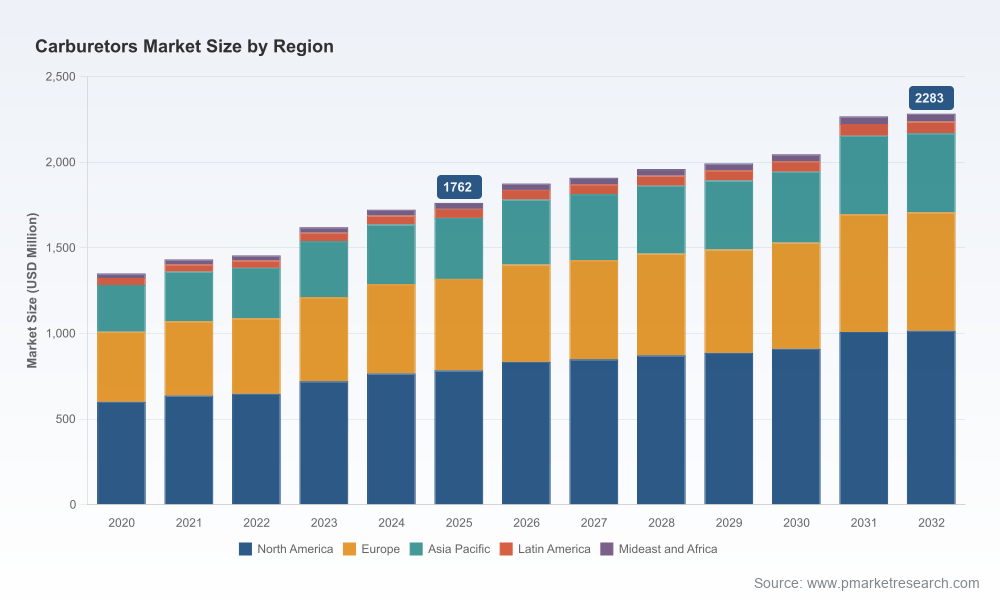

As organizations set strategy for 2026, the carburetors market presents a mix of steady recovery, regulatory pressure, and selective innovation. Our PW Consulting base-year analysis (2025) shows the global market at approximately USD 1,762 Million, with a forecast compound annual growth rate (CAGR) of 3.8% across the 2026–2032 horizon. By the end of the forecast period the market is projected to be in the low‑billions (USD), reflecting modest growth tempered by tightening emissions rules and ongoing electrification trends in key applications.

Carburetors Market

This briefing highlights the strategic value of our full Carburetors Market report for C‑suite executives, corporate strategy teams, OEM procurement leads, and M&A advisors. It signals where opportunity and risk cluster without disclosing the granular segment tables that are reserved for report subscribers — a deliberate “trailer” approach to invite deeper engagement with the underlying data and models.

Carburetors Market

Regulatory inflection points are compressing product life cycles. California and U.S. federal actions (notably tighter NOx/PM targets and restrictions on certain small‑engine sales and uses) are changing product design requirements and aftermarket opportunities faster than typical replacement cycles.

Carburetors Market

Manufacturers face a dual imperative: reduce unit costs while preserving emissions compliance. Material substitution (for example, greater use of plastics in structural components) is already reshaping BOMs and supplier footprints.

Market structure remains moderately concentrated (CR3 near 30%, CR5 near 40%), which means incumbents retain pricing and distribution advantages, but there is sufficient room for niche specialists and agile entrants to capture share via targeted innovation or regional plays.

Operators considering M&A, joint ventures, or manufacturing reconfiguration need scenario-tested revenue models and regulatory risk overlays to avoid overpaying for legacy technology exposure.

Our modeling — calibrated on 2020–2025 historicals and forward‑looking demand drivers — projects a steady, single‑digit growth trajectory. The base‑year market size (2025) of ~USD 1,762 Million expands at 3.8% CAGR across the 2026–2032 period, reflecting a balance of continuing demand in small engines and recreational applications, offset by structural headwinds from electrification and tighter emissions mandates for on‑road and industrial powertrains.

Strategic implication: companies that lean into emission‑compliant architectures and that can rapidly iterate low‑cost material alternatives will preserve near‑term revenue while creating optionality for transition strategies beyond 2030.

Stringent state‑level emissions mandates are forcing earlier redesigns and constraining aftermarket adjustability. Recent rules require large reductions in NOx and particulates for heavy‑duty engines and are proposing sales restrictions for certain internal combustion industrial equipment — outcomes that materially alter TAM assumptions for specific product families.

Federal and state enforcement around factory‑set calibration (disallowing post‑production adjustment that compromises emissions) increases the engineering bar for carburetor manufacturers supplying into regulated markets.

Supply‑side responses include accelerated adoption of engineered plastics, consolidation of specialist precision machining, and deeper supplier integration with OEMs to lock in compliance documentation and traceability.

Incremental innovation continues to be a route to differentiation: improved metering rods, automatic air‑density compensation, and unibody construction options are lowering warranty costs and improving altitude performance for recreational and off‑road segments.

At the same time, the product roadmap for many players now includes hybrid approaches — combining carburetion expertise with electronic controls or preparing modular interfaces that can be swapped for fuel‑injection subsystems as regulations and end‑market demand push electrification.

Productization strategies that emphasize emissions traceability, calibration integrity, and cost‑effective plastics substitution are gaining adoption among OEMs and large distributors.

The market is shaped by a mix of long‑established OEM suppliers, specialist niche players, and regional manufacturers that serve high‑volume small‑engine markets. Below are strategic profiles and implications for each highlighted player.

Keihin Corporation (Tokyo, Japan): Deep OEM relationships in motorcycles and small engines, coupled with a strong compliance orientation. Strategy: double down on emissions‑validated platforms and pursue integrated supply agreements with tier‑one motorcycle OEMs.

Mikuni Corporation (Tokyo, Japan): Known for slide and diaphragm designs for recreational vehicles. Strategy: leverage engineering heritage to push higher‑value service parts and performance‑tuned solutions where carburetors remain preferred.

Walbro LLC (Auburn, Alabama, USA): Strength in diaphragm carburetors and fuel systems for power equipment and marine. Strategy: use systems‑level offerings to deepen OEM lock‑in and cross‑sell fuel delivery subsystems that simplify regulatory compliance for customers.

Zama Group (Germany): Focus on small‑engine carburetors for lawn/garden equipment. Strategy: capitalize on aftermarket replacement cycles and expand low‑cost manufacturing channels while ensuring ISO and quality traceability demanded by global OEMs.

Holley Performance Products (USA): High‑performance and racing applications where carburetors remain preferred for tunability. Strategy: protect specialty margins and explore performance‑focused electrified accessory markets.

Dell'Orto S.p.A. (Italy): Supplier to automotive and karting markets with parts and whole assemblies. Strategy: emphasize OEM integrations and parts availability for legacy platforms in regions where full electrification is slower.

Bing Power Systems GmbH (Germany): Niche expertise for specialty equipment. Strategy: target high‑mix, low‑volume industrial niches where customization commands premium pricing.

Fuding Youli Carburetor Co., Ltd. (China): Volume supplier for two‑wheelers and commercial vehicles. Strategy: use scale to compete on cost while upgrading quality systems to penetrate regulated export markets.

Huayang Industrial (China): Producer for garden tools and OEMs; recent ISO9001 certification for a new production base underlines quality focus. Strategy: pursue certified supply contracts and OEM partnerships in regions with strict supplier quality requirements.

SmartCarb (USA): Agile innovator of metering‑rod designs; in 2025 it launched the SC3 series with features such as automatic air‑density compensation and unibody construction. Strategy: exploit niche performance and altitude‑compensation advantages to gain share in off‑road and specialty small‑engine segments.

Product launches that materially improve altitude and emissions performance have outsized impact on recreational and powersports revenue under constrained emissions regimes (example: SmartCarb SC3 family launched mid‑2025).

Quality and production certifications (example: Huayang’s ISO9001 for a new production base in late‑2025) accelerate access to OEM supply chains where compliance documentation is a gatekeeper.

Regulatory proposals and enforcement around emissions, sales restrictions for certain internal combustion equipment, and limits on post‑manufacture carburetor adjustments are reshaping both product engineering and aftersales service models.

Demand modeling with scenario variants that quantify upside/downside under alternative regulatory and electrification pathways (including sensitivity analyses and Monte Carlo overlays).

Practical go‑to‑market playbooks for product managers and OEM procurement: BOM optimization levers, target cost trees, and validation roadmaps to meet emissions and altitude tolerances.

Supplier and capacity maps, benchmarking matrices, and an M&A screen that highlights high‑leverage consolidation targets by risk profile.

Regulatory impact heatmaps and compliance checklists tailored to North American, European, and Asia‑Pacific requirements (note: detailed regional segment tables are included in the full report).

Price and raw‑material scenarios (including plastic substitution and machining vs. molded tradeoffs), warranty‑cost modeling, and channel profitability analysis for aftermarket vs OEM sales.

Product Roadmap: Prioritize emissions‑centric improvements and material substitution pilots that preserve margin while meeting state/federal calibration rules.

Manufacturing Footprint: Use our supplier maps and cost scenarios to evaluate whether to localize production for compliance documentation and air‑freight avoidance, or to centralize for cost efficiency.

M&A and Partnerships: Screen targets that add emissions‑validated IP or that provide certified manufacturing capacity in regulated markets; adjust valuation multiples for regulatory tail‑risk.

Commercial Strategy: Rebalance channel focus toward OEMs with long‑term compliance roadmaps and build aftermarket offerings that emphasize verified, factory‑set calibrations.

Risk Management: Embed regulatory scenario stress‑tests into product P&Ls to understand when subsegments become uneconomic under proposed CARB/EPA regimes.

This briefing is designed to surface the strategic implications of our 2025‑calibrated analysis and to demonstrate the practical, executionable tools contained in PW Consulting’s full Carburetors Market report. For detailed regional and application segment tables, downloadable datasets, and the proprietary forecasting workbook, access to the full report is required. We intentionally hold back granular segment numbers here to protect the value of the underlying research and to invite direct engagement with our analytics team.

Decision-makers preparing budgets and strategic plans for 2026 should prioritize access to the full study to ensure their capital allocation, product development, procurement, and M&A choices are informed by the most current regulatory overlays and probabilistic demand scenarios. PW Consulting can provide tailored briefings or a custom model workshop to translate the report’s insights into a 90‑day action plan for your organization.

For detailed analysis of this topic, please visit the official page:Carburetors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com